رجحان اور اتار چڑھاؤ کو یکجا کرنے والی مقداری تجارتی حکمت عملی

خلاصہ

دوہرا رجحان اتار چڑھاؤ کی حکمت عملی ایک مقداری تجارتی حکمت عملی ہے جو رجحان اور اتار چڑھاؤ کو یکجا کرتی ہے۔ یہ دو اشاروں کے مجموعے کا استعمال کرکے رجحان کی سمت اور شدت کی شناخت کرتی ہے، اور رجحان کے اتار چڑھاؤ کے دوران بہتر داخلے کے مواقع تلاش کرتی ہے۔

حکمت عملی کا اصول

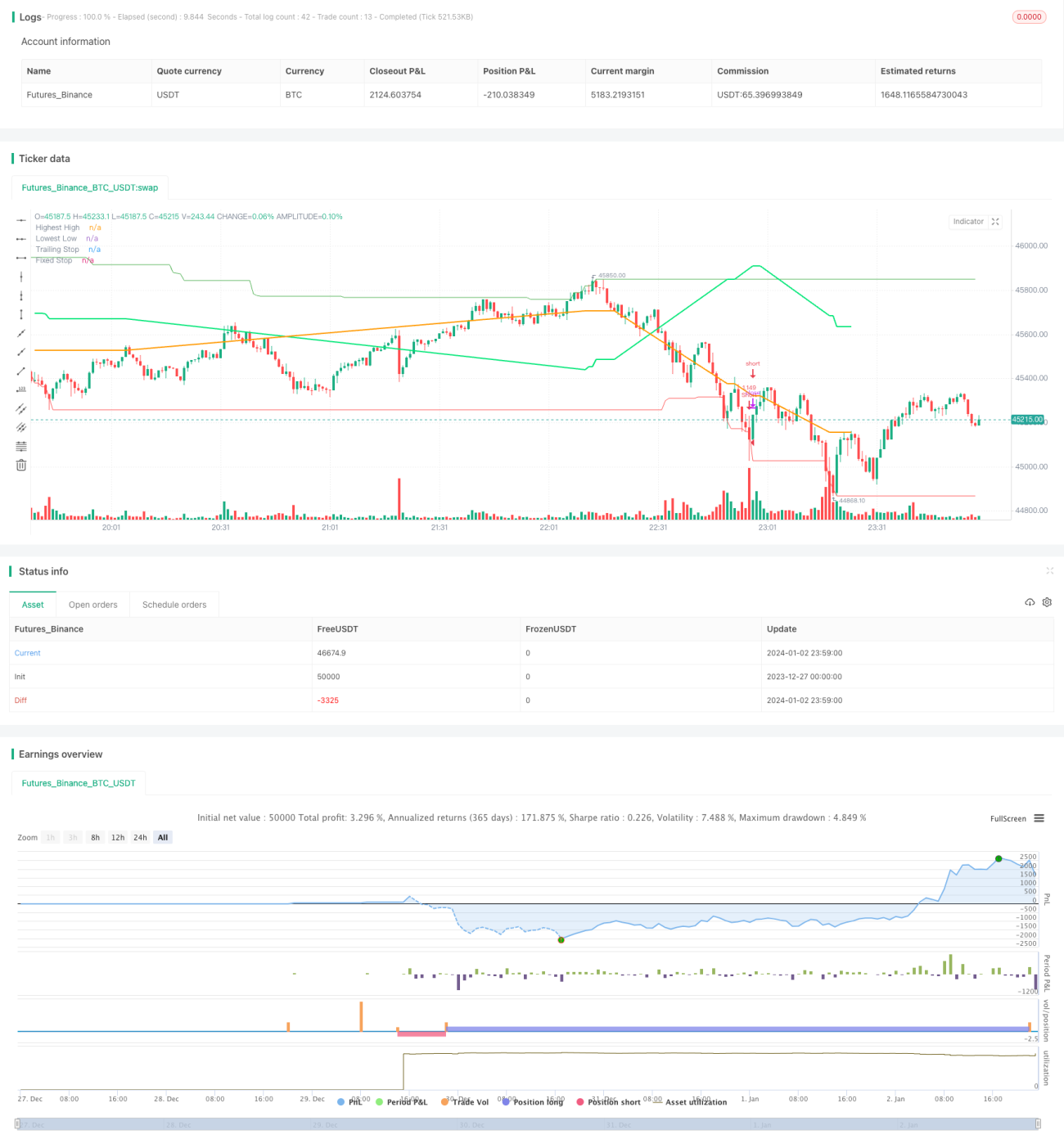

یہ حکمت عملی بنیادی طور پر دو عوامی اشارے استعمال کرتی ہے: Trend Surfers اور Mawreez's Trend Oscillator۔

Trend Surfers ایک رجحان پر مبنی سٹاپ لاس کا اشارہ ہے۔ یہ ایک مخصوص مدت کے اندر بلند ترین اور پست ترین قیمتوں کا حساب لگا کر قیمت کی حرکت کا اندازہ لگاتا ہے اور سٹاپ لاس کی تجویز کردہ پوزیشن دیتا ہے۔ مثال کے طور پر، جب قیمت حالیہ 168 کینڈلز کی بلند ترین قیمت کو توڑتی ہے تو یہ تیزی کا اشارہ ہے؛ جب قیمت حالیہ 168 کینڈلز کی پست ترین قیمت سے نیچے آجاتی ہے تو یہ مندی کا اشارہ ہے۔

Mawreez's Trend Oscillator ایک دو لکیروں والا اتار چڑھاؤ کا اشارہ ہے۔ یہ MACD سے مشابہ ہے، DI کے فرق کے ذریعے رجحان کی سمت اور شدت کا تعین کرتا ہے۔ اس اشارے کا منحنی خط زیرو لائن سے اوپر ہونا تیزی اور نیچے ہونا مندی کی علامت ہے۔

اس حکمت عملی کے تجارتی اصول یہ ہیں:

لمبی پوزیشن میں داخلہ: جب Trend Surfers بلند ترین لکیر کو توڑے اور Mawreez's Trend Oscillator تیزی کا اشارہ دے تو خریدیں

چھوٹی پوزیشن میں داخلہ: جب Trend Surfers پست ترین لکیر سے نیچے آئے اور Mawreez's Trend Oscillator مندی کا اشارہ دے تو بیچیں

سٹاپ لاس کا طریقہ رجحان پر مبنی سٹاپ لاس اور مقررہ سٹاپ لاس کا مجموعہ ہے۔

فوائد کا تجزیہ

یہ حکمت عملی رجحان اور اتار چڑھاؤ کے اشاروں کو یکجا کرتی ہے، جس سے یہ رجحان کو پکڑنے کے ساتھ ساتھ اتار چڑھاؤ میں بہتر قیمت پر داخل ہونے کے مواقع بھی فراہم کرتی ہے۔ اس کے درج ذیل فوائد ہیں:

- دوہرا اشارہ فلٹریشن، جو جھوٹے بریک آؤٹ سے مؤثر طریقے سے بچ سکتا ہے

- رجحان اور اتار چڑھاؤ کا امتزاج، اتار چڑھاؤ کے علاقے میں کم قیمت پر خریداری یا زیادہ قیمت پر ہلکی پھلکی پوزیشن لینے میں مدد دیتا ہے

- متعدد سٹاپ لاس کے طریقوں کا استعمال، جو خطرے کو اچھی طرح کنٹرول کر سکتا ہے

خطرات کا تجزیہ

اس حکمت عملی میں کچھ خطرات بھی ہیں:

- دوہرے اشاروں کا مجموعہ، آرڈر چھوٹ جانے کا امکان

- رجحان اور اتار چڑھاؤ کے اشارے متضاد سگنل دے سکتے ہیں

- مقررہ سٹاپ لاس قبل از وقت سٹاپ لاس کا سبب بن سکتا ہے

ان خطرات سے بچنے کے لیے درج ذیل اقدامات کیے جا سکتے ہیں:

- اشاروں کے پیرامیٹرز کو مناسب حد تک ڈھیلا کرنا، فلٹریشن کی شرح کم کرنا

- رجحان کے تعین کے قواعد میں اضافہ، اشاروں کے تضاد سے بچنا

- سٹاپ لاس کی پوزیشن کو متحرک طور پر ایڈجسٹ کرنا

بہتری کی سمت

اس حکمت عملی میں مزید بہتری کی گنجائش ہے:

- مختلف پیرامیٹرز کے مجموعے اور دورانیے کے پیرامیٹرز کی جانچ، بہترین پیرامیٹرز تلاش کرنا

- اتار چڑھاؤ، تجارتی حجم جیسے معاون فیصلہ سازی کے قواعد شامل کرنا

- مشین لرننگ کی تکنیک کا استعمال کرتے ہوئے اشاروں اور پیرامیٹرز کو متحرک طور پر بہتر بنانا

خلاصہ

دوہرا رجحان اتار چڑھاؤ کی حکمت عملی رجحان کی پیروی اور اتار چڑھاؤ کے اشاروں کے فوائد کو یکجا کرتی ہے، جو نہ صرف رجحان کی سمت کی شناخت کر سکتی ہے بلکہ اتار چڑھاؤ کے مواقع سے بھی فائدہ اٹھا سکتی ہے۔ پیرامیٹرز اور قواعد کی بہتری کے ذریعے حکمت عملی کی منافع بخش صلاحیت کو مزید بڑھایا جا سکتا ہے۔ اس حکمت عملی کے ترقی کے اچھے امکانات ہیں۔

- 1