سپر ٹرینڈ کی اعلیٰ حکمت عملی

خلاصہ

سپر ٹرینڈ ایڈوانسڈ حکمتِ عملی کلاسک سپر ٹرینڈ انڈیکیٹر کی اصلاح اور اپ گریڈ پر مبنی ہے۔ یہ قیمت کی حرکت، اتار چڑھاؤ اور متعدد تکنیکی اشاریوں کو یکجا کرتی ہے جس کا مقصد سگنل کے معیار کو بہتر بنانا، شور کو کم کرنا اور مارکیٹ کے رجحانات کی تبدیلی کو زیادہ درست طریقے سے پکڑنا ہے۔

حکمتِ عملی کا اصول

سپر ٹرینڈ ایڈوانسڈ حکمتِ عملی کا مرکز سپر ٹرینڈ لائن ہے۔ یہ حقیقی اتار چڑھاؤ کی حدود اور قیمت کی رفتار کی بنیاد پر شمار کیا جاتا ہے تاکہ ممکنہ قیمت کے رجحانات اور موڑ کے نکات کا اندازہ لگایا جا سکے۔ جب قیمت سپر ٹرینڈ لائن کے اوپر ہوتی ہے تو اس کا مطلب اوپر کا رجحان ہے، اور جب نیچے ہوتی ہے تو اس کا مطلب نیچے کا رجحان ہے۔

روایتی سپر ٹرینڈ انڈیکیٹر کے برعکس جو صرف اختتامی قیمت اور حقیقی اتار چڑھاؤ کی حدود پر غور کرتا ہے، ایڈوانسڈ حکمتِ عملی میں متعدد جہتوں جیسے تجارتی حجم، مومینٹم آسکیلیٹر اور بنیادی ڈیٹا کو بھی شامل کیا جاتا ہے تاکہ سگنل کی وشوسنییتا کی تصدیق ہو سکے۔ یہ کثیر متغیر طریقہ اس بات کو یقینی بناتا ہے کہ پیدا کردہ تجارتی سگنل زیادہ درست اور قابل اعتماد ہوں اور مارکیٹ کے شور سے متاثر نہ ہوں۔

فوائد کا تجزیہ

سپر ٹرینڈ ایڈوانسڈ حکمتِ عملی کے اہم فوائد یہ ہیں:

-

مارکیٹ کے رجحان کا زیادہ درست اندازہ لگانا اور جھوٹے بریک آؤٹ کو فلٹر کرنا۔ یہ حکمتِ عملی کئی عوامل کے اشاریوں کے یکساں ہونے کا انتظار کرتی ہے اس کے بعد تجارتی سگنل پیدا کرتی ہے، جس سے درستگی کی شرح میں بہت اضافہ ہو سکتا ہے۔

-

مارکیٹ کے شور کی مداخلت کو کم کرنا۔ فلٹرز کے مجموعی استعمال سے بہت سارے غیر اہم مارکیٹ ڈیٹا کو نظر انداز کیا جا سکتا ہے، جس سے فیصلے واضح ہو جاتے ہیں۔

-

رسک مینجمنٹ کو بہتر بنانا۔ صاف تجارتی سگنل تاجروں کو نقصان روکنے اور منافع کا تعین کرنے میں بہتر مدد دیتے ہیں، اس طرح رسک کنٹرول کی بہتر صلاحیت ملتی ہے۔

-

موافقت کی مضبوط صلاحیت۔ یہ حکمتِ عملی رجحان کی شناخت کے علاوہ دیگر تکنیکی آلات کے ساتھ بھی استعمال کی جا سکتی ہے تاکہ ایک جامع اور موثر تجارتی نظام تشکیل دیا جا سکے۔

خطرے کا تجزیہ

سپر ٹرینڈ ایڈوانسڈ حکمتِ عملی میں درج ذیل اہم خطرات بھی موجود ہیں:

-

پیرامیٹر سیٹنگ کا خطرہ۔ غلط اشاریوں کے پیرامیٹرز کا مجموعہ حکمتِ عملی کو ناکارہ بنا سکتا ہے یا بہت زیادہ غلط سگنل پیدا کر سکتا ہے۔

-

رجحان کی غلط تشخیص کا خطرہ۔ کوئی بھی حکمتِ عملی غلط تشخیص کے خطرے کو مکمل طور پر ختم نہیں کر سکتی، جب رجحان غیر متوقع طور پر تبدیل ہوتا ہے تو نقصان ہو سکتا ہے۔

-

حد سے زیادہ اصلاح (اوور آپٹیمائزیشن) کا خطرہ۔ جب پیرامیٹرز کو بہت زیادہ درست کیا جاتا ہے تو وہ تاریخی ڈیٹا پر بہت زیادہ انحصار کرنے لگتے ہیں اور مارکیٹ کی تبدیلیوں کے مطابق ڈھل نہیں سکتے۔

-

تجارتی لاگت کا خطرہ۔ جب تجارت کی تعداد بڑھ جاتی ہے تو تجارتی لاگت جیسے کمیشن اور سلپیج میں بھی واضح اضافہ ہوتا ہے۔

ان کے حل کے طریقے:

-

پیرامیٹرز کی بہترین ترتیب اور وقتاً فوقتاً بیک ٹیسٹنگ سے ان کی مضبوطی کی جانچ کرنا۔

-

نقصان روکنے اور منافع لینے کے آرڈر لگانا تاکہ ہر تجارت پر نقصان کو کنٹرول کیا جا سکے۔

-

حد سے زیادہ اصلاح سے بچنا اور پیرامیٹرز کی عمومیت (جنرلائزیشن) کی صلاحیت برقرار رکھنا۔

-

سگنل کے رسک-ریوارڈ تناسب کا حساب لگانا تاکہ تجارتی لاگت کو کنٹرول کیا جا سکے۔

بہتری کے رجحانات

سپر ٹرینڈ ایڈوانسڈ حکمتِ عملی کو درج ذیل پہلوؤں سے بہتر بنایا جا سکتا ہے:

-

مختلف مارکیٹوں کے مطابق پیرامیٹرز کو ایڈجسٹ کرنا تاکہ وہ اس مارکیٹ کی خصوصیات سے زیادہ مطابقت رکھیں۔ مثال کے طور پر اتار چڑھاؤ والی مارکیٹ میں حساب کے دورانیے کو کم کیا جا سکتا ہے۔

-

خودکار موافقت (ایڈاپٹیو) فلٹرنگ میکانزم شامل کرنا۔ جب مارکیٹ کسی خاص حالت میں داخل ہو تو پیرامیٹرز خود بخود ایڈجسٹ ہو جائیں یا کچھ فلٹرز غیر فعال ہو جائیں۔

-

مشین لرننگ کے طریقوں کو تلاش کرنا، نیورل نیٹ ورکس جیسے ماڈلز کو استعمال کرتے ہوئے پیرامیٹرز کو متحرک طور پر بہتر بنانا۔

-

جذباتی اشاریوں اور خبروں کی معلومات کو شامل کرنا تاکہ غیر ساختی ڈیٹا کا استعمال کرتے ہوئے کارکردگی میں اضافہ کیا جا سکے۔

-

ہدف کی پوزیشن کے سائز کا فنکشن شامل کرنا۔ جب جیتنے کی شرح بہت زیادہ ہو تو پوزیشن بڑھا کر زیادہ منافع حاصل کیا جا سکتا ہے۔

خلاصہ

سپر ٹرینڈ ایڈوانسڈ حکمتِ عملی متعدد فلٹرز اور تصدیقی اشاریوں کو شامل کرکے کلاسیکل سپر ٹرینڈ انڈیکیٹر کو بہتر اور اپ گریڈ کرتی ہے، جس سے مارکیٹ کے رجحان کو زیادہ درست طریقے سے پہچانا جا سکتا ہے اور سگنل کے معیار میں اضافہ ہوتا ہے۔ ایک ہی انڈیکیٹر کے مقابلے میں، یہ حکمتِ عملی زیادہ مضبوط، جامع اور موثر تجارتی حل فراہم کرتی ہے۔ تاہم، پیرامیٹرز کی غلط ترتیب اور غلط تشخیص کے خطرے سے بھی ہوشیار رہنا ضروری ہے اور مناسب رسک کنٹرول کے اقدامات اٹھانے چاہئیں۔ مزید بہتری اور دیگر آلات کے ساتھ استعمال کرنے سے، سپر ٹرینڈ ایڈوانسڈ حکمتِ عملی میں بہت زیادہ استعمال کی صلاحیت موجود ہے۔

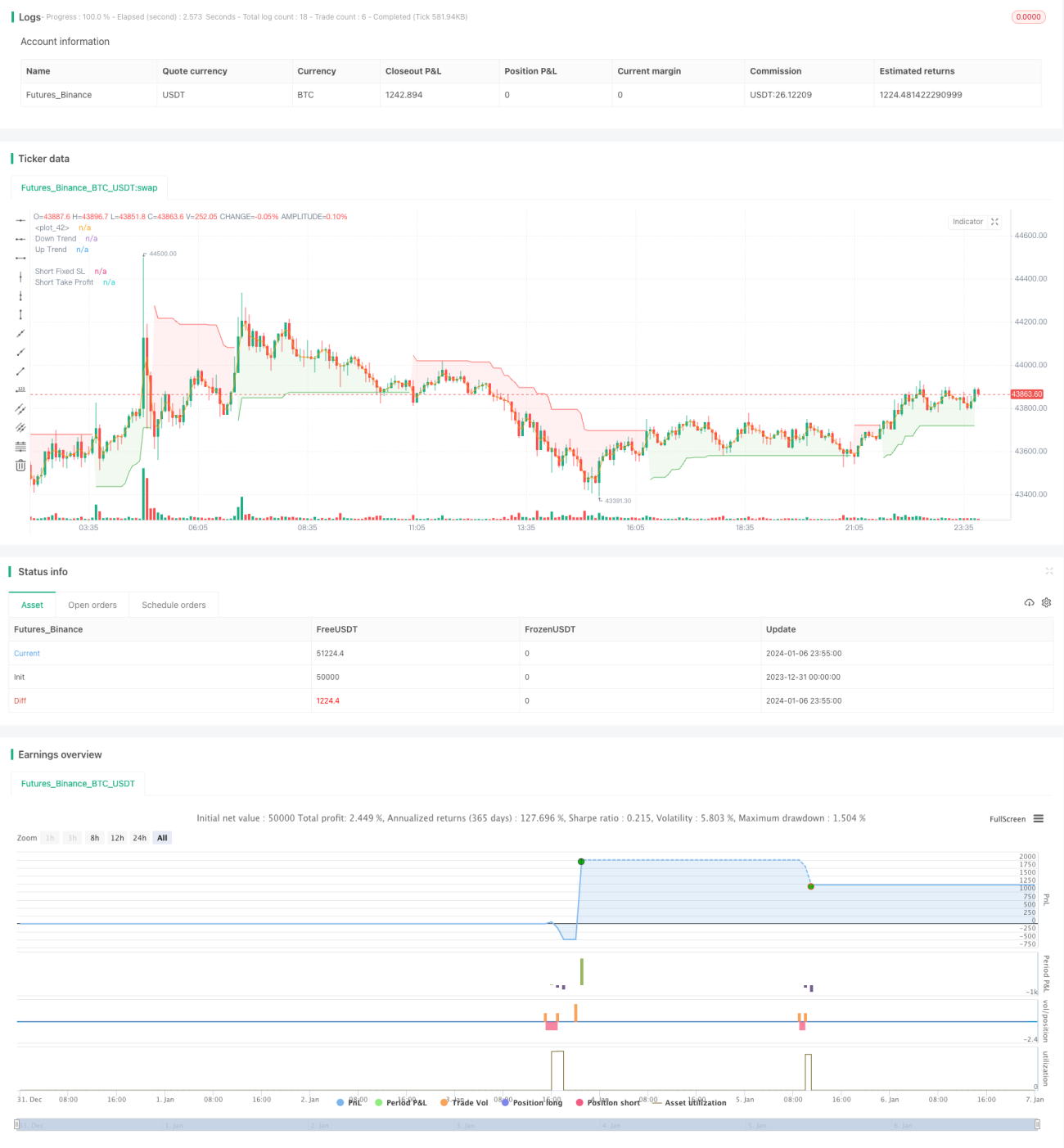

/*backtest

start: 2023-12-31 00:00:00

end: 2024-01-07 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © JS_TechTrading

//@version=5- 1