SSL پر مبنی موونگ ایوریج ٹرینڈ فالو کرنے کی حکمت عملی

خلاصہ

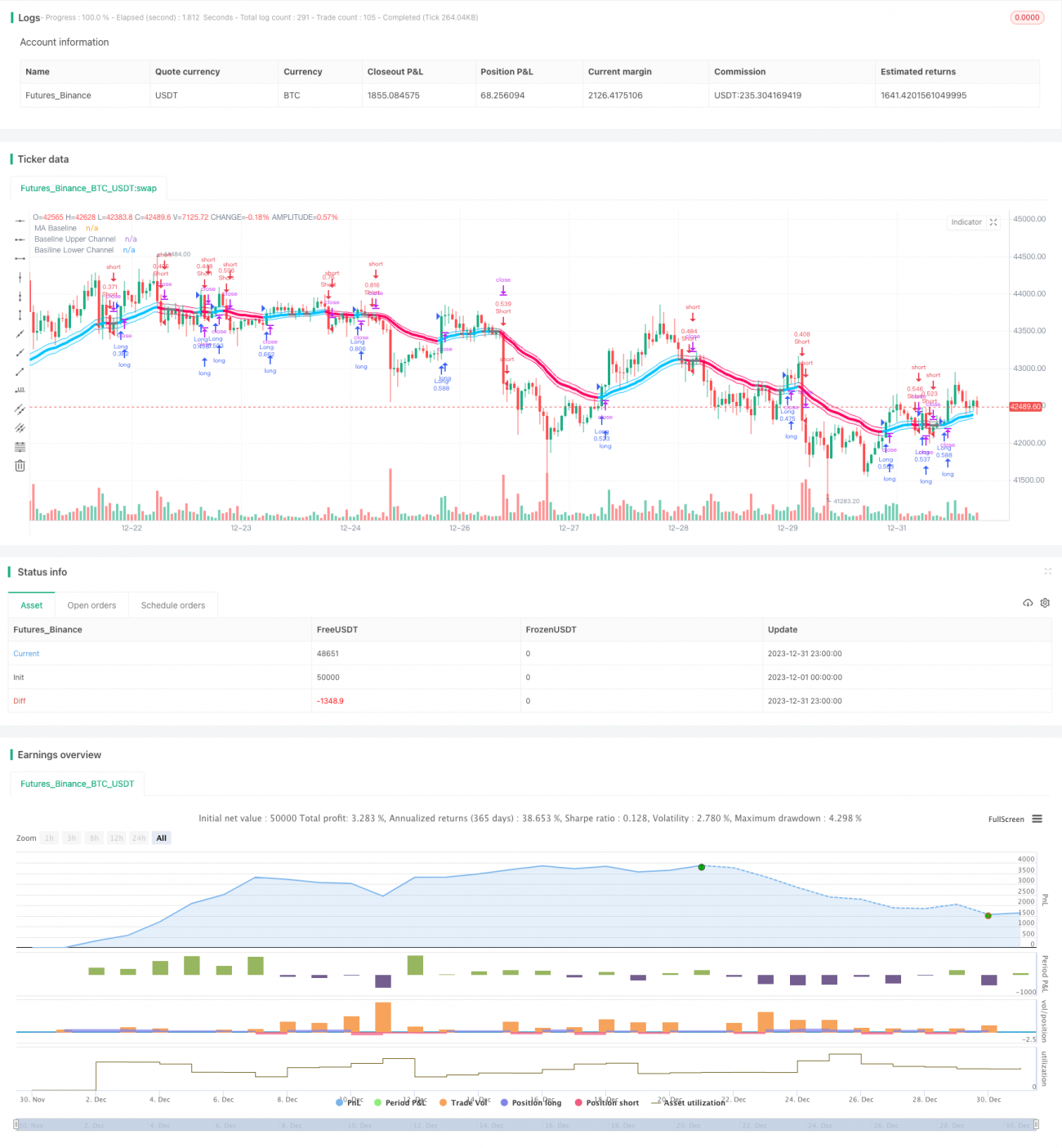

یہ حکمت عملی SSL چینل انڈیکیٹر کا استعمال کرتے ہوئے مارکیٹ کے رجحان کا اندازہ لگاتی ہے اور موونگ ایوریج کو بنیاد بنا کر رجحان کی پیروی کرتی ہے۔ یہ درمیانی سے طویل مدت کے 4 گھنٹے اور روزانہ چارٹس کے لیے موزوں ہے۔

حکمت عملی کے اصول

-

SSL چینل کیلٹنر موونگ ایوریج اور حقیقی اتار چڑھاؤ (True Range) سے تشکیل پاتا ہے۔ یہ مارکیٹ کے رجحان کی سمت کا تعین کرتا ہے۔ جب قیمت اوپری بینڈ کو توڑتی ہے تو یہ تیزی کا اشارہ ہے، اور جب نچلے بینڈ کو توڑتی ہے تو یہ مندی کا اشارہ ہے۔

-

حکمت عملی EMA جیسے موونگ ایوریج انڈیکیٹرز کا استعمال کرتے ہوئے ایک بنیادی موونگ ایوریج لائن کا حساب لگاتی ہے۔ یہ لائن کچھ جھوٹے بریک آؤٹ کو فلٹر کر سکتی ہے۔

-

حکمت عملی اس وقت لمبی پوزیشن (لانگ) لیتی ہے جب قیمت SSL کے اوپری بینڈ کو توڑتی ہے، اور اس وقت چھوٹی پوزیشن (شارٹ) لیتی ہے جب قیمت SSL کے نچلے بینڈ کو توڑتی ہے۔ بڑھتے ہوئے رجحان میں یہ تیزی کی پیروی کرتی ہے اور گرتے ہوئے رجحان میں نیچے سے خریدتی ہے۔

-

سٹاپ لاس کے طریقوں میں فیصدی سٹاپ لاس، ATR سٹاپ لاس، اور پچھلی کم ترین/بلند ترین قیمت پر مبنی سٹاپ لاس شامل ہیں۔ ٹیک پروفٹ سٹاپ لاس کا N گنا مقرر کیا جاتا ہے۔ مخصوص پیرامیٹرز صارف کی مرضی سے طے کیے جاتے ہیں۔

فوائد کا تجزیہ

-

SSL چینل رجحان کی سمت درست طریقے سے متعین کرتا ہے، جس سے جھوٹے سگنلز کم ہوتے ہیں۔ موونگ ایوریج کے ساتھ مل کر یہ مارکیٹ میں داخلے کی بنیاد فراہم کرتا ہے اور اوپر سے خریدنے یا نیچے سے بیچنے سے بچاتا ہے۔

-

مختلف اقسام کے موونگ ایوریجز کو منتخب کرنے کی لچک ہوتی ہے، جو مارکیٹ کے وسیع حالات کے مطابق ڈھل سکتی ہے۔

-

سٹاپ لاس کے طریقے لچک دار اور متنوع ہیں، جس سے خطرے پر قابو پایا جا سکتا ہے۔ ٹیک پروفٹ کا تناسب بھی لچک دار ہے، جو مختلف ترجیحات کو پورا کرتا ہے۔

-

ایک ہی وقت میں لمبی اور چھوٹی دونوں پوزیشنیں لی جا سکتی ہیں، جس سے مارکیٹ کے دو طرفہ مواقع سے بھرپور فائدہ اٹھایا جا سکتا ہے۔

خطرات کا تجزیہ

-

موونگ ایوریج انڈیکیٹرز میں تاخیر (Lag) ہوتی ہے، جس کی وجہ سے نقصان جمع ہو سکتا ہے۔

-

اتار چڑھاؤ والی مارکیٹ میں جیسے ہی اوپری یا نچلے بینڈ ٹوٹتے ہیں، قیمت الٹ سکتی ہے، جس سے پوزیشن پھنس سکتی ہے۔

-

غیر معمولی بریک آؤٹ میں ATR اور پچھلی قیمتوں پر مبنی سٹاپ لاس بہت ڈھیلے ہو سکتے ہیں، جس سے نقصان بڑھ سکتا ہے۔

خطرات سے نمٹنے کے اقدامات:

- موونگ ایوریج کے پیرامیٹرز کو مناسب طریقے سے ایڈجسٹ کریں، یا دیگر اقسام کے موونگ ایوریجز منتخب کریں۔

- سٹاپ لاس کی حد بڑھا دیں اور بروقت سٹاپ لاس لگائیں۔

- ATR میں ضرب (multiplicative factor) شامل کریں، یا پچھلی قیمتوں کے حساب کے دورانیے کو ایڈجسٹ کریں۔

بہتری کے ممکنہ پہلو

- موونگ ایوریج انڈیکیٹرز کی مزید اقسام کی جانچ کریں اور بہترین پیرامیٹرز تلاش کریں۔

- سٹاپ لاس کے ATR دورانیے کے پیرامیٹرز کو بہتر بنائیں۔

- مختلف سٹاپ لاس کے ضربی پیرامیٹرز کی جانچ کریں۔

- مختلف ٹیک پروفٹ رسک کوفیشینٹس کی جانچ کریں۔

خلاصہ

یہ حکمت عملی SSL کے ذریعے رجحان کا اندازہ لگانے اور موونگ ایوریج انڈیکیٹرز کے ذریعے مارکیٹ میں داخلے کی تصدیق کرنے کا مؤثر طریقہ فراہم کرتی ہے، جو رجحان کی مؤثر پیروی کر سکتی ہے۔ یہ لچک دار سٹاپ لاس اور ٹیک پروفٹ کے طریقے پیش کرتی ہے، جو خطرے پر قابو پانے کے ساتھ ساتھ زیادہ منافع حاصل کرنے میں مدد دیتی ہے۔ مسلسل جانچ اور پیرامیٹرز کی بہتری کے ذریعے بہتر تجارتی کارکردگی حاصل کی جا سکتی ہے۔ یہ ایک مؤثر حکمت عملی ہے جسے طویل مدت تک فالو کیا جا سکتا ہے اور استعمال کیا جا سکتا ہے۔

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// Thanks to @kevinmck100 for opensource strategy template and @Mihkel00 for SSL Hybrid

// @fpemehd

// @version=5- 1