تین موونگ ایوریج اور MACD کا مجموعہ مقداری حکمت عملی

جائزہ

یہ حکمت عملی تین گنا مووونگ ایوریج اور MACD انڈیکیٹر کے امتزاج سے ایک مستحکم اور قابل اعتماد مقداری تجارتی حکمت عملی تیار کرتی ہے۔ اس حکمت عملی کا مقصد مستقبل میں ممکنہ رجحانات کو پکڑنا ہے، اور یہ خاص طور پر درمیانی سے طویل مدتی پوزیشنوں کے لیے موزوں ہے۔

حکمت عملی کا اصول

یہ حکمت عملی بنیادی طور پر تین گنا مووونگ ایوریج اور MACD انڈیکیٹر کے امتزاج پر مبنی ہے۔

سب سے پہلے، حکمت عملی میں بالترتیب 3، 7 اور 2 کی لمبائی کے ساتھ تین گنا ایکسپونینشل مووونگ ایوریج استعمال کی گئی ہیں۔ یہ تین مووونگ ایوریج ایک تیز سے سست مووونگ ایوریج سسٹم تشکیل دیتے ہیں، جو مستقبل کے رجحان کی سمت کا تعین کرنے کے لیے استعمال ہوتا ہے۔ جب قلیل مدتی مووونگ ایوریج طویل مدتی مووونگ ایوریج کو اوپر سے کراس کرتی ہے تو یہ خرید کا سگنل ہوتا ہے، اور جب قلیل مدتی مووونگ ایوریج طویل مدتی مووونگ ایوریج کو نیچے سے کراس کرتی ہے تو یہ فروخت کا سگنل ہوتا ہے۔

دوم، حکمت عملی میں 3 اور 7 کے پیرامیٹرز کے ساتھ MACD انڈیکیٹر بھی استعمال کیا گیا ہے۔ جب MACD مین لائن سگنل لائن کو اوپر سے کراس کرتی ہے تو خرید کا سگنل ہوتا ہے، اور نیچے سے کراس کرنے پر فروخت کا سگنل ہوتا ہے۔

دہری انڈیکیٹرز کے امتزاج سے ایک ہی انڈیکیٹر کی وجہ سے پیدا ہونے والے متعدد غلط سگنلز سے بچا جا سکتا ہے، جس سے حکمت عملی کے استحکام میں اضافہ ہوتا ہے۔

حکمت عملی کے فوائد

- دہری انڈیکیٹرز کے ذریعے فلٹرنگ، سگنل کے معیار میں اضافہ

- پیرامیٹرز کو متعدد بار جانچ اور بہتر بنایا گیا ہے، مستحکم اور قابل اعتماد

- تین گنا مووونگ ایوریج سسٹم مارکیٹ کے شور کو مؤثر طریقے سے فلٹر کرنے اور مستقبل کے رجحان کا تعین کرنے میں مدد دیتا ہے

- MACD انڈیکیٹر کے پیرامیٹرز تیز رفتار ہیں، جو قلیل مدتی مواقع کو جلدی پکڑ سکتے ہیں

حکمت عملی کے خطرات

- کچھ حد تک کمی اور مسلسل نقصان کا خطرہ

- جب مارکیٹ میں واضح رجحان نہ ہو تو یہ حکمت عملی زیادہ غلط تجارت کرتی ہے

- MACD انڈیکیٹر آسانی سے غلط سگنل پیدا کر سکتا ہے، اس لیے اسے مووونگ ایوریج انڈیکیٹر کے ساتھ ملا کر استعمال کرنا چاہیے

حل کے طریقے:

- مناسب اسٹاپ لاس حکمت عملی اپناتے ہوئے زیادہ سے زیادہ کمی کو کنٹرول کریں

- جب Market State واضح طور پر بے رجحان ہو تو تجارت کی تعدد کم کریں

- MACD کے پیرامیٹرز کو بہتر بنائیں اور دوسرے انڈیکیٹرز کے ساتھ ملا کر استعمال کریں

حکمت عملی کی بہتری کے رخ

- مووونگ ایوریج اور MACD کے پیرامیٹرز کو جانچیں اور بہتر بنائیں تاکہ بہترین مجموعہ تلاش کیا جا سکے

- KDJ، VRSI جیسے معاون انڈیکیٹرز شامل کریں تاکہ غلط سگنلز سے بچا جا سکے

- مارکیٹ کی حالت کا اندازہ لگانے کے لیے مشین لرننگ ماڈل شامل کریں تاکہ متحرک ایڈجسٹمنٹ ممکن ہو

- اسٹاپ لاس حکمت عملی کے ساتھ ملا کر بہترین اسٹاپ لاس پوائنٹس مرتب کریں

خلاصہ

یہ حکمت عملی مووونگ ایوریج اور MACD کے امتزاج کے ذریعے مستحکم رجحان گرفتاری حاصل کرتی ہے۔ اس کا فائدہ انڈیکیٹرز کے مشترکہ استعمال میں ہے، جو غلط سگنلز کو مؤثر طریقے سے کم کرتا ہے، جس کے نتیجے میں بہتر حکمت عملی کارکردگی حاصل ہوتی ہے۔ اگلے مرحلے میں، پیرامیٹر کی بہتری، اسٹاپ لاس حکمت عملی کا اضافہ، اور متحرک ایڈجسٹمنٹ جیسے ذرائع سے اس حکمت عملی کو مزید بہتر بنایا جائے گا تاکہ یہ درمیانی سے طویل مدتی مواقع تلاش کرنے کا ایک مؤثر ذریعہ بن سکے۔

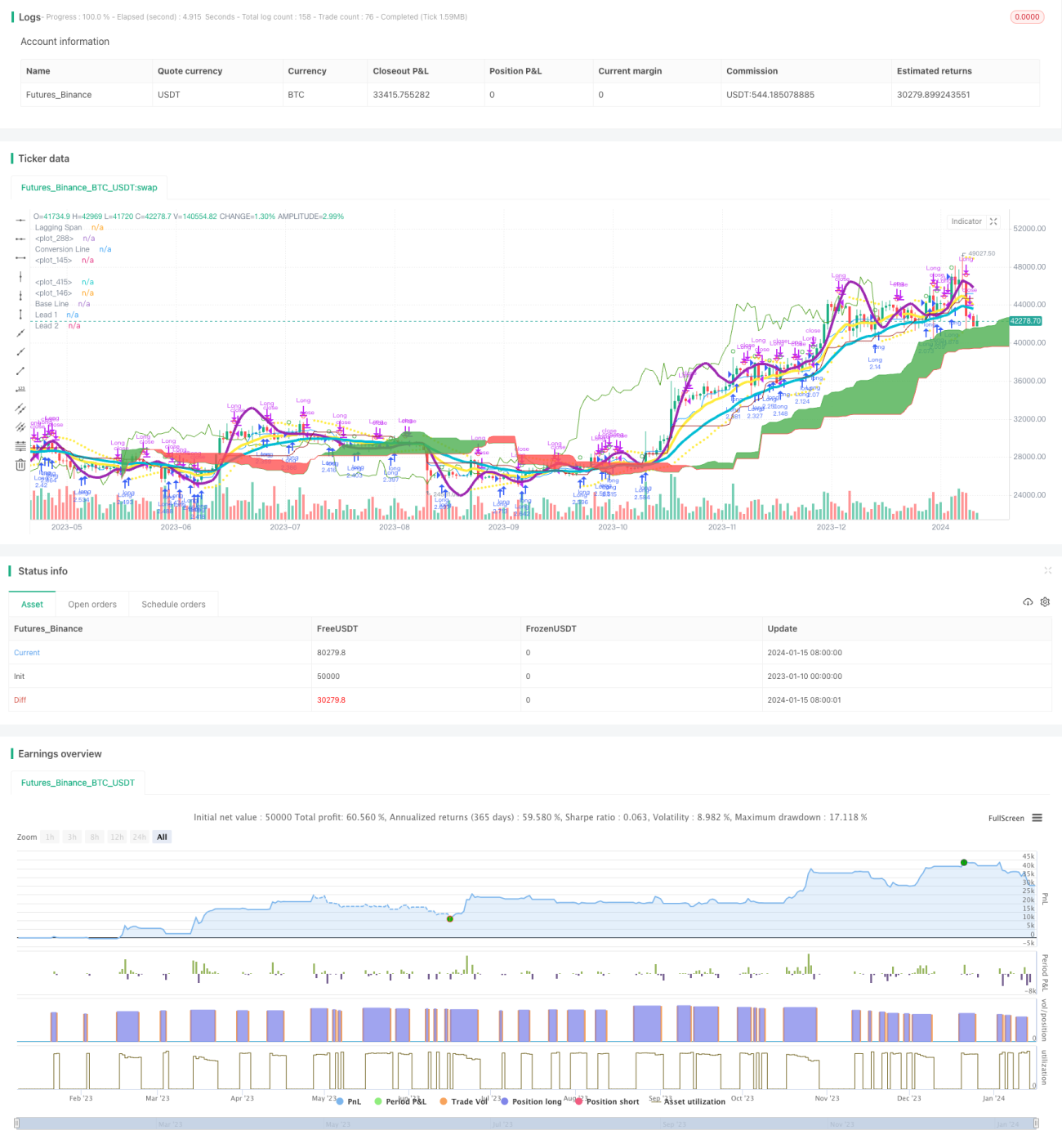

/*backtest

start: 2023-01-10 00:00:00

end: 2024-01-16 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

strategy("Matt's MACD Algo v1", shorttitle="Matt's MACD Algo v1", overlay=true, pyramiding = 0, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, initial_capital=7000, calc_on_order_fills = true, commission_type=strategy.commission.percent, commission_value=0, currency = currency.USD)

//study("MFI Fresh", shorttitle="MFI Fresh", overlay=true)

- 1