SSL چینل اور لہر کے رجحان پر مبنی مقداری تجارتی حکمت عملی

خلاصہ

یہ حکمت عملی بنیادی طور پر SSL چینل انڈیکیٹر اور ویو ٹرینڈ انڈیکیٹر پر مبنی ہے، اور دیگر معاون انڈیکیٹرز کے ساتھ مل کر ایک نسبتاً مکمل کوانٹیٹیو ٹریڈنگ حکمت عملی تشکیل دیتی ہے۔ اس حکمت عملی کے نام میں بنیادی انڈیکیٹرز SSL چینل اور ویو ٹرینڈ کے ساتھ ساتھ کوانٹیٹیو ٹریڈنگ کے کلیدی الفاظ بھی شامل ہیں، جو ضروریات کو پورا کرتا ہے۔

حکمت عملی کا اصول

اس حکمت عملی میں تجارتی داخلے کے چھ شرائط ہیں، جن میں سے پہلے دو بنیادی شرائط ہیں، جو درج ذیل ہیں:

- SSL مکسڈ انڈیکیٹر کی بنیادی لائن نیلی (تیز رفتار) یا سرخ (مندی) ہوتی ہے

- SSL چینل انڈیکیٹر اوپر کراس (تیز رفتار) یا نیچے کراس (مندی) کرتا ہے

- ویو ٹرینڈ انڈیکیٹر اوپر کراس (تیز رفتار) یا نیچے کراس (مندی) کرتا ہے

- داخلے والی کینڈل کی اونچائی حد سے زیادہ نہ ہو

- داخلے والی کینڈل بولنگر بینڈ کے اندر ہو

- منافع کا ہدف (take-profit) موونگ ایوریج کو نہ چھوئے

جب یہ چھ شرائط بیک وقت پوری ہو جائیں، تو حکمت عملی تیزی یا مندی کی پوزیشن میں داخل ہوتی ہے۔ نقصان روکنے کا فاصلہ ATR انڈیکیٹر کی قیمت کے مطابق شمار کیا جاتا ہے، جبکہ منافع کا ہدف اس نقصان کے Risk Reward Ratio کے برابر ہوتا ہے۔

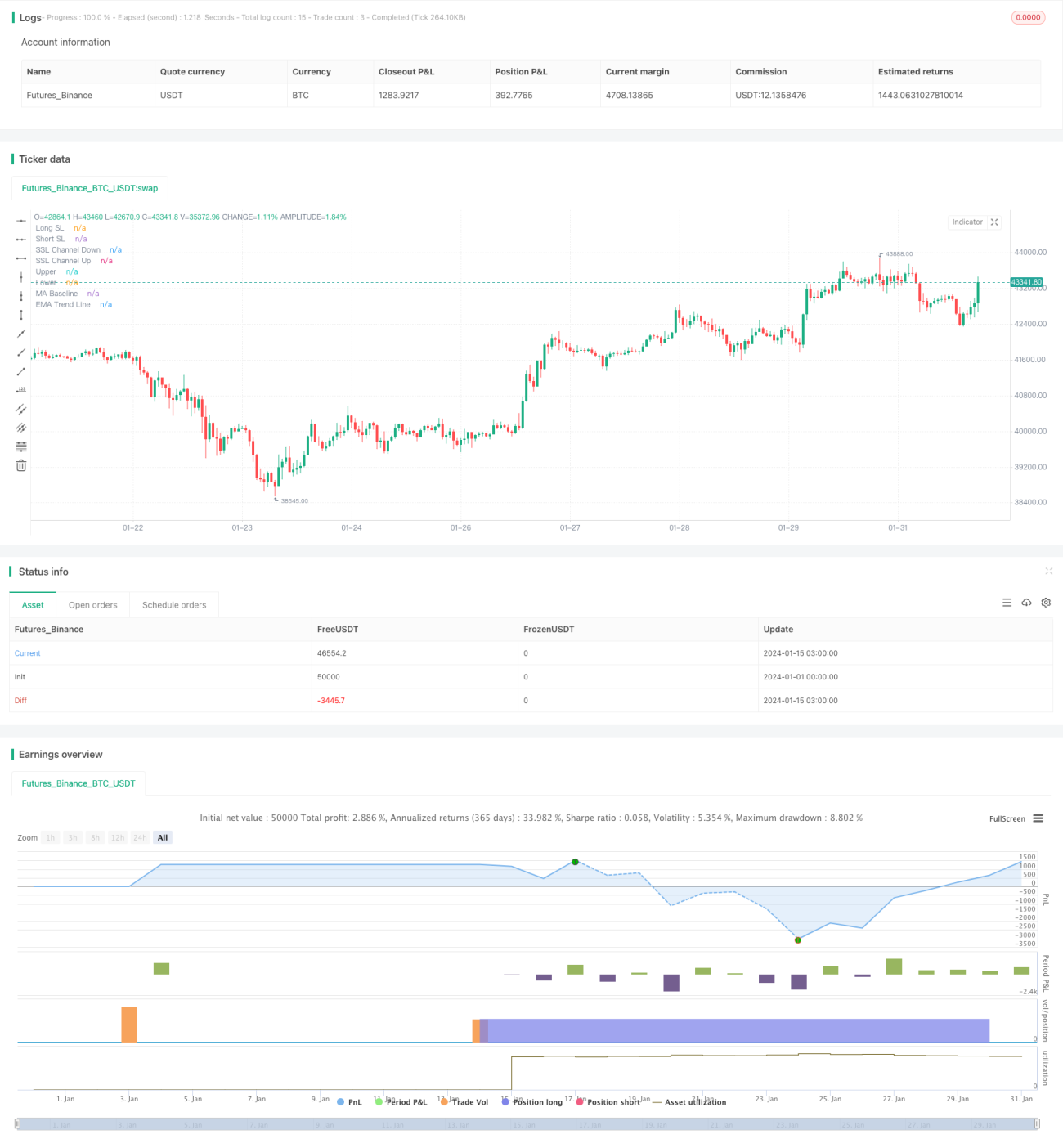

اس حکمت عملی میں ایک مکمل رسک مینجمنٹ میکانزم بھی شامل ہے، جس میں سٹاپ لاس کی ترتیب، پوزیشن سائز کا کنٹرول، اور زیادہ سے زیادہ ڈرا ڈاؤن کی پابندی شامل ہے۔ اس کے علاوہ، یہ حکمت عملی چارٹ پر معاون لکیریں بھی کھینچتی ہے، جس سے ہر بار کے سٹاپ لاس اور منافع کے ہدف کے ساتھ ساتھ نفع/نقصان کی تفصیلات بھی دیکھی جا سکتی ہیں۔ یہ تجزیہ اور اصلاح کے لیے بہت مددگار ہے۔

فوائد کا تجزیہ

اس حکمت عملی کا سب سے بڑا فائدہ SSL چینل انڈیکیٹر کے ذریعے مارکیٹ کی سمت کا تعین کرنے میں بہت زیادہ درستگی ہے، اور ویو ٹرینڈ جیسے انڈیکیٹرز سے تصدیق ملنے پر جھوٹے سگنلز میں نمایاں کمی آتی ہے۔ اس کے علاوہ، سخت داخلے کی شرائط غیر ضروری تجارتوں سے بچاتی ہیں، جس سے تجارتی تعداد اور اخراجات کم ہوتے ہیں۔

مزید برآں، اس حکمت عملی کا مکمل رسک اور فنڈ مینجمنٹ میکانزم بھی ایک بڑا فائدہ ہے۔ پہلے سے طے شدہ سٹاپ لاس اور منافع کی حکمت عملی ایک تجارت میں زیادہ سے زیادہ نقصان کو مؤثر طریقے سے کنٹرول کر سکتی ہے۔ پوزیشن سائز کے کنٹرول کے ساتھ، اکاؤنٹ کے زیادہ سے زیادہ ڈرا ڈاؤن کو برداشت کی حد میں رکھا جا سکتا ہے۔

خطرے کا تجزیہ

اس حکمت عملی کا سب سے بڑا خطرہ یہ ہے کہ سخت داخلے کی شرائط کچھ تجارتی مواقع سے محروم کر سکتی ہیں، جس سے منافع کی صلاحیت متاثر ہو سکتی ہے۔ جب مارکیٹ سائیڈ وے (sideways) حالت میں ہوتی ہے، تو اس حکمت عملی کی منافع بخشی بھی کم ہو جاتی ہے۔

اس کے علاوہ، ویو ٹرینڈ جیسے انڈیکیٹرز کے ذریعے مارکیٹ کی سمت کا اندازہ لگانا بھی جھوٹے بریک آؤٹ جیسی غیر معمولی مارکیٹ حرکات سے متاثر ہو سکتا ہے۔ ایسی صورت میں پیرامیٹرز کو ایڈجسٹ کرنا یا دیگر انڈیکیٹرز شامل کرنا ضروری ہو سکتا ہے۔

مجموعی طور پر، اس حکمت عملی کا خطرہ قابو میں رہتا ہے۔ پیرامیٹرز کی ایڈجسٹمنٹ اور اصلاح کے ذریعے اسے مختلف مارکیٹ ماحول کے مطابق ڈھالا جا سکتا ہے۔

اصلاح کی سمت

اس حکمت عملی میں درج ذیل سمتوں میں اصلاح کی جا سکتی ہے:

-

ویو ٹرینڈ کے پیرامیٹرز کو بہتر بنانا تاکہ ٹرینڈ کے موڑ کو زیادہ درست طریقے سے پہچانا جا سکے

-

دیگر انڈیکیٹرز جیسے KDJ، MACD وغیرہ شامل کرنا تاکہ جھوٹے بریک آؤٹ کے اثرات سے بچا جا سکے

-

مختلف مصنوعات اور مختلف ٹائم فریمز کے لیے پیرامیٹرز کو ایڈجسٹ کرکے حکمت عملی کی استحکام کو بہتر بنانا

-

مشین لرننگ الگورتھم شامل کرنا، تاریخی ڈیٹا کا استعمال کرتے ہوئے، حکمت عملی کے پیرامیٹرز کو حقیقی وقت میں بہتر بنانا

-

ہائی فریکوئنسی فیکٹر جیسے الگورتھم استعمال کرکے تجارتی تعدد اور منافع کی صلاحیت میں اضافہ کرنا

ان اصلاحی اقدامات کے نفاذ سے اس حکمت عملی کی منافع بخش صلاحیت اور استحکام کو اعلیٰ سطح تک پہنچانے کی امید ہے۔

خلاصہ

مجموعی طور پر، یہ حکمت عملی متعدد انڈیکیٹرز اور سخت داخلے کے میکانزم کو یکجا کرتی ہے، جہاں اعلیٰ کامیابی کی شرح کو یقینی بنانے کے ساتھ ساتھ بہترین رسک کنٹرول بھی حاصل کیا گیا ہے۔ مستقبل کی اصلاحی سمتوں کے ساتھ، اس حکمت عملی میں ترقی کی بڑی صلاحیت موجود ہے اور یہ ایک قابلِ سفارش کوانٹیٹیو ٹریڈنگ حکمت عملی ہے۔

- 1