Chiến lược EMA hai dạng đa dạng tiền tệ kỹ thuật số (Hướng dẫn)

Tác giả:Lydia., Tạo: 2022-11-08 12:50:56, Cập nhật: 2023-09-15 20:57:25

Theo yêu cầu của người dùng cộng đồng muốn có một chiến lược EMA đôi đa dạng để tham khảo thiết kế. Trong bài viết này, chúng tôi sẽ thực hiện một chiến lược EMA đôi đa dạng. Các bình luận sẽ được viết về mã chiến lược để dễ dàng hiểu và học. Hãy để nhiều người mới đến lập trình và giao dịch định lượng có được một khởi đầu nhanh chóng.

Ý tưởng chiến lược

Lý thuyết của chiến lược EMA đôi rất đơn giản, đó là hai EMA. Một EMA (đường nhanh) với khoảng thời gian tham số nhỏ và một EMA (đường chậm) với khoảng thời gian tham số lớn. Nếu hai đường có đường chéo vàng (đường nhanh đi qua đường chậm từ dưới lên trên), thì chúng ta mua và mua dài; và nếu hai đường có đường chéo chết (đường nhanh đi qua đường chậm từ trên xuống dưới), thì chúng ta bán và mua ngắn. Chúng ta sử dụng EMA ở đây.

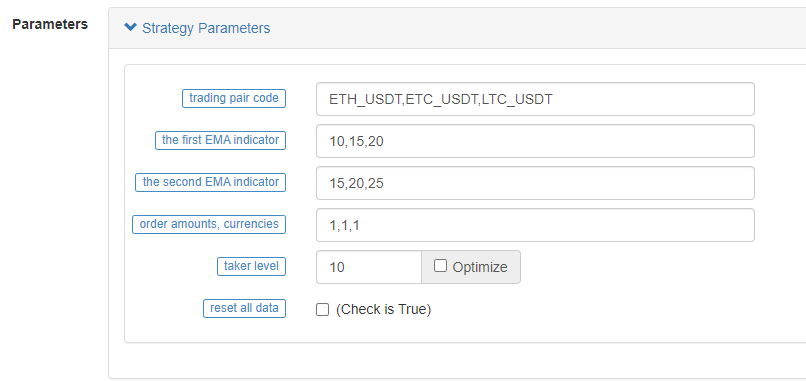

Tuy nhiên, chiến lược nên được thiết kế như nhiều giống, vì vậy các thông số của mỗi giống có thể khác nhau (các giống khác nhau sử dụng các thông số EMA khác nhau), vì vậy một phương pháp

Các tham số được thiết kế theo dạng chuỗi, với mỗi tham số tách ra dấu phẩy. Phân tích các chuỗi này khi chiến lược bắt đầu chạy. Logic thực thi phù hợp với mỗi biến thể (cặp giao dịch). Chiến lược xoay phát hiện thị trường của mỗi biến thể, kích hoạt điều kiện giao dịch, in biểu đồ, v.v. Sau khi tất cả các biến thể được xoay một lần, tóm tắt dữ liệu và hiển thị thông tin bảng trên thanh trạng thái.

Chiến lược được thiết kế rất đơn giản và phù hợp với người mới đến học, với tổng cộng chỉ có hơn 200 dòng mã.

Mã chiến lược

// Function: cancel all takers of the current trading pair

function cancelAll(e) {

while (true) {

var orders = _C(e.GetOrders)

if (orders.length == 0) {

break

} else {

for (var i = 0 ; i < orders.length ; i++) {

e.CancelOrder(orders[i].Id, orders[i])

Sleep(500)

}

}

Sleep(500)

}

}

// Functionn: calculate the profit/loss in real-time

function getProfit(account, initAccount, lastPrices) {

// account is the current account information, initAccount is the initial account information, lastPrices is the latest price of all varieties

var sum = 0

_.each(account, function(val, key) {

// Iterate through all current assets, calculate the currency difference of assets other than USDT, and the amount difference

if (key != "USDT" && typeof(initAccount[key]) == "number" && lastPrices[key + "_USDT"]) {

sum += (account[key] - initAccount[key]) * lastPrices[key + "_USDT"]

}

})

// Return to the profit and loss of the asset based on the current prices

return account["USDT"] - initAccount["USDT"] + sum

}

// Function: generate chart configuration

function createChartConfig(symbol, ema1Period, ema2Period) {

// symbol is the trading pair, ema1Period is the first EMA period, ema2Period is the second EMA period

var chart = {

__isStock: true,

extension: {

layout: 'single',

height: 600,

},

title : { text : symbol},

xAxis: { type: 'datetime'},

series : [

{

type: 'candlestick', // K-line data series

name: symbol,

id: symbol,

data: []

}, {

type: 'line', // EMA data series

name: symbol + ',EMA1:' + ema1Period,

data: [],

}, {

type: 'line', // EMA data series

name: symbol + ',EMA2:' + ema2Period,

data: []

}

]

}

return chart

}

function main() {

// Reset all data

if (isReset) {

_G(null) // Clear data of all persistent records

LogReset(1) // Clear all logs

LogProfitReset() // Clear all return logs

LogVacuum() //Release the resources occupied by the real bot database

Log("Reset all data", "#FF0000") // Print messages

}

// Parameter analysis

var arrSymbols = symbols.split(",") // Comma-separated string of trading varieties

var arrEma1Periods = ema1Periods.split(",") // Parameter string for splitting the first EMA

var arrEma2Periods = ema2Periods.split(",") // Parameter string for splitting the second EMA

var arrAmounts = orderAmounts.split(",") // Splitting the amount of orders placed for each variety

var account = {} // Variables used for recording current asset messages

var initAccount = {} // Variables used for recording initial asset messages

var currTradeMsg = {} // Variables used for recording whether current BAR trades

var lastPrices = {} // Variables used for recording the latest price of monitored varieties

var lastBarTime = {} // Variable used for recording the time of the last BAR, used to judge the update of BAR when drawing

var arrChartConfig = [] // Used for recording chart configuration message and draw

if (_G("currTradeMsg")) { // For example, restore currTradeMsg data when restarting

currTradeMsg = _G("currTradeMsg")

Log("Restore records", currTradeMsg)

}

// Initialize account

_.each(arrSymbols, function(symbol, index) {

exchange.SetCurrency(symbol)

var arrCurrencyName = symbol.split("_")

var baseCurrency = arrCurrencyName[0]

var quoteCurrency = arrCurrencyName[1]

if (quoteCurrency != "USDT") {

throw "only support quoteCurrency: USDT"

}

if (!account[baseCurrency] || !account[quoteCurrency]) {

cancelAll(exchange)

var acc = _C(exchange.GetAccount)

account[baseCurrency] = acc.Stocks

account[quoteCurrency] = acc.Balance

}

// Initialize chart-related data

lastBarTime[symbol] = 0

arrChartConfig.push(createChartConfig(symbol, arrEma1Periods[index], arrEma2Periods[index]))

})

if (_G("initAccount")) {

initAccount = _G("initAccount")

Log("Restore initial account records", initAccount)

} else {

// Initialize the initAccount variable with the current asset information

_.each(account, function(val, key) {

initAccount[key] = val

})

}

Log("account:", account, "initAccount:", initAccount) // Print asset information

// Initialize the chart object

var chart = Chart(arrChartConfig)

// Chart reset

chart.reset()

// Strategy main loop logic

while (true) {

// Iterate through all varieties and execute the double-EMA logic one by one

_.each(arrSymbols, function(symbol, index) {

exchange.SetCurrency(symbol) // Switch the trading pair to the trading pair of symbol string record

var arrCurrencyName = symbol.split("_") // Split the trading pairs with the "_" symbol

var baseCurrency = arrCurrencyName[0] // String for trading currencies

var quoteCurrency = arrCurrencyName[1] // String for denominated currency

// Obtain the EMA parameters of the current trading pair according to the index

var ema1Period = parseFloat(arrEma1Periods[index])

var ema2Period = parseFloat(arrEma2Periods[index])

var amount = parseFloat(arrAmounts[index])

// Obtain the K-line data of the current trading pair

var r = exchange.GetRecords()

if (!r || r.length < Math.max(ema1Period, ema2Period)) { // Return directly if K-line length is insufficient

Sleep(1000)

return

}

var currBarTime = r[r.length - 1].Time // Record the current BAR timestamp

lastPrices[symbol] = r[r.length - 1].Close // Record the latest current price

var ema1 = TA.EMA(r, ema1Period) // Calculate EMA indicators

var ema2 = TA.EMA(r, ema2Period) // Calculate EMA indicators

if (ema1.length < 3 || ema2.length < 3) { // The length of EMA indicator array is too short, return directly

Sleep(1000)

return

}

var ema1Last2 = ema1[ema1.length - 2] // EMA on the penultimate BAR

var ema1Last3 = ema1[ema1.length - 3] // EMA on the third from the last BAR

var ema2Last2 = ema2[ema2.length - 2]

var ema2Last3 = ema2[ema2.length - 3]

// Write data to the chart

var klineIndex = index + 2 * index

// Iterate through the K-line data

for (var i = 0 ; i < r.length ; i++) {

if (r[i].Time == lastBarTime[symbol]) { // Draw the chart, update the current BAR and indicators

// update

chart.add(klineIndex, [r[i].Time, r[i].Open, r[i].High, r[i].Low, r[i].Close], -1)

chart.add(klineIndex + 1, [r[i].Time, ema1[i]], -1)

chart.add(klineIndex + 2, [r[i].Time, ema2[i]], -1)

} else if (r[i].Time > lastBarTime[symbol]) { // Draw the charts, add BARs and indicators

// add

lastBarTime[symbol] = r[i].Time // Update timestamp

chart.add(klineIndex, [r[i].Time, r[i].Open, r[i].High, r[i].Low, r[i].Close])

chart.add(klineIndex + 1, [r[i].Time, ema1[i]])

chart.add(klineIndex + 2, [r[i].Time, ema2[i]])

}

}

if (ema1Last3 < ema2Last3 && ema1Last2 > ema2Last2 && currTradeMsg[symbol] != currBarTime) {

// Golden cross

var depth = exchange.GetDepth() // Obtain the depth data of current order book

var price = depth.Asks[Math.min(takeLevel, depth.Asks.length)].Price // Take the 10th grade price, taker

if (depth && price * amount <= account[quoteCurrency]) { // Obtain deep data normally with enough assets to place an order

exchange.Buy(price, amount, ema1Last3, ema2Last3, ema1Last2, ema2Last2) // Place a buy order

cancelAll(exchange) // Cancel all makers

var acc = _C(exchange.GetAccount) // Obtain account asset information

if (acc.Stocks != account[baseCurrency]) { // Detect changes in account assets

account[baseCurrency] = acc.Stocks // Update assets

account[quoteCurrency] = acc.Balance // Update assets

currTradeMsg[symbol] = currBarTime // Record that the current BAR has been traded

_G("currTradeMsg", currTradeMsg) // Persistent records

var profit = getProfit(account, initAccount, lastPrices) // Calculate profits

if (profit) {

LogProfit(profit, account, initAccount) // Print profits

}

}

}

} else if (ema1Last3 > ema2Last3 && ema1Last2 < ema2Last2 && currTradeMsg[symbol] != currBarTime) {

// dead cross

var depth = exchange.GetDepth()

var price = depth.Bids[Math.min(takeLevel, depth.Bids.length)].Price

if (depth && amount <= account[baseCurrency]) {

exchange.Sell(price, amount, ema1Last3, ema2Last3, ema1Last2, ema2Last2)

cancelAll(exchange)

var acc = _C(exchange.GetAccount)

if (acc.Stocks != account[baseCurrency]) {

account[baseCurrency] = acc.Stocks

account[quoteCurrency] = acc.Balance

currTradeMsg[symbol] = currBarTime

_G("currTradeMsg", currTradeMsg)

var profit = getProfit(account, initAccount, lastPrices)

if (profit) {

LogProfit(profit, account, initAccount)

}

}

}

}

Sleep(1000)

})

// Table variables in the status bar

var tbl = {

type : "table",

title : "Account Information",

cols : [],

rows : []

}

// Write data into the status bar table structure

tbl.cols.push("--")

tbl.rows.push(["initial"])

tbl.rows.push(["current"])

_.each(account, function(val, key) {

if (typeof(initAccount[key]) == "number") {

tbl.cols.push(key)

tbl.rows[0].push(initAccount[key]) // initial

tbl.rows[1].push(val) // current

}

})

// Show status bar table

LogStatus(_D(), "\n", "profit:", getProfit(account, initAccount, lastPrices), "\n", "`" + JSON.stringify(tbl) + "`")

}

}

Kiểm tra lại chiến lược

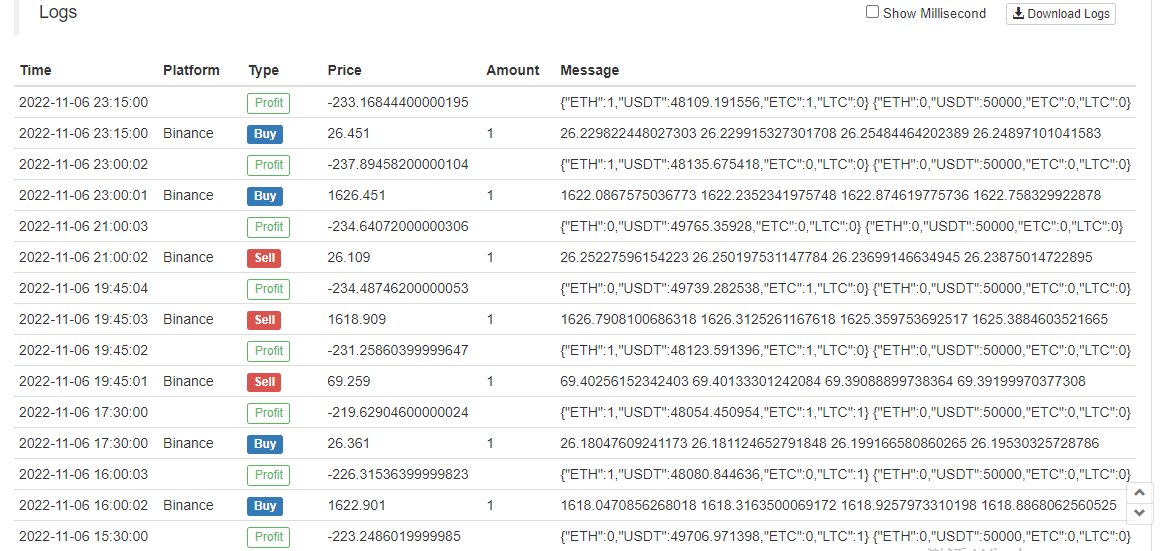

Có thể thấy rằng ETH, LTC và ETC được kích hoạt theo Golden Cross và Dead Cross của EMA, và giao dịch đã xảy ra.

Chúng ta cũng có thể lấy một robot mô phỏng để thử nghiệm.

Mã nguồn chiến lược:https://www.fmz.com/strategy/333783

Chiến lược được sử dụng cho backtesting, chỉ thiết kế chiến lược học tập, và nó nên được sử dụng một cách thận trọng trong bot thực sự.