Chiến lược theo xu hướng vững như bàn thạch

Tổng quan

Chiến lược này dựa trên sự kết hợp của SSL Hỗn Hợp Channel, QQE Cải Tiến và chỉ báo Vadaata Breakout, tạo nên một chiến lược bắt xu hướng vững chắc. Nó có thể mang lại lợi nhuận ổn định trên các loại tiền điện tử lớn như BTC và ETH, phù hợp cho giao dịch trung và dài hạn.

Nguyên lý chiến lược

Logic vào lệnh

Điều kiện vào lệnh mua (Long):

- Giá đóng cửa cao hơn đường cơ sở của SSL Hỗn Hợp Channel

- Chỉ báo QQE Cải Tiến chuyển sang màu xanh lam

- Chỉ báo Vadaata Breakout có màu xanh lục

Điều kiện vào lệnh bán (Short):

- Giá đóng cửa thấp hơn đường cơ sở của SSL Hỗn Hợp Channel

- Chỉ báo QQE Cải Tiến chuyển sang màu đỏ

- Chỉ báo Vadaata Breakout có màu đỏ

Logic thoát lệnh

Điều kiện thoát lệnh mua (Long):

- Chỉ báo QQE Cải Tiến chuyển sang màu đỏ

Điều kiện thoát lệnh bán (Short):

- Chỉ báo QQE Cải Tiến chuyển sang màu xanh lam

Phân tích lợi thế

Chiến lược này có các lợi thế sau:

-

Sự kết hợp của ba chỉ báo đảm bảo độ chính xác và ổn định của tín hiệu giao dịch.

-

Đường cơ sở của SSL Channel và chỉ báo QQE Cải Tiến có thể nắm bắt hiệu quả hướng của xu hướng.

-

Chỉ báo Vadaata Breakout xác nhận thêm tín hiệu giao dịch, tránh các phá vỡ giả.

-

Cấu trúc mã rõ ràng, dễ hiểu và dễ sửa đổi.

-

Có cơ chế quản lý rủi ro đầy đủ với cắt lỗ, chốt lời và quản lý rủi ro, giúp kiểm soát rủi ro hiệu quả.

-

Hiệu suất backtest tốt trên khung thời gian dài hơn (ví dụ: 1 giờ, 4 giờ).

Phân tích rủi ro

Chiến lược này cũng tồn tại các rủi ro sau:

-

Trên khung thời gian ngắn (ví dụ: 5 phút), kết quả backtest kém.

-

Trong thị trường dao động mạnh, cắt lỗ có thể bị kích hoạt thường xuyên.

-

Trên một số loại tiền điện tử cụ thể, kết quả backtest có thể không tốt.

Để đối phó với các rủi ro này, có thể thực hiện các biện pháp sau:

-

Chỉ sử dụng cho giao dịch trung và dài hạn, không phù hợp cho ngắn hạn.

-

Nới lỏng biên độ cắt lỗ một cách hợp lý để tránh cắt lỗ quá thường xuyên.

-

Kiểm tra thêm nhiều loại tài sản để tìm ra các loại tiền điện tử phù hợp với đặc điểm của chiến lược này.

Hướng tối ưu hóa

Chiến lược này có thể được tối ưu hóa từ các khía cạnh sau:

-

Kiểm tra các thiết lập tham số khác nhau để tìm ra sự kết hợp tốt nhất.

-

Thêm yếu tố học máy để chiến lược có khả năng thích ứng cao hơn.

-

Kết hợp nhiều yếu tố như chỉ báo tâm lý để nâng cao độ ổn định tổng thể của hệ thống.

-

Nghiên cứu đặc điểm ngành, điều chỉnh tham số để chiến lược phù hợp với ngành cụ thể.

-

Thêm module giao dịch thuật toán, sử dụng đặt lệnh tự động để nâng cao lợi nhuận.

Tổng kết

Nhìn chung, chiến lược này đáng được khuyến nghị. Nó ổn định, dễ hiểu và có hệ thống quản lý rủi ro đầy đủ. Trên các loại tài sản và khung thời gian phù hợp, nó có thể mang lại lợi nhuận tốt. Thông qua việc tối ưu hóa và điều chỉnh liên tục, chiến lược này có thể trở thành một công cụ đầu tư định lượng hiệu quả.

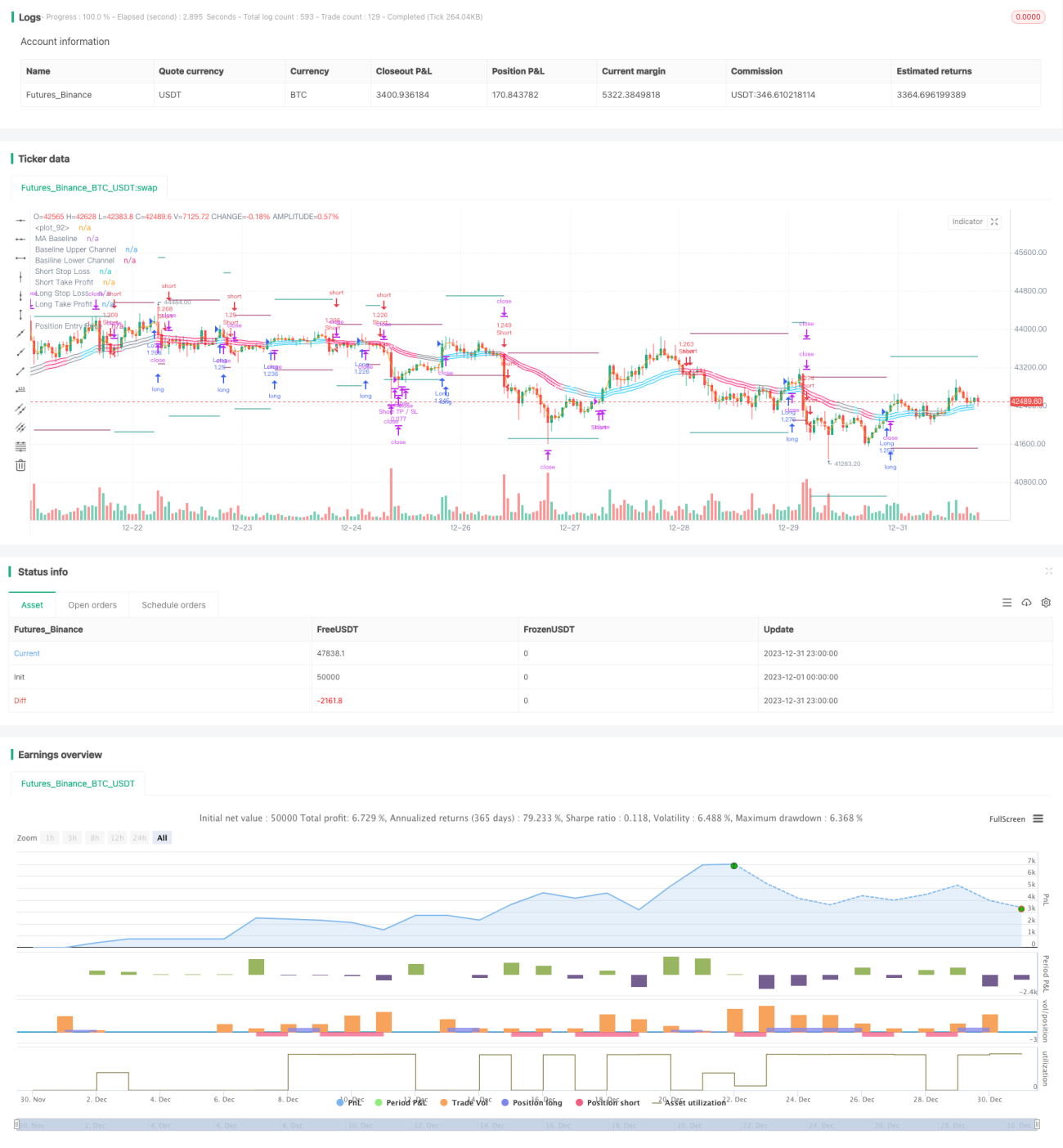

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © fpemehd

// Thanks to myncrypto, jason5480, kevinmck100

// @version=5- 1