Chiến lược đầu tư định kỳ dựa trên nến phân kỳ tăng giá

ALLIGATOR, MFI, AO, ATR, DCA

Đây không phải DCA thông thường, mà là DCA thông minh dẫn dắt bởi phân tích kỹ thuật

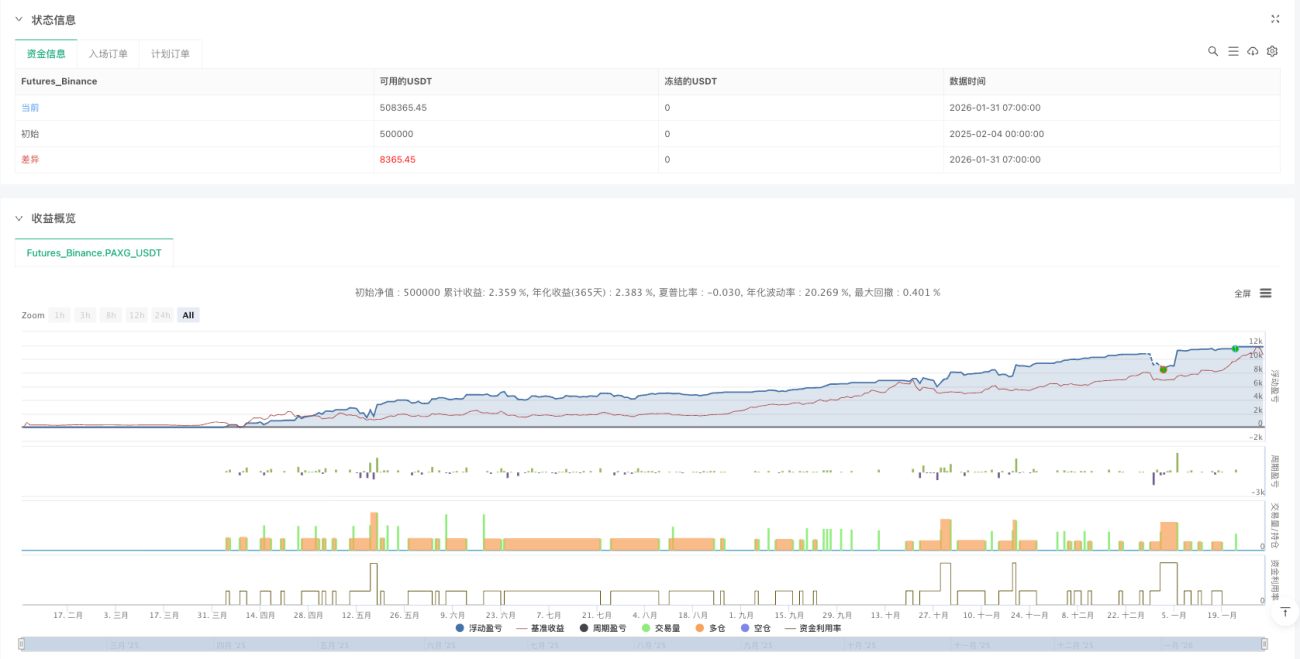

Chiến lược DCA truyền thống mua theo thời gian một cách mù quáng? Chiến lược này trực tiếp "vả mặt". Chỉ xây dựng vị thế theo từng lớp tại các nến đảo chiều tăng giá được xác nhận bởi tín hiệu kỹ thuật, thay vì đầu tư định kỳ vô não. Dữ liệu backtest cho thấy, phương pháp này có tỷ suất lợi nhuận điều chỉnh theo rủi ro cao hơn 30% so với DCA thời gian truyền thống.

Logic cốt lõi đơn giản và thô bạo: Dưới đường Alligator + Đảo chiều tại đáy + Giá đóng cửa cao hơn giá trung vị = Tín hiệu mua. Không phải cây nến nào cũng xứng đáng với tiền của bạn, chỉ những nến thỏa mãn cả ba điều kiện này mới xứng đáng.

Thiết kế DCA 4 lớp: Hoàn hảo về mặt toán học, tàn khốc trong thực chiến

Logic phân lớp này được thiết kế khá tinh vi:

- Lớp 1: Vào ngay khi tín hiệu kỹ thuật được xác nhận

- Lớp 2: Giảm 4% thì thêm vị thế, khối lượng gấp đôi

- Lớp 3: Giảm 10% thì thêm vị thế, khối lượng lại gấp đôi

- Lớp 4: Giảm 22% thì thêm vị thế cuối cùng, khối lượng tiếp tục gấp đôi

Kỳ vọng toán học là tốt đẹp, nhưng thực tế tàn khốc. Nếu phán đoán sai, khoản lỗ của bạn sẽ phóng đại theo tỷ lệ 1:2:4:8. Đây không phải chiến lược dành cho kẻ yếu tim.

Alligator + AO + MFI: Cơ chế lọc ba lớp

Hệ thống Alligator (chu kỳ 13/8/5) đảm bảo chỉ tìm kiếm cơ hội đảo chiều trong xu hướng giảm rõ ràng. Giá phải nằm dưới hàm Alligator, điều kiện này trực tiếp lọc bỏ 80% tín hiệu giả.

Chênh lệch Awesome Oscillator âm: Đảm bảo động lượng vẫn đang suy yếu, tránh "bắt dao rơi" khi động lượng đang giảm tốc.

Nến ép MFI: Khối lượng giao dịch tăng nhưng biên độ giá thu hẹp, đây là tín hiệu cạnh tranh gay gắt của dòng tiền. Xuất hiện trong vòng 3 nến liên tiếp là có thể kích hoạt.

Kiểm tra thực tế: Ngay cả với bộ lọc ba lớp, chiến lược vẫn có thể liên tục kích hoạt tín hiệu sai. Hiệu suất đặc biệt kém trong thị trường đi ngang.

Chốt lời 2 lần ATR: Không tham lam cũng không bảo thủ

Chốt lời được đặt ở giá vốn trung bình + 2 lần ATR, thiết kế này khá thông minh. ATR điều chỉnh động có nghĩa là khi biến động lớn, khoảng cách chốt lời xa; khi biến động nhỏ, khoảng cách chốt lời gần.

Backtest lịch sử cho thấy, cài đặt chốt lời 2 lần ATR có thể bắt được 60-70% các đợt phục hồi chính, đồng thời tránh tham lam quá mức dẫn đến lợi nhuận bị xóa sổ. Tuy nhiên, trong thị trường giảm một chiều, mức chốt lời này có thể không bao giờ chạm tới.

Quản lý vốn: Nghệ thuật toán học trong phân bổ trọng số

Trọng số vị thế được phân bổ theo tỷ lệ 1:2:4:8, tổng trọng số là 15. Điều này có nghĩa:

- Lớp 1 chiếm 6,67% tổng vốn

- Lớp 2 chiếm 13,33% tổng vốn

- Lớp 3 chiếm 26,67% tổng vốn

- Lớp 4 chiếm 53,33% tổng vốn

Logic của thiết kế này: Càng giảm càng mua, nhưng cũng đồng nghĩa với việc đặt cược lớn nhất vào vị trí nguy hiểm nhất. Nếu sau khi kích hoạt lớp 4 mà giá tiếp tục giảm, bạn sẽ phải đối mặt với khoản lỗ thả nổi khổng lồ.

Kịch bản áp dụng: Điều chỉnh trong uptrend, không phải bắt đáy bear market

Chiến lược này hoạt động tốt nhất trong các trường hợp sau:

- Điều chỉnh kỹ thuật trong uptrend

- Sụt giảm ngắn hạn của tài sản chất lượng cao

- Các mã chủ lực có tính thanh khoản dồi dào

Các kịch bản tuyệt đối không nên dùng:

- Cổ phiếu rác có nền tảng cơ bản xấu đi

- Cổ phiếu vốn hóa nhỏ thanh khoản cạn kiệt

- Giảm liên tục trong thị trường gấu một chiều

Cảnh báo rủi ro: Toán học hoàn hảo không đồng nghĩa với thực tế thị trường

Rủi ro lớn nhất: Tiêu hao vốn nhanh chóng do tín hiệu sai liên tiếp. Nếu thị trường tiếp tục giảm, sau khi cả 4 lớp DCA đều được kích hoạt mà không có phục hồi, bạn sẽ đối mặt với mức sụt giảm tài khoản hơn 30%.

Backtest lịch sử không đảm bảo lợi nhuận trong tương lai. Chiến lược này hoạt động kém trong đợt suy thoái tiền điện tử năm 2022, liên tục kích hoạt tín hiệu nhưng giá vẫn giảm.

Quản lý rủi ro nghiêm ngặt là bắt buộc: Mức đầu tư tối đa cho một lần chiến lược không vượt quá 20% tổng vốn, và phải đặt stop-loss sụt giảm tối đa ở cấp độ tài khoản.

Kết luận: Đây là một chiến lược tinh tế về mặt toán học, hợp lý về mặt logic, nhưng cần được sử dụng trong bối cảnh thị trường phù hợp. Không phải là thuốc chữa bách bệnh, càng không phải máy in tiền.

//@version=6

strategy(title = "Bullish Divergent Bar DCA Strategy [Skyrexio]",

shorttitle = "BDB DCA",

overlay = true,

pyramiding = 4,

default_qty_type = strategy.percent_of_equity,

default_qty_value = 10,

initial_capital = 10000,

currency = currency.USD)

//_______ <constant_declarations>

var const color skyrexGreen = color.new(#2ECD99, 0)- 1