Chiến lược AI siêu xu hướng tự thích ứng

SUPERTREND, ATR, ADX, EMA, AI

Đây không phải là chiến lược SuperTrend thông thường bạn từng thấy

Vấn đề lớn nhất của chiến lược SuperTrend truyền thống? Các tham số cố định hoạt động rất khác nhau trong các môi trường thị trường khác nhau. Phiên bản nâng cấp AI này điều chỉnh động bội số ATR, tăng lên gấp 2 lần giá trị cơ bản trong thời kỳ biến động cao và giảm xuống 0,85 lần trong thời kỳ biến động thấp. Dữ liệu backtest cho thấy cơ chế thích ứng này có thể giảm đáng kể tín hiệu giả trong thị trường dao động.

Đổi mới cốt lõi nằm ở hệ thống lọc ba lớp: nhận diện trạng thái thị trường, đánh giá tín hiệu AI, cơ chế xác nhận nhiều lớp. Không còn đơn giản là giá phá vỡ đường SuperTrend để vào lệnh, mà yêu cầu điểm đánh giá AI đạt trên 65 mới kích hoạt tín hiệu giao dịch. Hệ thống đánh giá này xem xét tổng thể 5 khía cạnh: sự gia tăng đột biến khối lượng, mức độ lệch giá, tính nhất quán của xu hướng, v.v.

Hệ thống đánh giá AI: Định lượng độ tin cậy của mỗi tín hiệu

Cơ chế đánh giá được thiết kế tinh tế: Sự gia tăng đột biến khối lượng chiếm 20 điểm, khoảng cách lệch giá so với đường SuperTrend chiếm 25 điểm, tính nhất quán xu hướng EMA chiếm 20 điểm, chất lượng trạng thái thị trường chiếm 15 điểm, khoảng cách giá trước đó với đường xu hướng chiếm 20 điểm. Tổng điểm 100, ngưỡng mặc định 65 điểm có nghĩa là chỉ những tín hiệu chất lượng cao mới vượt qua bộ lọc.

Cụ thể, khi khối lượng vượt quá trung bình 20 chu kỳ 2,5 lần thì đạt điểm tối đa 20, và khi giá lệch khỏi đường SuperTrend trên 1,5 lần ATR thì đạt điểm tối đa 25. Đánh giá định lượng này tránh phán đoán chủ quan, mỗi tín hiệu đều có dữ liệu hỗ trợ rõ ràng. Trong thực tế, khuyến nghị điều chỉnh yêu cầu điểm tối thiểu dựa trên đặc tính của từng sản phẩm.

Tự thích ứng trạng thái thị trường: Nói lời tạm biệt với tham số một kích cỡ cho tất cả

Chiến lược xác định ba trạng thái thị trường thông qua tỷ lệ ATR và chỉ số ADX: thời kỳ xu hướng (regime=1), thời kỳ biến động cao (regime=2), thời kỳ dao động (regime=0). Khi tỷ lệ ATR vượt quá 1,4 thì xác định là thời kỳ biến động cao, khi ADX dưới 20 và tỷ lệ ATR dưới 0,9 là thời kỳ dao động.

Logic điều chỉnh bội số thích ứng: Trong thời kỳ biến động cao, bội số tăng 40% × (tỷ lệ ATR - 1,0), trong thời kỳ dao động, bội số giảm xuống 85% giá trị cơ bản. Điều này có nghĩa là bội số cơ bản 3.0 có thể được điều chỉnh lên 4.2 trong biến động cực đoan và giảm xuống 2.55 trong thời kỳ dao động. Cơ chế điều chỉnh động này nâng cao đáng kể khả năng thích ứng của chiến lược trong các môi trường thị trường khác nhau.

Quản lý rủi ro: Ba chế độ stop loss tùy bạn lựa chọn

ATR dynamic stop loss là lựa chọn ưu tiên, khoảng cách 2,5 lần ATR mặc định có thể dung nạp biến động bình thường và cắt lỗ kịp thời. Phần trăm stop loss phù hợp với các sản phẩm có biến động tương đối ổn định, chế độ SuperTrend đóng vị thế ngay lập tức khi xu hướng đảo chiều.

Cài đặt take profit hỗ trợ chế độ tỷ lệ rủi ro/lợi nhuận, tỷ lệ rủi ro/lợi nhuận mặc định 2.5:1 có lợi thế thống kê. Khi bật trailing stop, mức stop loss của vị thế có lãi sẽ được điều chỉnh động dựa trên khoảng cách 2,5 lần ATR, tối đa hóa lợi nhuận trong các xu hướng mạnh.

Bộ lọc đa lớp: Giảm giao dịch không hiệu quả

Bộ lọc xu hướng EMA đảm bảo chỉ vào lệnh khi hướng của EMA 50 chu kỳ đồng thuận, tránh giao dịch ngược xu hướng. Bộ lọc thời kỳ dao động trực tiếp bỏ qua các tín hiệu regime=0, dù có thể bỏ lỡ một số cơ hội nhưng giảm đáng kể tỷ lệ tín hiệu giả.

Bộ lọc khối lượng yêu cầu khối lượng khi vào lệnh phải cao hơn trung bình 20 chu kỳ, đảm bảo có đủ sự tham gia của thị trường để hỗ trợ phá vỡ giá. Thời gian chờ 10 chu kỳ ngăn giao dịch quá thường xuyên, giảm chi phí giao dịch.

Lời khuyên thực hành: Tối ưu tham số và kiểm soát rủi ro

Đối với tiền điện tử, khuyến nghị nâng điểm AI tối thiểu lên 70, đối với cổ phiếu truyền thống có thể hạ xuống 60. Nhà giao dịch tần suất cao có thể rút ngắn thời gian chờ xuống 5 chu kỳ, nhà đầu tư dài hạn khuyến nghị kéo dài lên 15 chu kỳ.

Tham số độ dài ATR 10 là điểm cân bằng đã được tối ưu, quá ngắn sẽ quá nhạy cảm, quá dài sẽ chậm trễ. Bội số cơ bản 3.0 phù hợp với hầu hết các sản phẩm, sản phẩm biến động cao có thể điều chỉnh lên 3.5, sản phẩm biến động thấp giảm xuống 2.5.

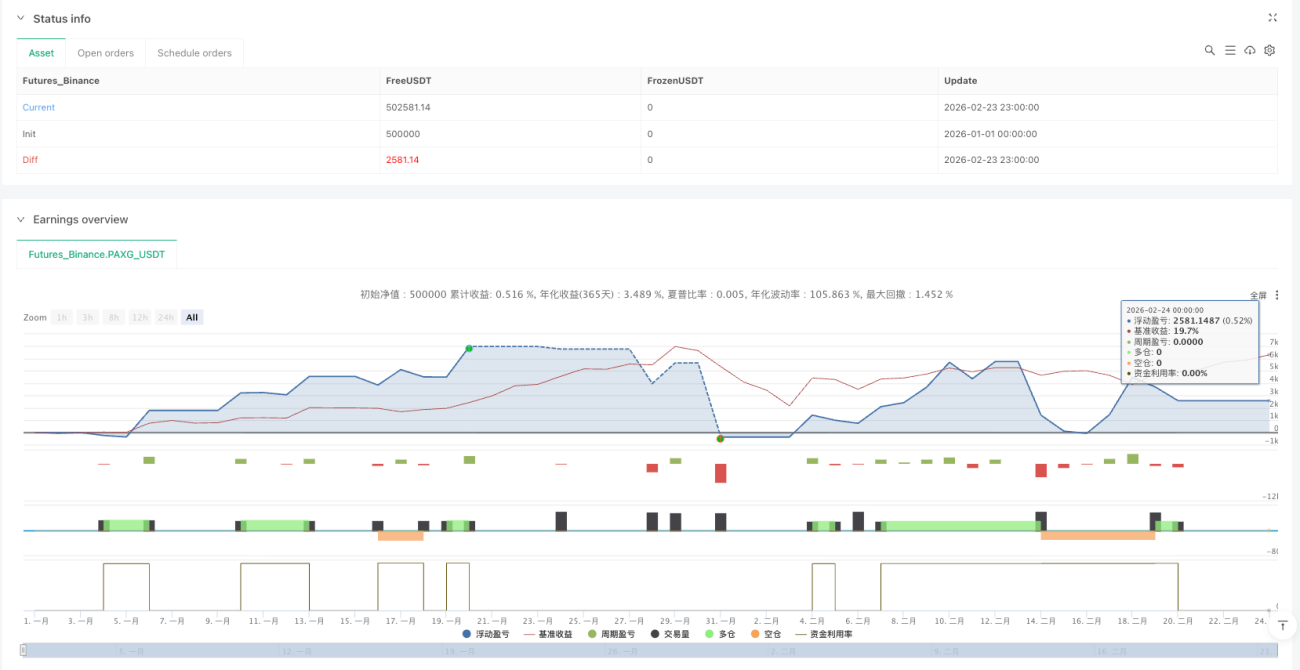

Cảnh báo rủi ro quan trọng: Kết quả backtest lịch sử không đại diện cho hiệu suất trong tương lai. Chiến lược có thể gặp thua lỗ liên tiếp trong điều kiện thị trường cực đoan, khuyến nghị kiểm soát chặt chẽ khối lượng mỗi lệnh không quá 30% tổng vốn. Hiệu suất chiến lược khác biệt đáng kể trong các môi trường thị trường khác nhau, cần theo dõi và điều chỉnh tham số liên tục.

/*backtest

start: 2026-01-01 00:00:00

end: 2026-02-24 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"PAXG_USDT","balance":500000}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © DefinedEdge

//@version=6- 1