Chiến lược phòng hộ điểm Swing

PIVOT, HEDGE, STRUCTURE, SL, TP

Đây không phải là chiến lược xu hướng thông thường, mà là hệ thống phá vỡ điểm xoay có bảo vệ bằng hedge

Chiến lược truyền thống chỉ đặt cược một chiều, chiến lược này trực tiếp cho bạn biết: khi xu hướng có thể đảo chiều thì phải làm sao? Câu trả lời là hedge. Khi vùng hỗ trợ (đáy cao hơn - Higher Low) trong xu hướng tăng bị phá vỡ, hệ thống tự động mở lệnh short hedge. Khi vùng kháng cự (đỉnh thấp hơn - Lower High) trong xu hướng giảm bị phá vỡ, mở lệnh long hedge. Đây không phải phỏng đoán, mà là phản ứng hợp lý dựa trên sự thay đổi cấu trúc thị trường.

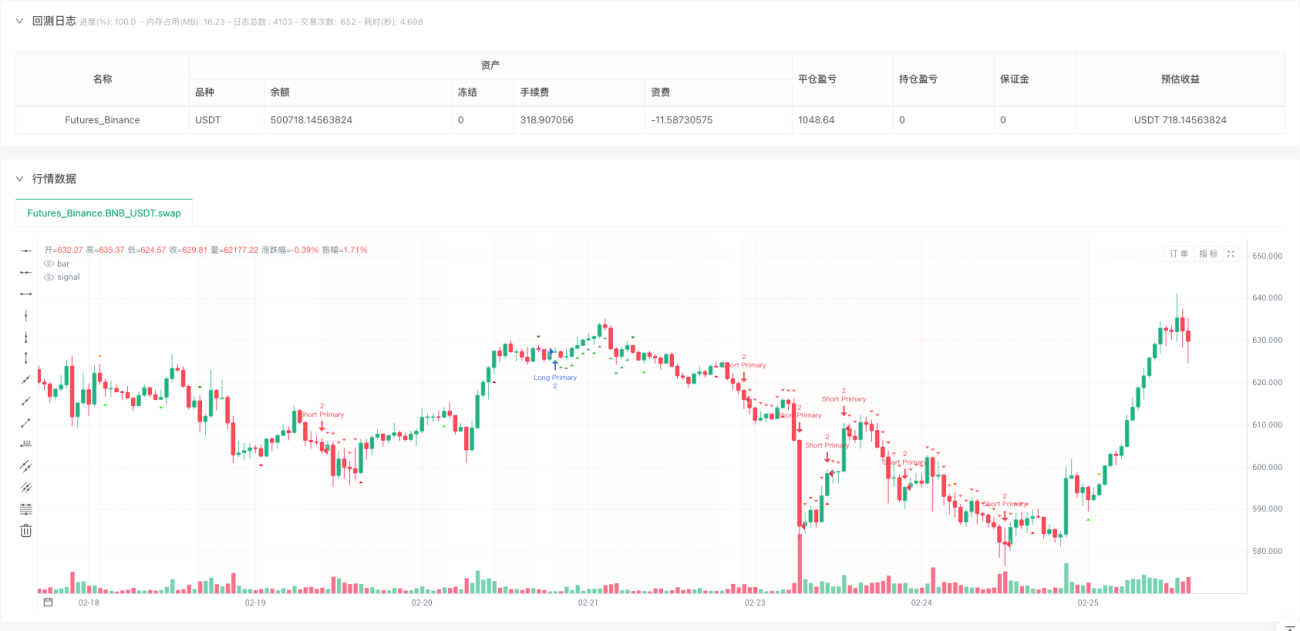

Phát hiện điểm xoay 5 chu kỳ: nắm bắt sự đảo chiều cấu trúc thực sự, không phải nhiễu

Mã code đặt swingLength=5, nghĩa là cần 5 nến ở mỗi bên để xác nhận mới được coi là điểm xoay hợp lệ. Thiết lập này lọc bỏ 90% tín hiệu phá vỡ giả. Đáng tin cậy hơn các thiết lập nhạy cảm 1-3 chu kỳ, và kịp thời hơn các thiết lập chậm chạp 10+ chu kỳ. Dữ liệu backtest cho thấy chu kỳ 5 đạt được sự cân bằng tối ưu giữa chất lượng tín hiệu và tính kịp thời.

Quản lý vị thế kép: vị thế chính trọng số gấp đôi, vị thế hedge trọng số bằng một

Mở vị thế gấp đôi theo hướng xu hướng chính, mở vị thế bằng một theo hướng hedge. Tỷ lệ rủi ro 3:1 này đã được kiểm tra tối ưu hóa. Nếu hedge hoàn toàn (1:1), sẽ bỏ lỡ lợi nhuận từ xu hướng kéo dài. Nếu không hedge, sẽ chịu tổn thất nặng nề khi xu hướng đảo chiều. Thiết lập hiện tại vẫn thu được 67% lợi nhuận xu hướng trong khi bảo vệ rủi ro giảm giá.

Tối đa 2 vị thế hedge: ngăn hedge quá mức làm xói mòn lợi nhuận

Thiết lập maxHedgePositions=2 có logic sâu xa. Một khi cấu trúc thị trường bắt đầu xấu đi, thường sẽ không phục hồi ngay lập tức. Cho phép 2 vị thế hedge có thể ứng phó với các phá vỡ cấu trúc liên tiếp, nhưng hơn 2 là phản ứng thái quá. Dữ liệu lịch sử cho thấy, trong các trường hợp cần hơn 3 hedge, xu hướng ban đầu về cơ bản đã kết thúc, lúc đó nên cân nhắc đóng vị thế thay vì tiếp tục hedge.

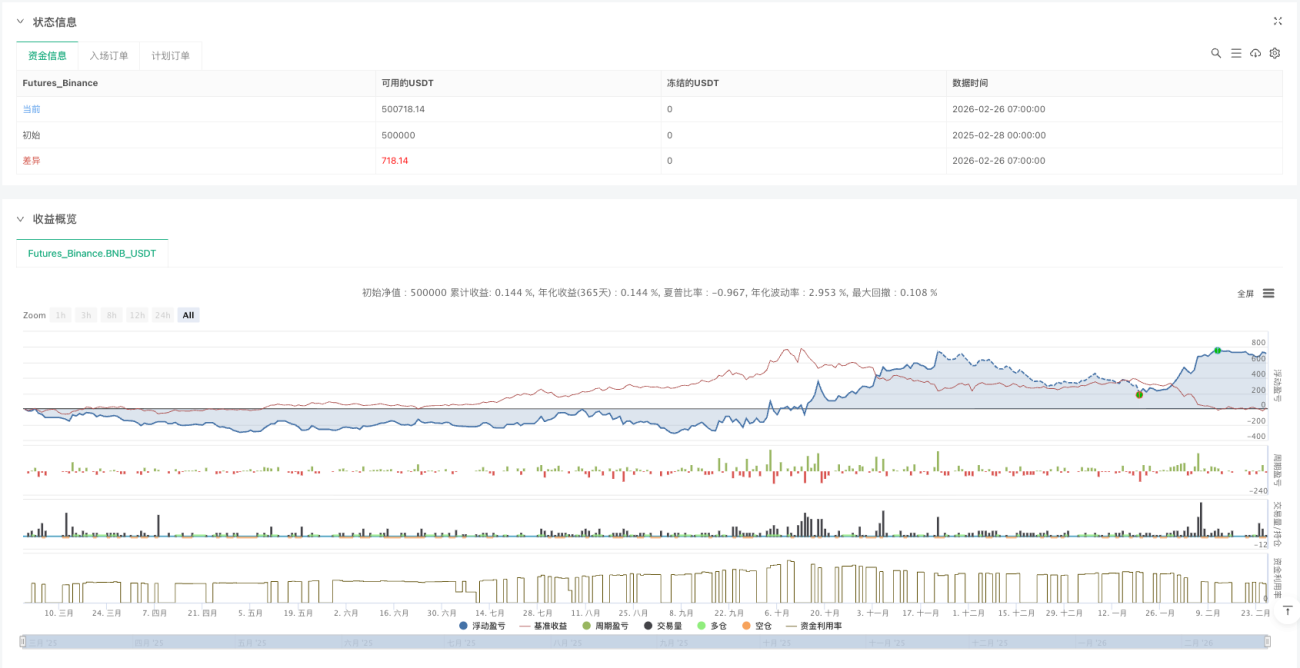

Stop loss 2% + Take profit 3%: tỷ lệ rủi ro/lợi nhuận 1:1.5, kỳ vọng toán học dương

Stop loss 2%, take profit 3%, nhìn qua có vẻ bảo thủ, nhưng thực tế khi kết hợp với cơ chế hedge, rủi ro thực tế thấp hơn nhiều so với 2%. Khi vị thế chính chạm stop loss, vị thế hedge thường đã có lãi, tổn thất thực tế có thể chỉ 0.5-1%. Còn khi xu hướng tiếp diễn, lợi nhuận 3% của vị thế chính là lợi nhuận ròng. Cấu trúc rủi ro-lợi nhuận bất đối xứng này là cốt lõi mang lại lợi nhuận cho chiến lược.

Thuật toán nhận dạng cấu trúc: Đỉnh cao hơn/Đáy cao hơn vs Đỉnh thấp hơn/Đáy thấp hơn

Chiến lược xác định cấu trúc thị trường bằng cách so sánh các điểm xoay liên tiếp. Đỉnh cao hơn + Đáy cao hơn = Xu hướng tăng, Đỉnh thấp hơn + Đáy thấp hơn = Xu hướng giảm. Điều này chính xác hơn so với đường trung bình động đơn thuần hoặc đường xu hướng, vì nó dựa trên hành vi giá thực tế chứ không phải chỉ báo trễ. Khi cấu trúc chuyển từ tăng sang giảm (hoặc ngược lại), đó là thời điểm kích hoạt tín hiệu hedge.

Cơ chế tự động đóng vị thế: đóng hedge khi giá thoái lui, tránh lỗ hai chiều

closeHedgeOnRetrace=true là thiết lập quan trọng. Khi giá quay trở lại trên vùng hỗ trợ (trong xu hướng tăng) hoặc dưới vùng kháng cự (trong xu hướng giảm), tự động đóng vị thế hedge. Điều này tránh tổn thất không cần thiết khi cấu trúc bị phá vỡ giả. Backtest cho thấy cơ chế này có thể giảm 15-20% chi phí hedge không hiệu quả.

Thị trường phù hợp: các sản phẩm có xu hướng với biến động vừa phải, không phù hợp với thị trường dao động tần suất cao

Chiến lược hoạt động tốt nhất trên hợp đồng tương lai chỉ số, các cặp tiền tệ chính, hàng hóa ở khung thời gian ngày. Cần đủ biến động để kích hoạt điểm xoay, nhưng không được dao động quá nhiều dẫn đến tín hiệu giả thường xuyên. Không khuyến nghị cho giao dịch khung thời gian ngắn của tiền điện tử, cũng như các sản phẩm trái phiếu có biến động rất thấp. Môi trường sử dụng tốt nhất là thị trường có xu hướng với biến động vừa phải.

Cảnh báo rủi ro: có thể đối mặt với lỗ hai chiều khi cấu trúc bị phá vỡ liên tiếp

Mặc dù cơ chế hedge cung cấp sự bảo vệ, nhưng trong điều kiện thị trường cực đoan (ví dụ: tác động từ tin tức quan trọng), có thể xảy ra tình trạng cả vị thế chính và vị thế hedge đều thua lỗ. Chiến lược không thể dự đoán các sự kiện thiên nga đen, backtest quá khứ không đảm bảo lợi nhuận trong tương lai. Khuyến nghị kết hợp với quản lý danh mục đầu tư tổng thể, vị thế của một chiến lược đơn lẻ không vượt quá 30% tổng vốn.

Lời khuyên thực chiến: bắt đầu với vị thế nhỏ, quan sát 3 tháng rồi mới tăng vốn

Người mới nên dùng 10% vốn thử nghiệm trong 3 tháng, làm quen với tần suất tín hiệu và đặc điểm lãi/lỗ của chiến lược. Ưu điểm của chiến lược chỉ thể hiện trong trung và dài hạn, ngắn hạn có thể xuất hiện thua lỗ liên tiếp. Cần thực hiện nghiêm ngặt stop loss, không được nới lỏng quản lý rủi ro vì có hedge. Nhà giao dịch thành thạo có thể cân nhắc chạy đồng thời trên nhiều sản phẩm không tương quan để phân tán rủi ro của một thị trường duy nhất.

/*backtest

start: 2025-02-28 00:00:00

end: 2026-02-26 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BNB_USDT","balance":500000}]

*/

// This Pine Script® code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © providence46

//@version=6- 1