0

关注

18

关注者

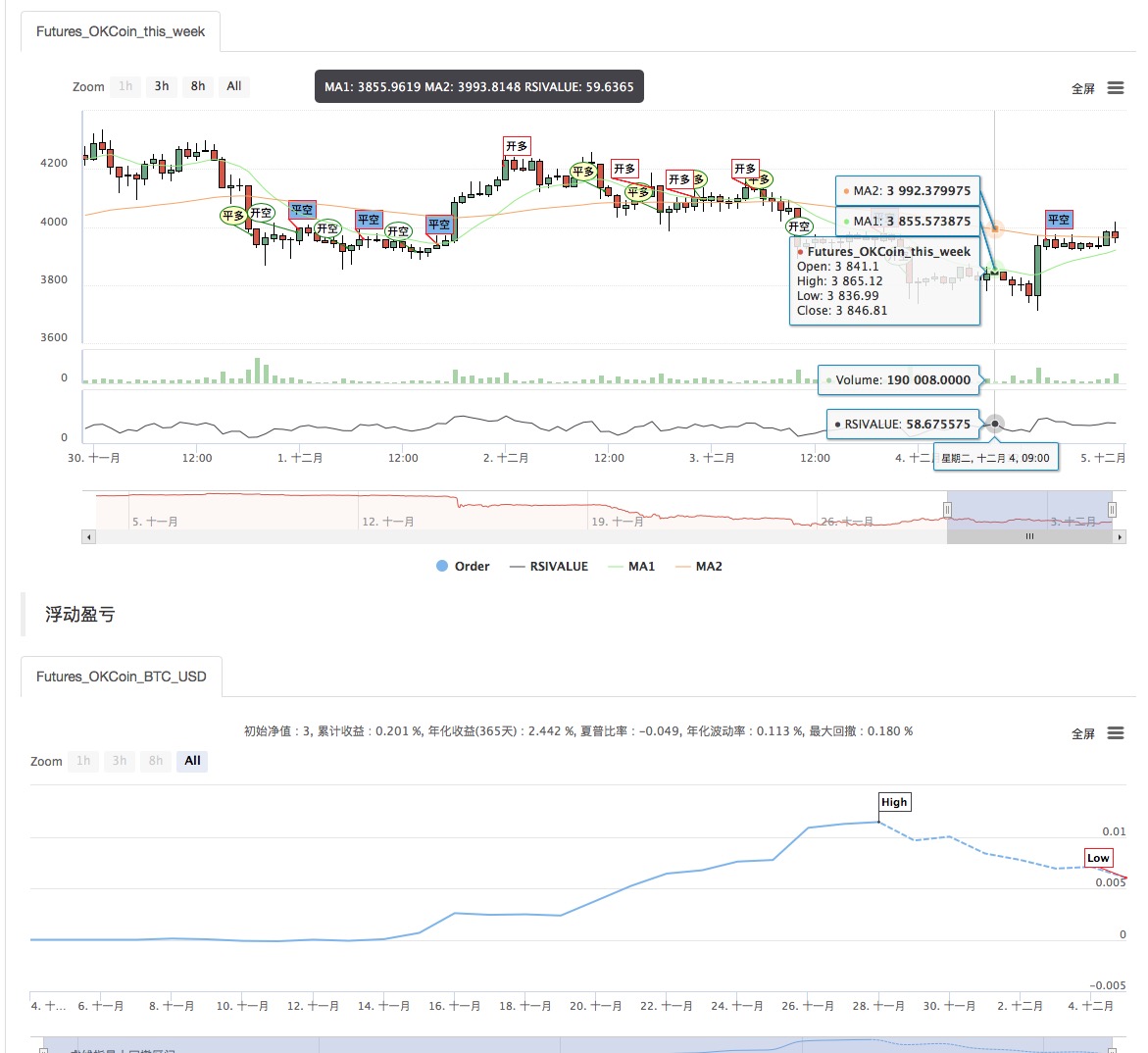

- 策略名称:双均线策略与相对强弱RSI指标组合

- 数据周期:15M,30M等

- 支持:商品期货、数字货币

- 官方网站:www.quantinfo.com

-

主图:

均线1,公式:MA1^^EMA(C,N1);

均线2,公式:MA2^^EMA(C,N2); -

副图:

RSI,公式:RSIVALUE:SMA(MAX(CLOSE-REF(CLOSE,1),0),LENGTH,1)/SMA(ABS(CLOSE-REF(CLOSE,1)),LENGTH,1)*100;

策略源码

My语言

策略参数

评论

全部评论 (2)

- 1