Python简单测试策略

6

Follow

948

Followers

需要下载最新的托管者, 托管者机器个需要安装python, (Linux自带无需安装)

Source

Python

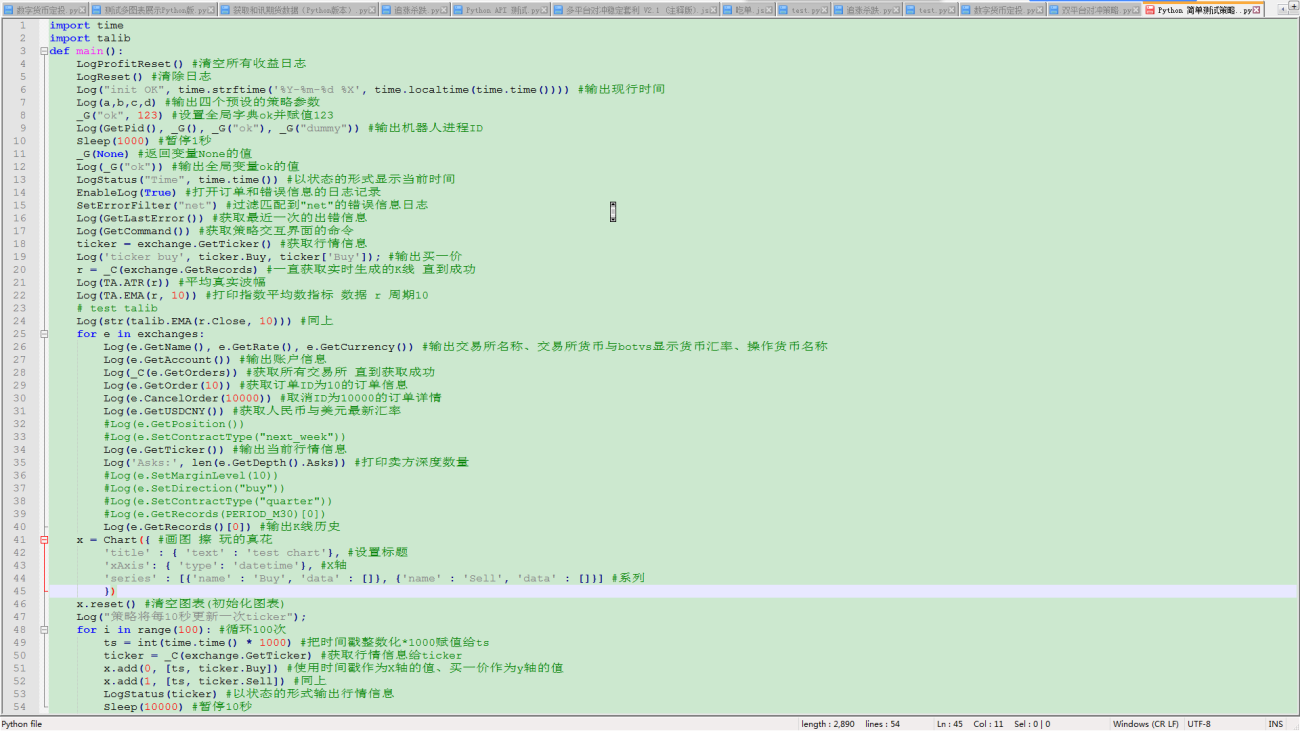

import time

import talib

def main():

LogProfitReset()

LogReset()

Log("init OK", time.strftime('%Y-%m-%d %X', time.localtime(time.time())))

Log(a,b,c,d)

_G("ok", 123)

Log(GetPid(), _G(), _G("ok"), _G("dummy"))

Sleep(1000)

_G(None)

Log(_G("ok"))

LogStatus("Time", time.time())

EnableLog(True)

SetErrorFilter("net")

Log(GetLastError())

Log(GetCommand())

ticker = exchange.GetTicker()

Log('ticker buy', ticker.Buy, ticker['Buy']);

r = _C(exchange.GetRecords)

Log(TA.ATR(r))

Log(TA.EMA(r, 10))

# test talib

Log(str(talib.EMA(r.Close, 10)))

for e in exchanges:

Log(e.GetName(), e.GetRate(), e.GetCurrency())

Log(e.GetAccount())

Log(_C(e.GetOrders))

Log(e.GetOrder(10))

Log(e.CancelOrder(10000))

Log(e.GetUSDCNY())

#Log(e.GetPosition())

#Log(e.SetContractType("next_week"))

Log(e.GetTicker())

Log('Asks:', len(e.GetDepth().Asks))

#Log(e.SetMarginLevel(10))

#Log(e.SetDirection("buy"))

#Log(e.SetContractType("quarter"))

#Log(e.GetRecords(PERIOD_M30)[0])

Log(e.GetRecords()[0])

x = Chart({

'title' : { 'text' : 'test chart'},

'xAxis': { 'type': 'datetime'},

'series' : [{'name' : 'Buy', 'data' : []}, {'name' : 'Sell', 'data' : []}]

})

x.reset()

Log("策略将每10秒更新一次ticker");

for i in range(100):

ts = int(time.time() * 1000)

ticker = _C(exchange.GetTicker)

x.add(0, [ts, ticker.Buy])

x.add(1, [ts, ticker.Sell])

LogStatus(ticker)

Sleep(10000)Strategy parameters

Related strategies