Advanced Fair Value Gap Detection Strategy with Dynamic Risk Management and Fixed Take Profit

Overview

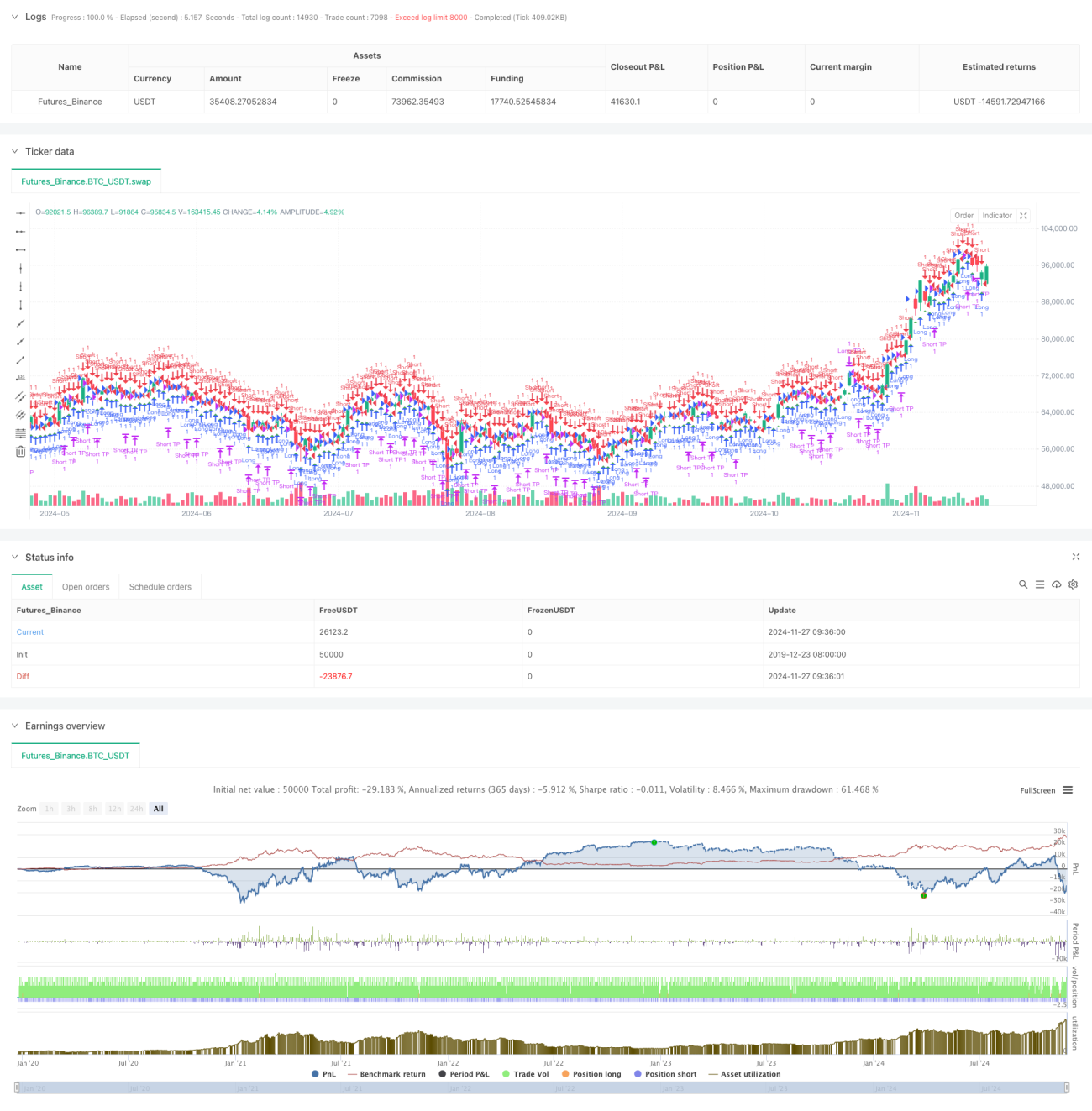

This is a trading strategy based on Fair Value Gap (FVG) detection, combining dynamic risk management with fixed take profit targets. Operating on a 15-minute timeframe, the strategy identifies potential trading opportunities by detecting price gaps in the market. According to backtest data from November 2023 to August 2024, the strategy achieved a net profit of 284.40% with 153 total trades, maintaining a win rate of 71.24% and a profit factor of 2.422.

Strategy Principle

The core mechanism revolves around detecting Fair Value Gaps by monitoring price relationships across three consecutive candles:

- Bullish FVG: When the high of the middle candle is below the low of the first candle

- Bearish FVG: When the low of the middle candle is above the high of the first candle

- Entry signals are controlled by an FVG threshold parameter

- Risk control uses a fixed percentage (1%) of account equity as stop loss

- Take profit is set at a fixed 50 points

Strategy Advantages

- Scientific risk management: Uses account equity percentage for stop loss

- Clear trading rules: Fixed take profit targets eliminate subjective judgment

- Excellent performance: High win rate and profit factor indicate strategy stability

- Simple implementation: Clear code logic, easy to understand and maintain

- High adaptability: Can be adjusted for different market conditions

Strategy Risks

- Market volatility risk: Fixed point take profit may be inflexible in highly volatile markets

- Slippage risk: Frequent trading may lead to higher slippage costs

- Parameter dependency: Performance heavily relies on FVG threshold settings

- False breakout risk: Some FVG signals might be false breakouts

- Money management risk: Fixed percentage stop loss might lead to quick drawdowns

Optimization Directions

- Introduce volatility indicators for dynamic take profit adjustment

- Add trend filters to avoid ranging market trades

- Develop multiple timeframe confirmation mechanism

- Optimize position sizing algorithm with floating position system

- Add trading time filters to avoid high volatility periods

- Develop signal strength scoring system for high-quality trade selection

Summary

This strategy demonstrates impressive results by combining Fair Value Gap theory with scientific risk management. The high win rate and stable profit factor indicate its practical value. Through the suggested optimization directions, there is potential for further improvement. Traders are advised to conduct thorough parameter optimization and backtesting before live implementation.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-11-28 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Fair Value Gap Strategy with % SL and Fixed TP", overlay=true, initial_capital=500, default_qty_type=strategy.fixed, default_qty_value=1)

// Parameters- 1