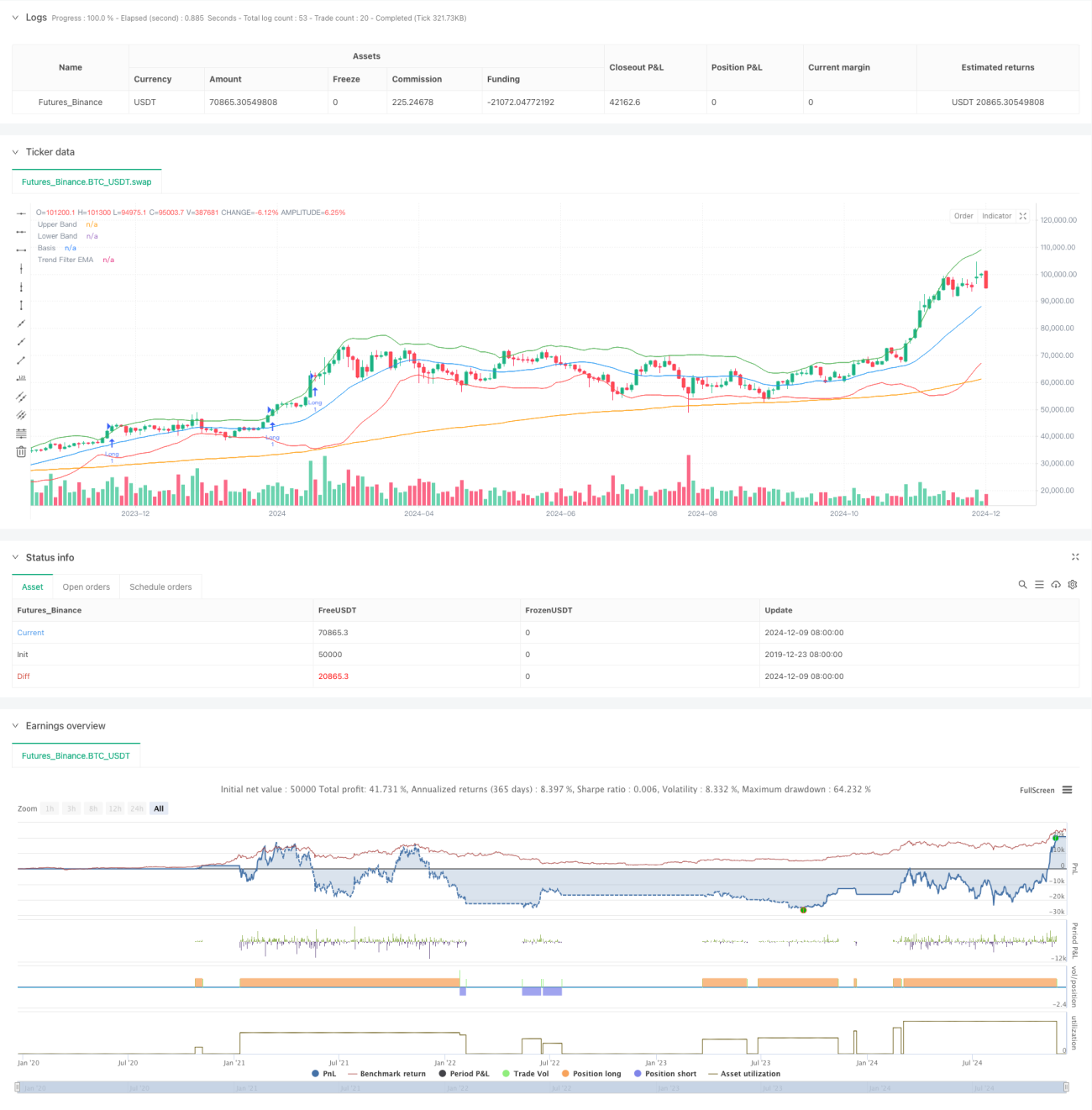

Overview

This strategy is an advanced quantitative trading system combining Bollinger Bands, RSI indicator, and 200-period EMA trend filter. Through the synergy of multiple technical indicators, it captures high-probability breakout opportunities in trend direction while effectively filtering false signals in oscillating markets. The system employs dynamic stop-loss and profit targets based on risk-reward ratio to achieve robust trading performance.

Strategy Principle

The core logic is based on three levels:

- Bollinger Bands breakout signals: Using Bollinger Bands as volatility channels, price breaks above upper band signal long entries, breaks below lower band signal short entries.

- RSI momentum confirmation: RSI above 50 confirms bullish momentum, below 50 confirms bearish momentum, avoiding trades without trend.

- EMA trend filtering: Using 200-period EMA to determine main trend, only trading in trend direction. Long above EMA, short below EMA.

Trade confirmation requires:

- Breakout conditions maintained for two consecutive candles

- Volume above 20-period average

- Dynamic stop-loss calculated based on ATR

- Profit target set at 1.5 times risk-reward ratio

Strategy Advantages

- Multiple technical indicators synergize to significantly improve signal quality

- Dynamic position management mechanism adapts to market volatility

- Strict trade confirmation mechanism effectively reduces false signals

- Complete risk control system including dynamic stop-loss and fixed risk-reward ratio

- Flexible parameter optimization space adaptable to different market environments

Strategy Risks

- Excessive parameter optimization may lead to overfitting

- Volatile markets may trigger frequent stop-losses

- Oscillating markets may produce consecutive losses

- Signals lag at trend turning points

- Technical indicators may produce contradictory signals

Risk control suggestions:

- Strictly execute stop-loss discipline

- Control single trade risk

- Regular backtest parameter validity

- Integrate fundamental analysis

- Avoid overtrading

Strategy Optimization Directions

- Introduce more technical indicators for cross-validation

- Develop adaptive parameter optimization mechanism

- Add market sentiment indicators

- Optimize trade confirmation mechanism

- Develop more flexible position management system

Main optimization approaches:

- Dynamically adjust parameters based on different market cycles

- Add trading filters

- Optimize risk-reward ratio settings

- Improve stop-loss mechanism

- Develop smarter signal confirmation system

Summary

This strategy constructs a complete trading system through organic combination of Bollinger Bands, RSI and EMA technical indicators. While ensuring trading quality, the system demonstrates strong practical value through strict risk control and flexible parameter optimization space. Traders are advised to carefully validate parameters in live trading, strictly execute trading discipline, and continuously optimize strategy performance.

- 1