2

关注

502

关注者

概述

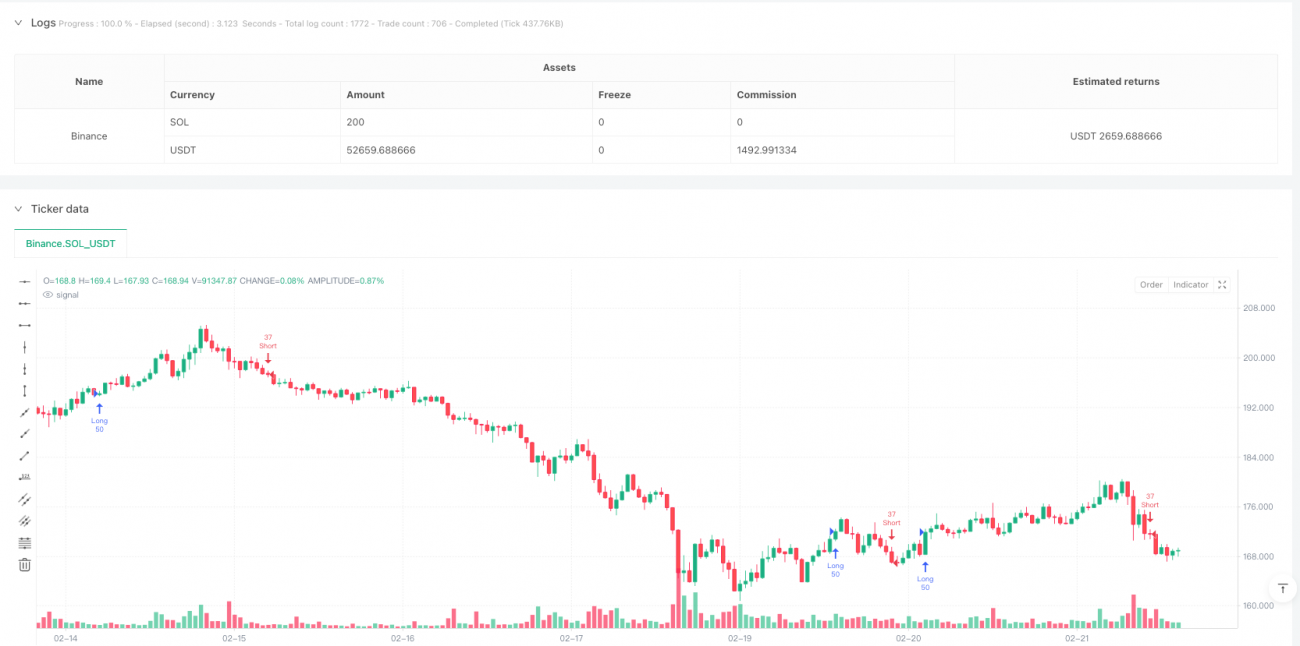

这是一个专为纳斯达克100微型期货设计的日内交易策略。策略核心采用双均线系统结合成交量加权平均价格(VWAP)作为趋势确认,并通过真实波动幅度(ATR)动态调整止损位置。该策略在保持资金安全的同时,通过严格的风险控制和动态的仓位管理来捕捉市场趋势。

策略原理

策略主要基于以下几个核心组件:

- 信号系统采用9周期与21周期指数移动平均线(EMA)的交叉来识别趋势方向。当短期均线向上穿越长期均线时产生做多信号,反之产生做空信号。

- 使用VWAP作为趋势确认指标,价格需要位于VWAP之上才能开多仓,位于VWAP之下才能开空仓。

- 风险管理系统使用基于ATR的动态止损,多仓止损设置为2倍ATR,空仓为1.5倍ATR。

- 获利目标采用不对称设计,多仓使用3:1的收益风险比,空仓使用2:1的收益风险比。

- 设置了移动止损和保本止损机制,当价格达到目标利润的50%时,止损点上移至成本位。

策略优势

- 动态适应性强 - 通过ATR来调整止损和移动止损参数,策略能够自动适应不同的市场波动环境。

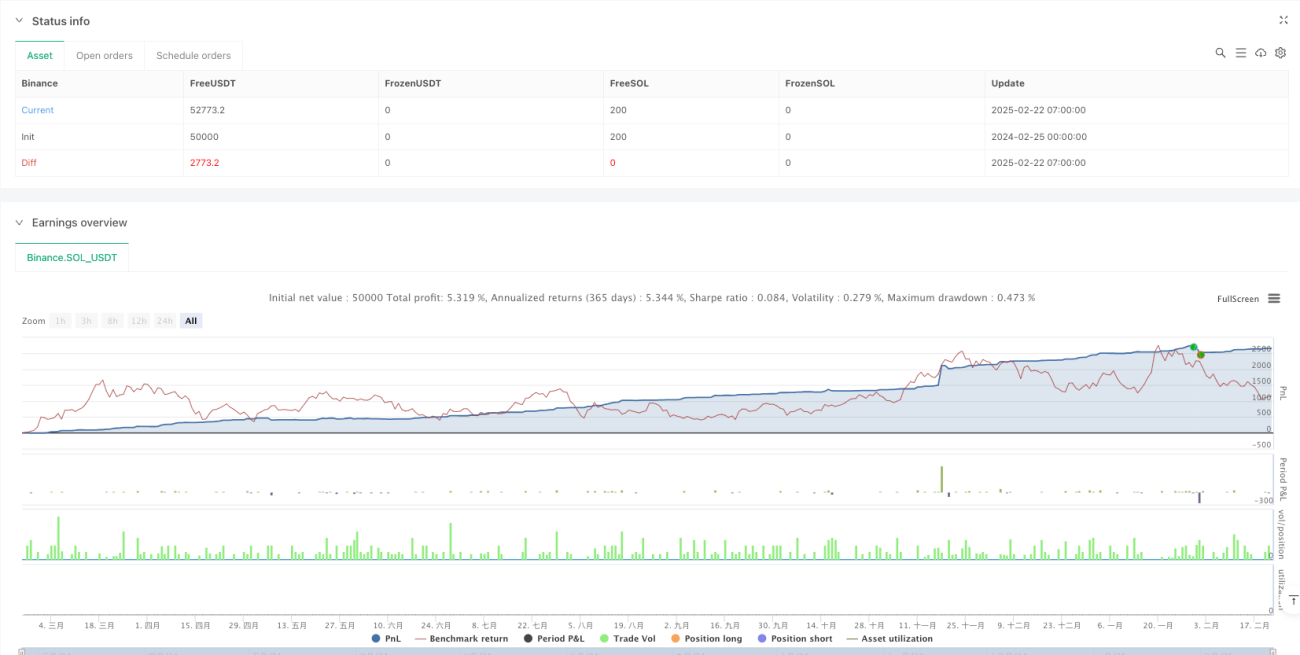

- 风险控制完善 - 每笔交易风险限制在1500美元以内,并设置了7500美元的每周最大亏损限制。

- 不对称收益设计 - 考虑到市场特性,多空策略采用不同的收益风险比和仓位大小,更符合市场实际情况。

- 多重确认机制 - 结合EMA交叉和VWAP确认,有效减少假突破信号。

- 完整的止损体系 - 包含固定止损、移动止损和保本止损三重保护。

策略风险

- 震荡市场风险 - 在横盘震荡市场中,均线交叉信号可能产生较多假信号。

- 滑点风险 - 在快速行情中,实际成交价格可能与信号价格存在较大偏差。

- 系统性风险 - 当市场出现重大事件时,止损可能失效。

- 过度交易风险 - 频繁的信号可能导致交易成本增加。

- 资金管理风险 - 如果初始资金较小,可能无法有效执行完整的仓位管理计划。

策略优化方向

- 引入成交量过滤器 - 可以添加成交量确认机制,只在成交量满足条件时执行交易。

- 优化时间过滤 - 考虑加入具体的交易时间窗口,避开波动较大的开盘和收盘时段。

- 动态调整参数 - 可以根据不同的市场环境自动调整均线周期和ATR倍数。

- 增加市场情绪指标 - 引入VIX等波动率指标来调整交易频率和仓位大小。

- 完善移动止损 - 可以设计更灵活的移动止损算法,提高对趋势的把握能力。

总结

该策略通过均线系统和VWAP的配合建立了稳健的趋势跟踪系统,并通过多层次的风险控制机制保护资金安全。策略的最大特点是其适应性和风险管理能力,通过ATR动态调整各项参数,使其能够在不同市场环境下保持稳定性能。该策略特别适合日内交易纳斯达克100微型期货,但需要交易者严格执行风险控制规则,并根据市场变化适时调整参数。

策略源码

Pine

/*backtest

start: 2024-02-25 00:00:00

end: 2025-02-22 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"SOL_USDT"}]

*/

//@version=5

strategy("Nasdaq 100 Micro - Optimized Risk Management", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// === INPUTS ===策略参数

评论

全部评论 (0)

暂无数据

- 1