8周期RSI+动量阈值14:这不是传统RSI策略

别再用14周期RSI了。这个策略直接把RSI周期压缩到8,配合14点动量阈值,专门捕捉短线爆发。传统RSI策略在震荡市场中反复打脸,而这套组合在高频波动中表现更稳定。

核心逻辑很直接:RSI动量变化>14时触发多头信号,<-14时触发空头信号。同时要求成交量超过13周期均量,确保不是假突破。这种设计比单纯的RSI超买超卖信号提前1-2个周期,抓住趋势启动的黄金时刻。

4.15%止盈vs1.85%止损:风险收益比超过2:1

止盈4.15%,止损1.85%,风险收益比达到2.24:1。这个比例在剥头皮策略中算是激进的,但配合2.55%移动止损,实际风险控制更严格。

关键在于移动止损的设计:一旦价格朝有利方向移动,止损线会跟随最高点/最低点动态调整。这意味着即使没达到4.15%止盈目标,也能锁定大部分利润。实战中,很多交易会在2-3%的位置被移动止损带出,避免了利润回吐。

成交量过滤器:1倍乘数看似保守,实则精准

成交量必须超过13周期均量才能开仓。这个设计过滤掉了90%的假信号。很多RSI策略在低量环境下频繁开仓,结果被来回打脸。

13周期的成交量均线比常见的20周期更敏感,能更快识别资金流入。1倍乘数看起来不高,但结合8周期RSI的快速反应,已经足够筛选出真正的突破机会。

三重入场条件:不是每个RSI信号都值得交易

多头入场需要满足三个条件之一:RSI动量>14、RSI从超卖区反弹、RSI上穿超卖线。这种设计比单一条件更灵活,适应不同的市场状态。

超卖线设在10,超买线设在90,比传统的30/70更极端。这样做的好处是减少假信号,坏处是可能错过一些机会。但对于剥头皮策略来说,宁可错过也不要做错。

适用场景:高波动品种的短线天堂

这套策略最适合加密货币、外汇主要货币对、热门股票等高波动品种。在低波动的蓝筹股或债券上表现会大打折扣。

最佳时间窗口是欧美交易时段重叠期,此时流动性最好,成交量过滤器最有效。亚洲时段由于成交量偏低,信号质量会下降。

风险警示:连续止损是最大威胁

回测数据显示该策略存在连续亏损风险,特别是在横盘震荡市场中。8周期RSI过于敏感,容易在区间震荡中被反复止损。

建议单次风险敞口不超过账户的2%,并在连续3次止损后暂停交易。历史回测不代表未来收益,实盘交易需要严格的资金管理和心理控制。

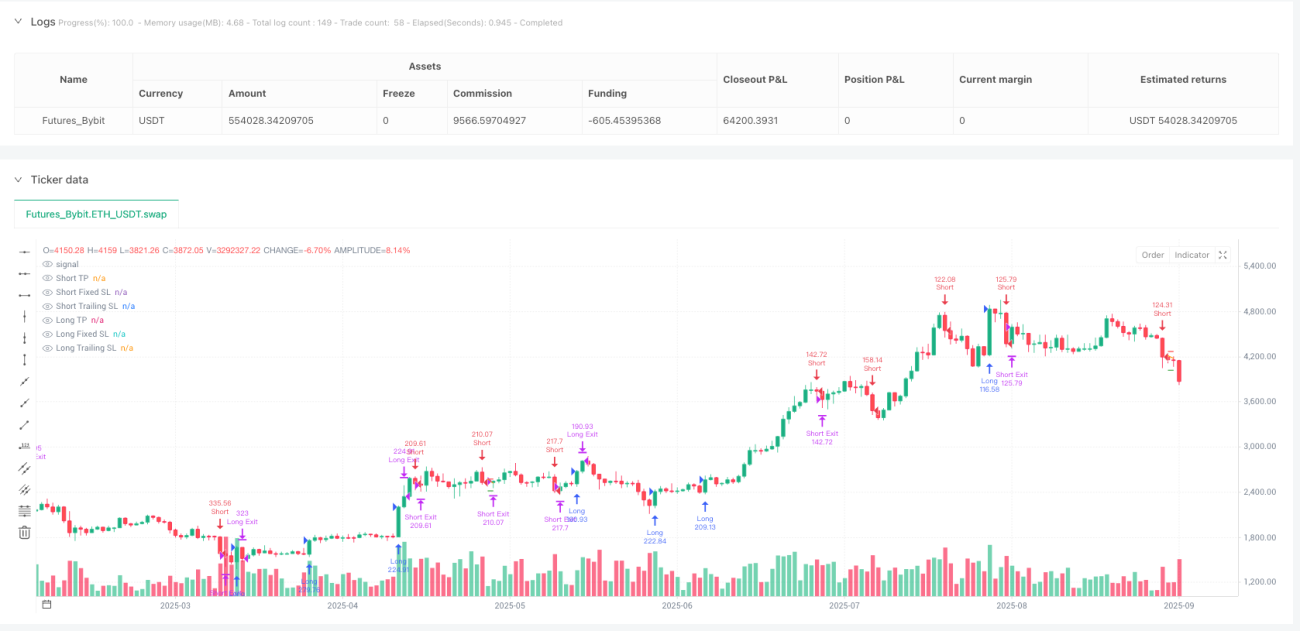

/*backtest

start: 2024-09-29 00:00:00

end: 2025-09-26 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Bybit","currency":"ETH_USDT","balance":500000}]

*/

// This Pine Script® code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © MonkeyPhone

//@version=5- 1