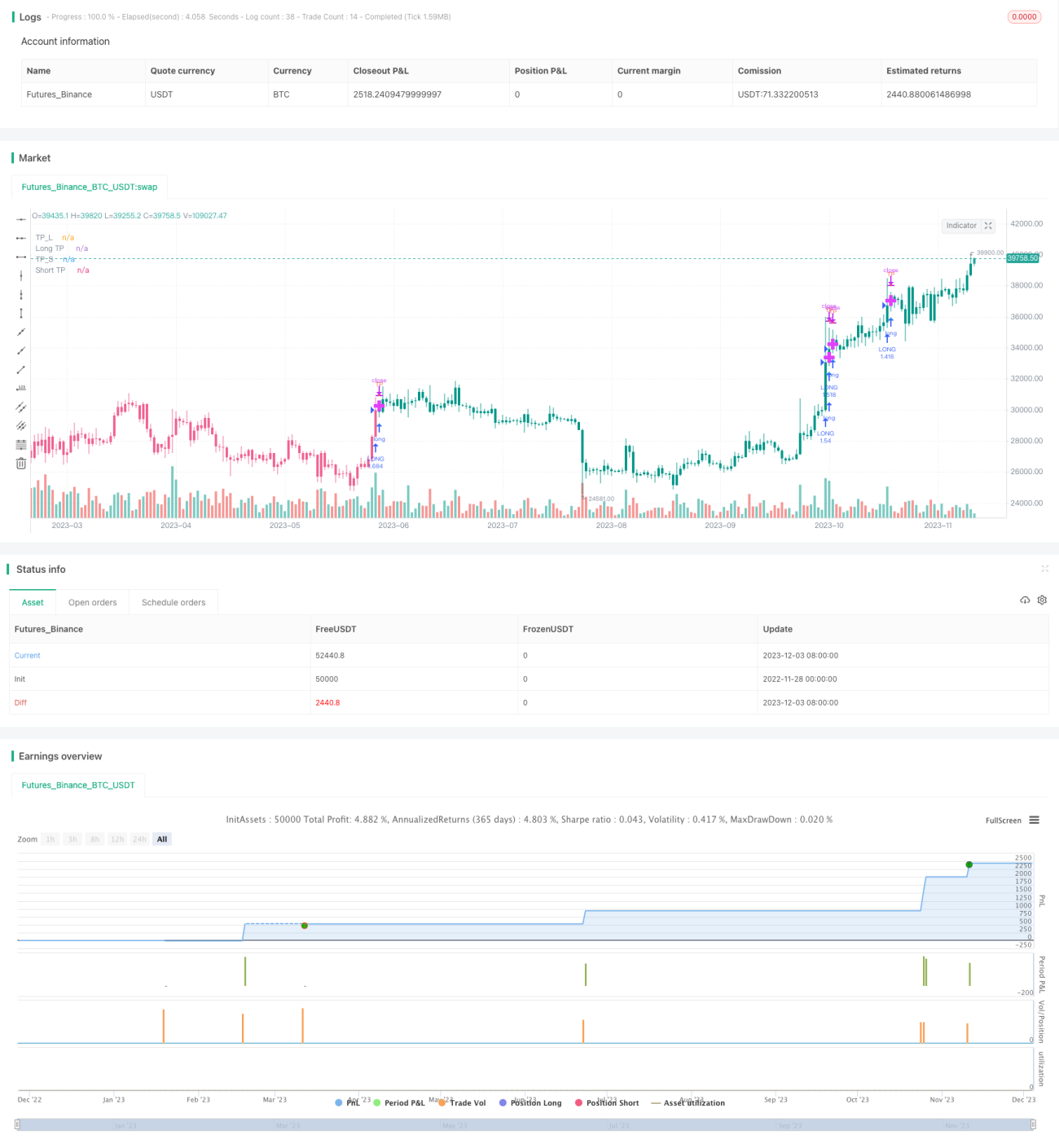

EMA/ADX/VOL - ক্রিপ্টোকারেন্সি কিলার

ইএমএ গড় সিস্টেম ব্যবহার করে ট্রেন্ডের দিকনির্ণয়, ADX ইন্ডিকেটর ব্যবহার করে ট্রেন্ডের শক্তি নির্ণয়, এবং ভলিউম ফিল্টারিংয়ের মাধ্যমে এন্ট্রি করার জন্য একটি কোয়ান্টিটেটিভ ট্রেডিং স্ট্র্যাটেজি

নীতি

এই স্ট্র্যাটেজি প্রথমে ৫টি ভিন্ন সময়কালের ইএমএ গড় ব্যবহার করে দামের ট্রেন্ডের দিকনির্ণয় করে। যখন ৫টি ইএমএ গড় সবগুলোই উপরে যাচ্ছে, তখন বুলিশ ট্রেন্ড গঠিত হয়েছে বলে ধরা হয়। আর যখন ৫টি ইএমএ গড় সবগুলোই নিচে যাচ্ছে, তখন বেয়ারিশ ট্রেন্ড গঠিত হয়েছে বলে ধরা হয়।

এরপর ADX ইন্ডিকেটর ব্যবহার করে ট্রেন্ডের শক্তি নির্ধারণ করা হয়। যখন DI+ লাইন DI- লাইনের উপরে থাকে এবং ADX মান নির্ধারিত থ্রেশহোল্ড অতিক্রম করে, তখন শক্তিশালী বুলিশ অবস্থা ধরা হয়। আর যখন DI- লাইন DI+ লাইনের উপরে থাকে এবং ADX মান নির্ধারিত থ্রেশহোল্ড অতিক্রম করে, তখন বেয়ারিশ অবস্থা ধরা হয়।

একই সাথে, ভলিউমের ব্রেকআউট ব্যবহার করে অতিরিক্ত নিশ্চিতকরণ করা হয়—বর্তমান ক্যান্ডেলের ভলিউম যেন নির্দিষ্ট সময়ের গড় ভলিউমের একটি নির্দিষ্ট গুণের বেশি হয়, যাতে কম ভলিউমের অবস্থানে ভুল এন্ট্রি এড়ানো যায়।

ট্রেন্ডের দিক, ট্রেন্ডের শক্তি এবং ভলিউমের সম্মিলিত বিচারের ভিত্তিতে এই স্ট্র্যাটেজির লং এবং শর্ট পজিশন খোলার লজিক গঠিত হয়।

সুবিধা

-

একক ইএমএ গড়ের তুলনায় পাঁচটি ইএমএ গড়ের সিস্টেম ব্যবহার করে ট্রেন্ডের দিকনির্ণয় আরও নির্ভরযোগ্য।

-

ADX ইন্ডিকেটরের সাহায্যে ট্রেন্ডের শক্তি নির্ধারণ করে স্পষ্ট ট্রেন্ড না থাকলে ভুল এন্ট্রি এড়ানো যায়।

-

ভলিউম ফিল্টারিং মেকানিজম নিশ্চিত করে যে পর্যাপ্ত ভলিউমের সমর্থন আছে, যা স্ট্র্যাটেজির নির্ভরযোগ্যতা বাড়ায়।

-

একাধিক শর্তের সম্মিলিত বিচার এন্ট্রি সিগন্যালকে আরও সঠিক ও নির্ভরযোগ্য করে তোলে।

-

স্ট্র্যাটেজিতে অনেক প্যারামিটার আছে, যা প্যারামিটার অপটিমাইজেশনের মাধ্যমে ক্রমাগত উন্নত করা যায়।

ঝুঁকি ও সমাধান

-

অস্থির বাজারে (রেঞ্জ মার্কেট) EMA গড়, ADX ইত্যাদির বিচার ভুল সিগন্যাল দিতে পারে, ফলে অপ্রয়োজনীয় ক্ষতি হতে পারে। প্যারামিটার যথাযথভাবে সামঞ্জস্য করা বা অন্যান্য ইন্ডিকেটর যুক্ত করে সহায়তা নেওয়া যেতে পারে।

-

ভলিউম ফিল্টারিং শর্ত খুব কঠোর হলে সুযোগ হাতছাড়া হতে পারে; ভলিউম ফিল্টারের প্যারামিটার কমিয়ে আনা যেতে পারে।

-

স্ট্র্যাটেজি থেকে ট্রেড ফ্রিকোয়েন্সি বেশি হতে পারে, তাই অর্থ ব্যবস্থাপনার দিকে নজর দিতে হবে এবং প্রতি ট্রেডে অবস্থানের আকার নিয়ন্ত্রণ করতে হবে।

অপটিমাইজেশনের দিকনির্দেশনা

-

বিভিন্ন প্যারামিটার কম্বিনেশন পরীক্ষা করে সেরা প্যারামিটার খুঁজে বের করা, যা স্ট্র্যাটেজির কার্যকারিতা বাড়ায়।

-

MACD, KDJ ইত্যাদির মতো অন্যান্য ইন্ডিকেটর যোগ করে EMA ও ADX-এর সাথে সমন্বয় করে আরও শক্তিশালী সমন্বিত এন্ট্রি সিদ্ধান্ত নেওয়া।

-

স্টপ লস স্ট্র্যাটেজি যুক্ত করে আরও ঝুঁকি নিয়ন্ত্রণ করা।

-

পজিশন ম্যানেজমেন্ট স্ট্র্যাটেজি অপটিমাইজ করে আরও বৈজ্ঞানিক অর্থ ব্যবস্থাপনা প্রয়োগ করা।

সারসংক্ষেপ

এই স্ট্র্যাটেজি দামের ট্রেন্ডের দিক, ট্রেন্ডের শক্তি এবং ভলিউম তথ্য সমন্বিতভাবে বিবেচনা করে এন্ট্রি নিয়ম তৈরি করে, যা কিছুটা হলেও সাধারণ ভুল ফাঁদে পড়া এড়ায় এবং যথেষ্ট নির্ভরযোগ্যতা রাখে। তবে প্যারামিটার অপটিমাইজেশন, ইন্ডিকেটর নির্বাচন এবং ঝুঁকি ব্যবস্থাপনার মাধ্যমে স্ট্র্যাটেজি সিস্টেমকে আরও পরিমার্জিত করে কার্যকারিতা বাড়ানোর প্রয়োজন। সামগ্রিকভাবে, এই স্ট্র্যাটেজি ফ্রেমওয়ার্কের বিস্তৃত সম্প্রসারণ সম্ভাবনা এবং অপটিমাইজেশনের সুযোগ রয়েছে।

- 1