Strategie für einen doppelten gleitenden Durchschnitt mit mehreren Symbolen (Teaching)

Schriftsteller:- Ich bin ein Idiot., Erstellt: 2022-04-07 16:14:35, Aktualisiert: 2022-04-08 09:13:58Strategie für einen doppelten gleitenden Durchschnitt mit mehreren Symbolen (Teaching)

Auf Anfrage unserer Benutzer in den Foren, dass sie eine Multi-Symbol-Doppel-Durchschnitts-Strategie als Designreferenz haben möchten, wird eine Multi-Symbol-Doppel-Durchschnitts-Strategie in der heutigen Freigabe implementiert.

Strategisches Denken

Die Logik der doppelten gleitenden Durchschnittsstrategie ist sehr einfach, d.h. zwei gleitende Durchschnitte. Ein gleitender Durchschnitt mit einer kleinen Periode (schnelle Linie) und ein gleitender Durchschnittswert mit einer großen Periode (langsamer Linie). Wenn die beiden Linien ein goldenes Kreuz haben (die schnelle Linie überquert die langsame Linie von unten), kaufen Sie lang und wenn die beiden Linien ein totes Kreuz haben (die schnelle Linie überquert die langsame Linie von oben), verkaufen Sie kurz. Für den gleitenden Durchschnitt verwenden wir EMA.

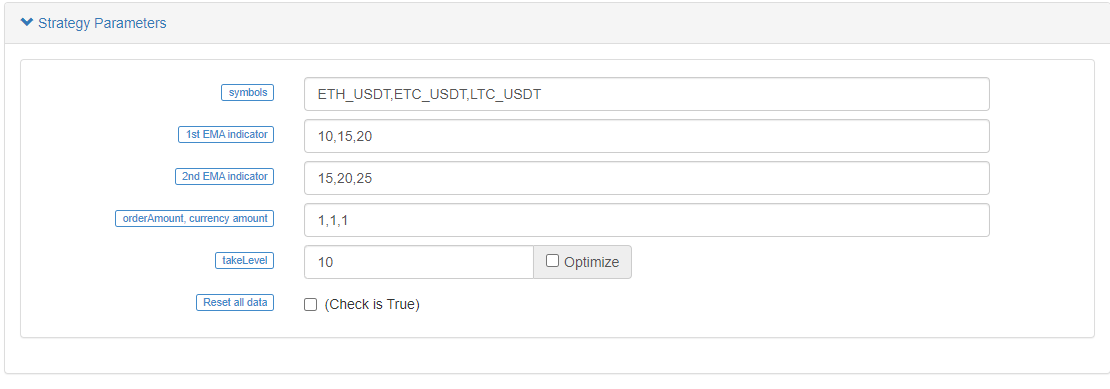

Es ist nur so, dass die Strategie für mehrere Symbole konzipiert werden muss, so dass die Parameter verschiedener Symbole unterschiedlich sein können (verschiedene Symbole verwenden unterschiedliche gleitende Durchschnittsparameter), so dass es notwendig ist, Parameter in einem

Die Parameter sind in Form einer Zeichenfolge, wobei jeder Parameter durch ein Komma getrennt ist, entworfen. Diese Zeichenfolge werden analysiert, wenn die Strategie ausläuft, die mit der Ausführungslogik für jedes Symbol (Handelspaar) abgestimmt wird. Strategie-Umfrage erkennt die Marktkurse aller Symbole, den Auslöser der Handelsbedingungen und den Chartdruck. Nachdem alle Symbole einmal befragt wurden, werden die Daten aggregiert und die Tabelleninformationen werden in der Statusleiste angezeigt.

Die Strategie ist super einfach gestaltet und sehr für Anfänger geeignet; sie umfasst insgesamt nur mehr als 200 Zeilen.

Strategie-Code

// function effect: to cancel all pending orders of the current trading pair

function cancelAll(e) {

while (true) {

var orders = _C(e.GetOrders)

if (orders.length == 0) {

break

} else {

for (var i = 0 ; i < orders.length ; i++) {

e.CancelOrder(orders[i].Id, orders[i])

Sleep(500)

}

}

Sleep(500)

}

}

// function effect: to calculate the real-time profit and loss

function getProfit(account, initAccount, lastPrices) {

// account indicates the current account information; initAccount is the initial account information; lastPrices is the the latest prices of all current symbols

var sum = 0

_.each(account, function(val, key) {

// traverse the current total assets, and calculate asset currency (except USDT) difference and amount difference

if (key != "USDT" && typeof(initAccount[key]) == "number" && lastPrices[key + "_USDT"]) {

sum += (account[key] - initAccount[key]) * lastPrices[key + "_USDT"]

}

})

// return the asset profit and loss calculated by the current price

return account["USDT"] - initAccount["USDT"] + sum

}

// function effect: to generate chart configuration

function createChartConfig(symbol, ema1Period, ema2Period) {

// symbol indicates trading pair; ema1Period indicates the first EMA period; ema2Period indicates the second EMA period

var chart = {

__isStock: true,

extension: {

layout: 'single',

height: 600,

},

title : { text : symbol},

xAxis: { type: 'datetime'},

series : [

{

type: 'candlestick', // K-line date series

name: symbol,

id: symbol,

data: []

}, {

type: 'line', // EMA data series

name: symbol + ',EMA1:' + ema1Period,

data: [],

}, {

type: 'line', // EMA data series

name: symbol + ',EMA2:' + ema2Period,

data: []

}

]

}

return chart

}

function main() {

// reset all data

if (isReset) {

_G(null) // vacuum all persistently recorded data

LogReset(1) // vacuum all logs

LogProfitReset() // vacuum all profit logs

LogVacuum() // release the resource occupied by the bot database

Log("reset all data", "#FF0000") // print information

}

// parse parameters

var arrSymbols = symbols.split(",") // use comma to split the trading symbol strings

var arrEma1Periods = ema1Periods.split(",") // split the string of the first EMA parameter

var arrEma2Periods = ema2Periods.split(",") // split the string of the second EMA parameter

var arrAmounts = orderAmounts.split(",") // split the order amount of each symbol

var account = {} // the variable used to record the current asset information

var initAccount = {} // the variable used to record the initial asset information

var currTradeMsg = {} // the variable used to record whether the current BAR is executed

var lastPrices = {} // the variable used to record the latest price of the monitored symbol

var lastBarTime = {} // the variable used to record the time of the latest BAR, to judge the BAR update during plotting

var arrChartConfig = [] // the variable used to record the chart configuration information, to plot

if (_G("currTradeMsg")) { // for example, when restart, recover currTradeMsg data

currTradeMsg = _G("currTradeMsg")

Log("recover GetRecords", currTradeMsg)

}

// initialize account

_.each(arrSymbols, function(symbol, index) {

exchange.SetCurrency(symbol)

var arrCurrencyName = symbol.split("_")

var baseCurrency = arrCurrencyName[0]

var quoteCurrency = arrCurrencyName[1]

if (quoteCurrency != "USDT") {

throw "only support quoteCurrency: USDT"

}

if (!account[baseCurrency] || !account[quoteCurrency]) {

cancelAll(exchange)

var acc = _C(exchange.GetAccount)

account[baseCurrency] = acc.Stocks

account[quoteCurrency] = acc.Balance

}

// initialize the related data of chart

lastBarTime[symbol] = 0

arrChartConfig.push(createChartConfig(symbol, arrEma1Periods[index], arrEma2Periods[index]))

})

if (_G("initAccount")) {

initAccount = _G("initAccount")

Log("recover initial account information", initAccount)

} else {

// use the current asset information to initialize initAccount (variable)

_.each(account, function(val, key) {

initAccount[key] = val

})

}

Log("account:", account, "initAccount:", initAccount) // print asset information

// initialize the chart objects

var chart = Chart(arrChartConfig)

// reset chart

chart.reset()

// strategy logic of the main loop

while (true) {

// traverse all symbols, and execute the dual moving average logic one by one

_.each(arrSymbols, function(symbol, index) {

exchange.SetCurrency(symbol) // switch the trading pair to the trading pair recorded by by symbol string

var arrCurrencyName = symbol.split("_") // split trading pairs by "_"

var baseCurrency = arrCurrencyName[0] // string of base currency

var quoteCurrency = arrCurrencyName[1] // string of quote currency

// according to index, obtain the EMA paramater of the current trading pair

var ema1Period = parseFloat(arrEma1Periods[index])

var ema2Period = parseFloat(arrEma2Periods[index])

var amount = parseFloat(arrAmounts[index])

// obtain the K-line data of the current trading pair

var r = exchange.GetRecords()

if (!r || r.length < Math.max(ema1Period, ema2Period)) { // when the length of K-line is not long enough, return directly

Sleep(1000)

return

}

var currBarTime = r[r.length - 1].Time // record the current BAR timestamp

lastPrices[symbol] = r[r.length - 1].Close // record the current latest price

var ema1 = TA.EMA(r, ema1Period) // calculate EMA indicator

var ema2 = TA.EMA(r, ema2Period) // calculate EMA indicator

if (ema1.length < 3 || ema2.length < 3) { // when the length of EMA indicator array is too short, return derectly

Sleep(1000)

return

}

var ema1Last2 = ema1[ema1.length - 2] // EMA on the second last BAR

var ema1Last3 = ema1[ema1.length - 3] // EMA on the third last BAR

var ema2Last2 = ema2[ema2.length - 2]

var ema2Last3 = ema2[ema2.length - 3]

// write the chart data

var klineIndex = index + 2 * index

// traverse k-line data

for (var i = 0 ; i < r.length ; i++) {

if (r[i].Time == lastBarTime[symbol]) { // plot; update the current BAR and its indicator

// update

chart.add(klineIndex, [r[i].Time, r[i].Open, r[i].High, r[i].Low, r[i].Close], -1)

chart.add(klineIndex + 1, [r[i].Time, ema1[i]], -1)

chart.add(klineIndex + 2, [r[i].Time, ema2[i]], -1)

} else if (r[i].Time > lastBarTime[symbol]) { // plot; add BAR and its indicator

// add

lastBarTime[symbol] = r[i].Time // update the timestamp

chart.add(klineIndex, [r[i].Time, r[i].Open, r[i].High, r[i].Low, r[i].Close])

chart.add(klineIndex + 1, [r[i].Time, ema1[i]])

chart.add(klineIndex + 2, [r[i].Time, ema2[i]])

}

}

if (ema1Last3 < ema2Last3 && ema1Last2 > ema2Last2 && currTradeMsg[symbol] != currBarTime) {

// golden cross

var depth = exchange.GetDepth() // obtain the depth data of the current order book

var price = depth.Asks[Math.min(takeLevel, depth.Asks.length)].Price // select the 10th level price; taker

if (depth && price * amount <= account[quoteCurrency]) { // obtain that the depth data is normal, and the assets are enough to place an order

exchange.Buy(price, amount, ema1Last3, ema2Last3, ema1Last2, ema2Last2) // maker; buy

cancelAll(exchange) // cancel all pending orders

var acc = _C(exchange.GetAccount) // obtain the account asset information

if (acc.Stocks != account[baseCurrency]) { // detect the account assets changed

account[baseCurrency] = acc.Stocks // update assets

account[quoteCurrency] = acc.Balance // update assets

currTradeMsg[symbol] = currBarTime // record the current BAR has been executed

_G("currTradeMsg", currTradeMsg) // persistently record

var profit = getProfit(account, initAccount, lastPrices) // calculate profit

if (profit) {

LogProfit(profit, account, initAccount) // print profit

}

}

}

} else if (ema1Last3 > ema2Last3 && ema1Last2 < ema2Last2 && currTradeMsg[symbol] != currBarTime) {

// death cross

var depth = exchange.GetDepth()

var price = depth.Bids[Math.min(takeLevel, depth.Bids.length)].Price

if (depth && amount <= account[baseCurrency]) {

exchange.Sell(price, amount, ema1Last3, ema2Last3, ema1Last2, ema2Last2)

cancelAll(exchange)

var acc = _C(exchange.GetAccount)

if (acc.Stocks != account[baseCurrency]) {

account[baseCurrency] = acc.Stocks

account[quoteCurrency] = acc.Balance

currTradeMsg[symbol] = currBarTime

_G("currTradeMsg", currTradeMsg)

var profit = getProfit(account, initAccount, lastPrices)

if (profit) {

LogProfit(profit, account, initAccount)

}

}

}

}

Sleep(1000)

})

// variables in the table of status bar

var tbl = {

type : "table",

title : "account information",

cols : [],

rows : []

}

// write the data in the table structure of status bar

tbl.cols.push("--")

tbl.rows.push(["initial"])

tbl.rows.push(["current"])

_.each(account, function(val, key) {

if (typeof(initAccount[key]) == "number") {

tbl.cols.push(key)

tbl.rows[0].push(initAccount[key]) // initial

tbl.rows[1].push(val) // current

}

})

// display the status bar table

LogStatus(_D(), "\n", "profit:", getProfit(account, initAccount, lastPrices), "\n", "`" + JSON.stringify(tbl) + "`")

}

}

Strategie-Backtest

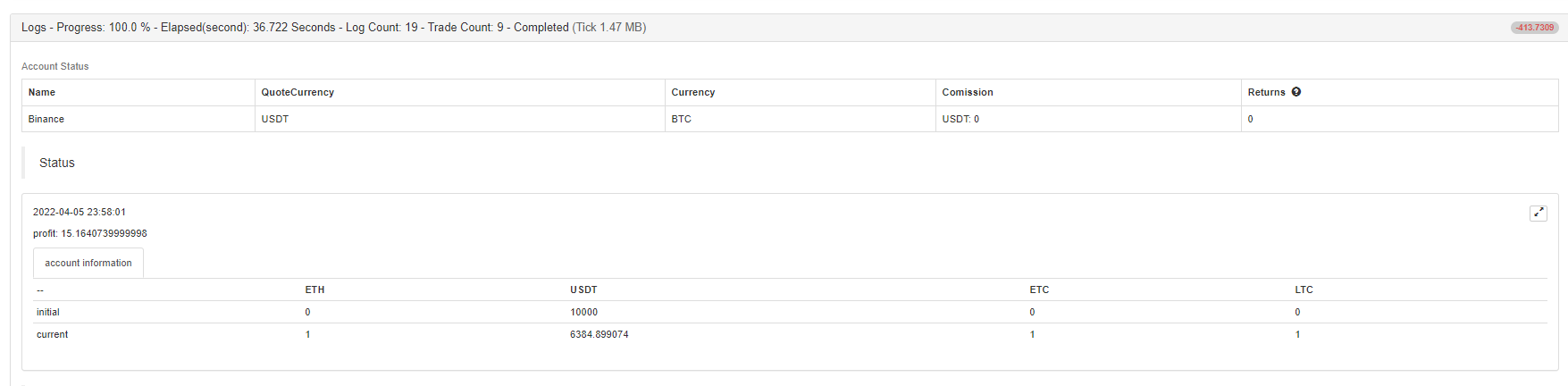

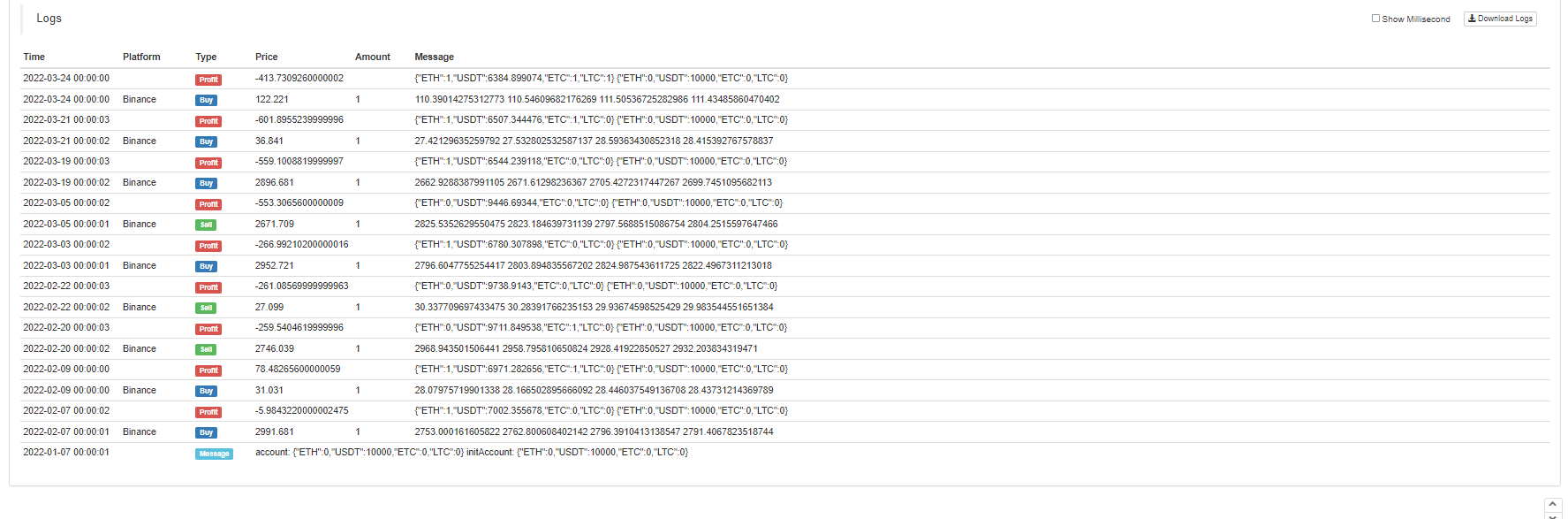

Sie können sehen, dass ETH, LTC und ETC alle Trades nach den Auslösern des goldenen Kreuzes und des Todeskreuzes der gleitenden Durchschnitte hatten.

Sie können auch auf simulierten Bot warten, um zu testen.

Strategie-Quellcode:https://www.fmz.com/strategy/333783

Die Strategie wird nur für Backtest und Strategie-Design-Lernen verwendet, also verwenden Sie sie in einem Bot mit Vorsicht.

- Eine Plattform, die auf FMZ basiert.

- Kryptowährungs-Kontrakt einfacher Auftragsüberwachungsbot

- Wenn Sie mit getdepth die entsprechende Zeitschrift erhalten möchten

- Ignoriert, gelöst

- Die Frage nach dem Gesichtswert

- dYdX-Strategie-Entwurfsbeispiel

- Erste Erforschung der Anwendung von Python Crawler auf FMZ

Crawling Binance Ankündigungsinhalt - Hedge-Strategie-Design-Forschung & Beispiel für offene Spot- und Futures-Orders

- Aktuelle Situation und empfohlene Anwendung der Finanzierungsrate-Strategie

- Strategie für einen doppelten gleitenden Durchschnitts-Brechpunkt von Kryptowährungs-Futures (Teaching)

- Realisierung von Fisher Indicator in JavaScript und Plotting auf FMZ

- Treuhänder

- 2021 Kryptowährungs-TAQ-Überprüfung & Einfachste verpasste Strategie der 10-fachen Erhöhung

- Kryptowährungs-Futures Multi-Symbol ART-Strategie (Lehre)

- Aktualisieren! Kryptowährungs Futures Martingale Strategie

- Die Getrecords-Funktion kann keine K-Stringkarte in Sekunden erhalten

- Konstruktion eines FMZ-basierten Auftragsmanagementsystems (2)

- Die Volumen-Daten, die Getticker zurückgegeben hat, sind falsch.

- Gestaltung eines FMZ-basierten Auftragssynchronmanagementsystems (1)

- Entwerfen Sie eine Bibliothek mit mehreren Diagrammen