Multi-Indikator-Trendfolgestrategie

Übersicht

Diese Strategie kombiniert drei Open-Source-Indikatoren, um Trendentscheidungen über mehrere Zeitrahmen hinweg zu treffen, und setzt Stop-Loss und Take-Profit zur Gewinnsicherung ein. Konkret wird der AK MACD BB Indikator verwendet, um die kurzfristige Trendrichtung zu bestimmen, der SSL Indikator filtert einige Fehlsignale heraus, und schließlich wird der Volumenindikator VSF genutzt, um die tatsächliche Kauf- und Verkaufsdynamik zu beurteilen und so den Einstiegszeitpunkt zu bestimmen. Gleichzeitig sind im Strategie voreingestellte Stop-Loss- und Take-Profit-Punkte enthalten, die das Verlustrisiko pro Trade erheblich reduzieren.

Strategieprinzip

-

AK MACD BB Indikator

Dieser Indikator wendet Bollinger-Bänder auf den MACD Indikator an. Wenn die MACD-Linie die obere Grenze des Bollinger-Bands durchbricht, wird ein Kaufsignal generiert; beim Bruch der unteren Grenze ein Verkaufssignal. -

SSL Indikator

Der SSL Indikator erkennt, ob der Preis einen gleitenden Durchschnitt durchbricht, und prüft Retest-Signale. Wenn der Preis den gleitenden Durchschnitt von unten nach oben durchbricht und der SSL Indikator blau ist, liegt ein Aufwärtstrend vor; bei einem Bruch von oben nach unten und rotem Indikator ein Abwärtstrend. Daraus werden Handelssignale abgeleitet. -

VSF Indikator

Der VSF Indikator beurteilt die Stärke von Käufern und Verkäufern. Die Strategie gibt nur dann ein Signal, wenn die Kauf- oder Verkaufsstärke über 50 % liegt, um ungültige Ausbrüche zu vermeiden. -

Stop-Loss und Take-Profit

Die Strategie verfügt über vier progressive Take-Profit-Stufen, die von 1,5-fachem bis 3-fachem Gewinnabstand reichen. Zudem wird ein fester Stop-Loss von 2 % gesetzt, um den maximalen Verlust pro Trade wirksam zu begrenzen.

Vorteile

-

Hohe Treffsicherheit durch Kombination mehrerer Indikatoren

Durch die Nutzung verschiedener Indikatoren zur Trendbestimmung über mehrere Zeitrahmen können Fehlsignale gefiltert werden, was die Genauigkeit erhöht. -

Automatischer Take-Profit und Stop-Loss – kontrolliertes Risiko

Die integrierten Take-Profit- und Stop-Loss-Einstellungen halten den Verlust pro Trade bei etwa 2 % und vermeiden große Verluste. -

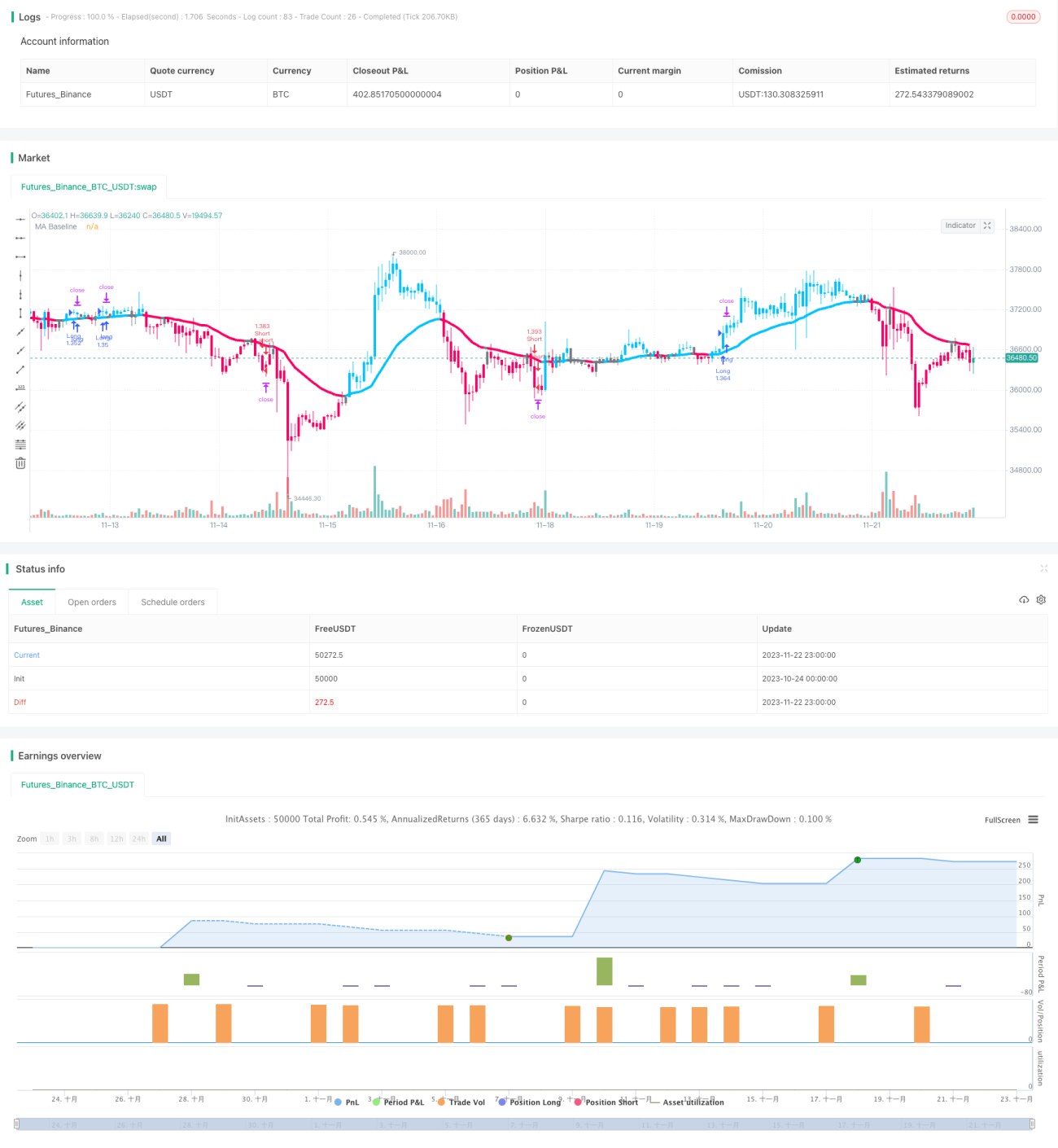

Hervorragende Backtest-Ergebnisse

Laut Backtest des Verfassers waren 74 % von 100 Trades profitabel, mit einem Gesamtgewinn von 427 %.

Risiken und Gegenmaßnahmen

-

Risiko extremer Marktvolatilität

Bei großen Seitwärtsbewegungen kann es zu mehreren kleinen Verlusten kommen. In diesem Fall kann der feste Stop-Loss angepasst oder der Handel ausgesetzt werden. -

Eingeschränkte Long-/Short-Möglichkeiten

Die Strategie erlaubt sowohl Long- als auch Short-Positionen. Wenn nur eine Richtung erlaubt ist, halbiert sich die Anzahl potenziell profitabler Gelegenheiten. -

Handelszeitenrisiko

Die Strategie verwendet 5-Minuten-Daten. Stehen an einem Handelstag nur wenige Stunden Daten zur Verfügung, ist die Stichprobe zu klein und die Signale könnten unzuverlässig sein.

Optimierungsmöglichkeiten

-

Optimierung der Stop-Loss- und Take-Profit-Parameter

Durch Tests verschiedener Stop-Loss- und Take-Profit-Werte können optimale Parameter gefunden werden. Ein zu kleiner Stop-Loss kann das Risiko nicht ausreichend begrenzen, ein zu großer Stop-Loss kann größere Gewinne verhindern. -

Erweiterung um automatische Positionsanpassung

Es können trailing Stops oder dynamische Stops eingesetzt werden, um Gewinne zu sichern. Auch das Nachkaufen unter bestimmten Bedingungen könnte die Gewinne steigern. -

Kombination mit weiteren Indikatoren

Unterschiedliche Indikatorkombinationen können getestet werden, um die effektivste zu ermitteln. Auch die Einbeziehung weiterer Indikatoren zur Kreuzvalidierung ist möglich. -

Parameteroptimierung

Durch Backtests mit verschiedenen Parametern lassen sich Optimierungsrichtungen finden. In dieser Strategie könnten Änderungen der Bollinger-Band- oder Gleitender-Durchschnitts-Parameter zu besseren Ergebnissen führen.

Zusammenfassung

Diese Strategie integriert mehrere Indikatoren zur Trendbestimmung, setzt automatische Take-Profit- und Stop-Loss-Grenzen und ermöglicht es, in starken Trends Gewinne zu erzielen, während das Verlustrisiko pro Trade sehr gering gehalten wird. Laut den Backtest-Daten des Verfassers sind die Gewinnrate und die Rentabilität sehr vielversprechend. Durch gezielte Optimierungen kann die Stabilität und Rentabilität der Strategie weiter verbessert werden.

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © myn

//@version=5

strategy('Strategy Myth-Busting #7 - MACDBB+SSL+VSF - [MYN]', max_bars_back=5000, overlay=true, pyramiding=0, initial_capital=1000, currency='USD', default_qty_type=strategy.percent_of_equity, default_qty_value=1.0, commission_value=0.075, use_bar_magnifier = false)

/////////////////////////////////////

//* Put your strategy logic below *//

/////////////////////////////////////

//nwVqTuPe6yo- 1