Nota de la API del intercambio BitMEX

El autor:Las hierbas, Creado: 2019-04-04 11:40:52, Actualizado: 2024-02-05 20:09:52Nota de uso de la API del intercambio BitMEX

La plataforma de FMZ Doc API Únete a nosotros en el grupo telegrama

www.fmz.com(anteriormente BotVs) es una plataforma de trading de estrategias cuantitativas donde puedes aprender, escribir, compartir y negociar estrategias cuantitativas fácilmente.

-

Nuestra plataforma tiene muchas ventajas:

- 1, multiplataforma, soporte a todos los principales intercambios comerciales, la estrategia escrita en nuestra plataforma es adecuada para todos los principales intercambios.

- 2、Fácil de empezar, la documentación específica de la API y las estrategias clásicas de plantillas ayudan a los usuarios a comenzar muy rápido.

- 3■Tiene un sistema eficaz de simulación de pruebas de retroceso.

- 4、Apoyo para enviar correos electrónicos, enviar mensajes a su teléfono.

- 5, mecanismo de control basado en la web, se puede acceder a través de su teléfono.

- Apoyo para la programación completa de Python\C++\JavaScript

- 7、Apoyar el comercio de spot y futuros, y apoyará más intercambios en el futuro.

- 8、El costo es extremadamente bajo. 0,125 RMB por hora, basado en el tipo de cambio actual: USDCNY 6,9303, lo que significa 0,01804 dólares por hora.

- 9、No se guardan API-KEY ni contraseñas en nuestro sitio web. FMZ ha estado funcionando durante más de cuatro años sin ningún problema de seguridad.

FMZ (BOTVS) ahora es compatible con todos los contratos de BitMEX!

-

El código de prueba:

var initAccount = null;

var nowAccount = null;

function main() {

LogReset(1);

Log("This is BitMEX test bot");

Log("Fee:", exchange.GetFee());

Log("Initial account:", initAccount = _C(exchange.GetAccount));

var info = exchange.SetContractType("XBTUSD"); // BitMEX : XBTUSD , OK : this_week

Log("XBTUSD info:", info);

Log("Use GetTicker to get ticker information:", _C(exchange.GetTicker))

Sleep(1000 * 10);

// make an order

exchange.SetDirection("sell"); // set order direction

var orderId = exchange.Sell(-1, 1); // sell at market price。

Sleep(6000);

// log positions

var positions = null;

Log(positions = _C(exchange.GetPosition));

Log("Account before changing leverage:", _C(exchange.GetAccount));

// change leverage

Log("Change leverage", _C(exchange.SetMarginLevel, positions[0].MarginLevel * 2));

Log("Account after changing leverage:", _C(exchange.GetAccount));

// test GetOrder

if (orderId) {

Log(_C(exchange.GetOrder, orderId));

}

Sleep(1000 * 10);

Log(_C(exchange.GetPosition));

// set direction to close

exchange.SetDirection("closesell");

var go_buy = exchange.Go("Buy", -1, 1);

var orderId2 = go_buy.wait();

Log(_C(exchange.GetOrder, orderId2));

Log("Current account:", nowAccount = _C(exchange.GetAccount));

Log(_C(exchange.GetPosition));

LogProfit(nowAccount.Stocks - initAccount.Stocks, " initAccount:", initAccount, " nowAccount:", nowAccount);

Sleep(1000 * 10);

var ticker = _C(exchange.GetTicker);

exchange.SetDirection("buy");

exchange.Buy(ticker.Last - 50, 1);

exchange.SetDirection("sell");

exchange.Sell(ticker.Last + 50, 1);

// GetOrders

Log("Test GetOrders:", _C(exchange.GetOrders));

var e = exchange;

while (true) {

var orders = _C(e.GetOrders);

if (orders.length === 0) {

break;

}

Sleep(500);

for (var j = 0; j < orders.length; j++) {

e.CancelOrder(orders[j].Id);

if (j < (orders.length - 1)) {

Sleep(500);

}

}

}

Log("Cancel order, test GetOrders again:", _C(exchange.GetOrders));

}

-

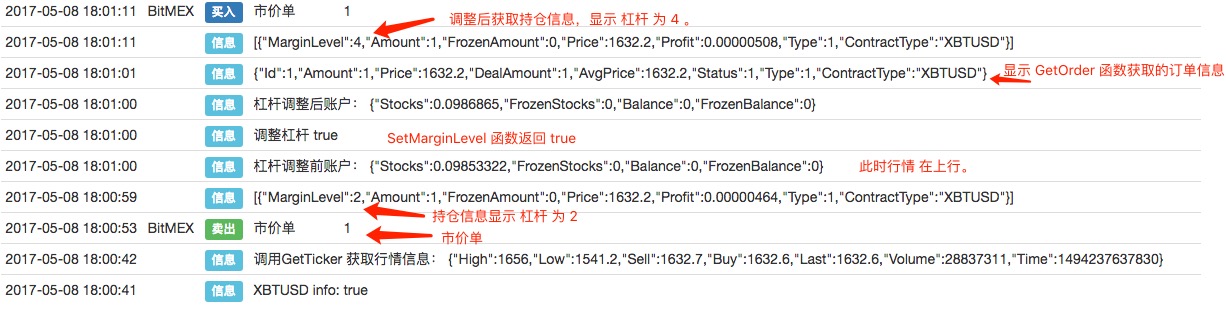

Compruebe la información de su cuenta en BitMEX.

Registra la información por bot, que es el mismo que en BitMEX.

-

Log positions after changing leverage, the leverage has been changed (Log posiciones después de cambiar el apalancamiento, el apalancamiento ha sido cambiado).

-

Use Go function to cover your positions at the same time (Utilice la función Go para cubrir sus posiciones al mismo tiempo).

exchange.SetDirection("closesell"); var go_buy = exchange.Go("Buy", -1, 1); var orderId2 = go_buy.wait(); Log(_C(exchange.GetOrder, orderId2)); Log("当前账户:", nowAccount = _C(exchange.GetAccount)); Log(_C(exchange.GetPosition)); LogProfit(nowAccount.Stocks - initAccount.Stocks, " initAccount:", initAccount, " nowAccount:", nowAccount);

-

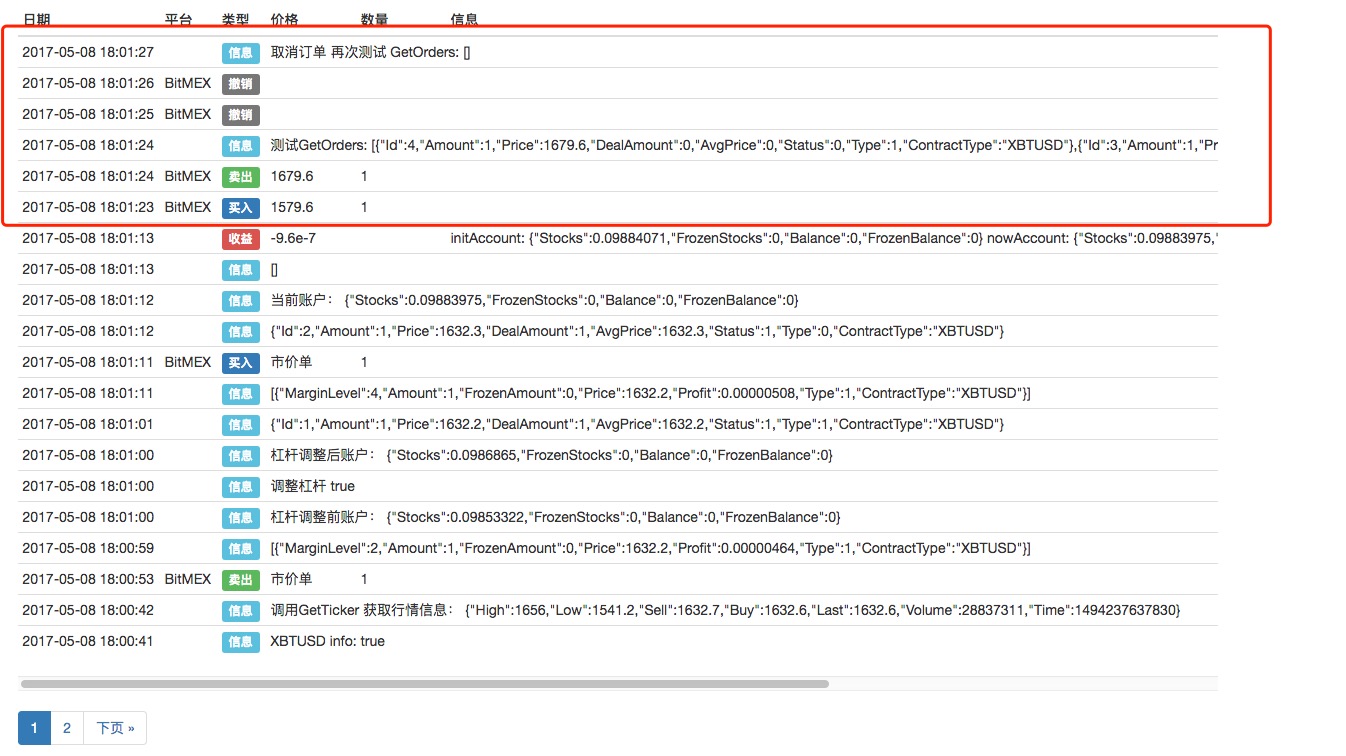

Let's try post orders and cancel it. (Vamos a intentar hacer pedidos por correo y cancelarlos)

var ticker = _C(exchange.GetTicker); exchange.SetDirection("buy"); exchange.Buy(ticker.Last - 50, 1); exchange.SetDirection("sell"); exchange.Sell(ticker.Last + 50, 1); // GetOrders Log("Test GetOrders:", _C(exchange.GetOrders)); var e = exchange; while (true) { var orders = _C(e.GetOrders); if (orders.length === 0) { break; } Sleep(500); for (var j = 0; j < orders.length; j++) { e.CancelOrder(orders[j].Id); if (j < (orders.length - 1)) { Sleep(500); } } } Log("orders have been canceled. Now check orders again, order array is empty. GetOrders:", _C(exchange.GetOrders));

The pending orders

information (La información de pedidos pendientes fue obtenida).

[{"Id":4,"Amount":1,"Price":1679.6,"DealAmount":0,"AvgPrice":0,"Status":0,"Type":1,"ContractType":"XBTUSD"},

{"Id":3,"Amount":1,"Price":1579.6,"DealAmount":0,"AvgPrice":0,"Status":0,"Type":0,"ContractType":"XBTUSD"}]

-

Nota: No se puede hacer nada.

-

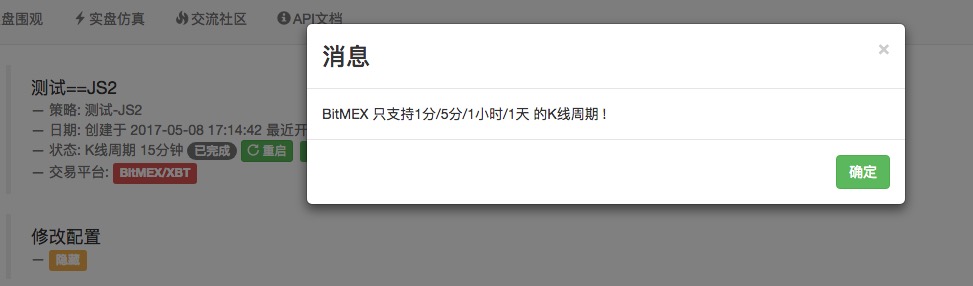

BitMEX sólo soporta K-line periodes de 1m, 5m, 1h, 1d.

Usando los últimos hosts, el substrato puede sintetizar K-lines automáticamente, y algunos datos de ciclos de K-lines que no son compatibles con BITMEX también pueden sintetizarse, por lo que no se limita a la configuración de ciclos de K-lines.

1分钟、5分钟、1小时、1天Estos ciclos, todos los ciclos pueden ser configurados.

-

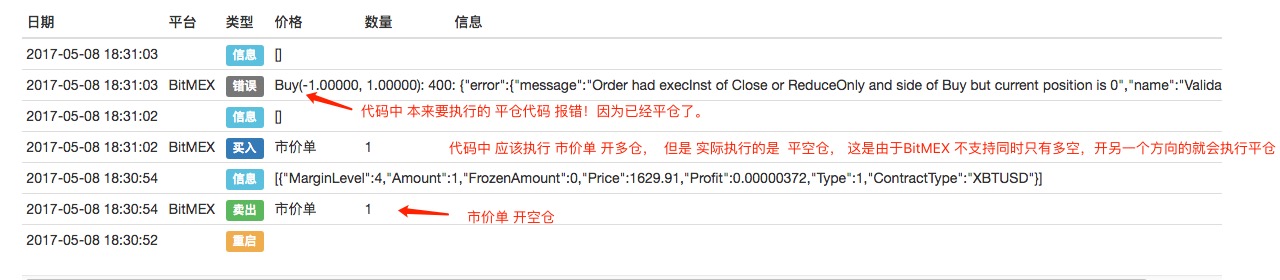

2, Test holding long and short positions at the same time. (Teste manteniendo posiciones largas y cortas al mismo tiempo)

LogReset(1); var info = exchange.SetContractType("XBTUSD"); exchange.SetDirection("sell"); var orderId = exchange.Sell(-1, 1); Log(_C(exchange.GetPosition)); Sleep(1000*6); exchange.SetDirection("buy"); var orderId2 = exchange.Buy(-1, 1); Log(_C(exchange.GetPosition)); exchange.SetDirection("closesell"); var orderId3 = exchange.Buy(-1, 1); Log(_C(exchange.GetPosition));

-

3. El apalancamiento puede ser cambiado mientras se mantiene la posición.

-

4■ Apoyoexchange.IOFunción para más API.

// exchange.IO example exchange.SetContractType("XBTUSD"); Log(exchange.IO("api", "POST", "position/leverage", "symbol=XBTUSD&leverage=4")); Log(exchange.IO("api", "GET", "user"));The raw information of position/leverage API (La información cruda de la API de posición/apalancamiento)

{"homeNotional":0, "sessionMargin":0, "bankruptPrice":null, "initMarginReq":0.25, "execBuyQty":2, "execComm":184, "unrealisedCost":0, "commission":0.00075, "leverage":4, "posLoss":0, "posMargin":0, "posMaint":0, "liquidationPrice":null, "maintMarginReq":0.005, "grossExecCost":0, "execCost":7, "currentTimestamp":"2017-05-08T10:51:20.576Z", "markValue":0, "unrealisedGrossPnl":0, "taxBase":7720, "unrealisedPnlPcnt":0, "prevUnrealisedPnl":0, "openOrderSellCost":0, "deleveragePercentile":null, "openingComm":31588, "openOrderBuyCost":0, "posCross":0, "taxableMargin":0, "simpleCost":0, "underlying":"XBT", "quoteCurrency":"USD", "execBuyCost":122613, "execSellCost":122620, "execQty":0, "realisedCost":-7720, "unrealisedPnl":0, "openingQty":0, "openOrderBuyQty":0, "initMargin":0, "unrealisedTax":0, "simpleQty":0, "avgCostPrice":null, "rebalancedPnl":24052, "openingTimestamp":"2017-05-08T10:00:00.000Z", "unrealisedRoePcnt":0, "posCost":0, "posInit":0, "posComm":0, "realisedTax":0, "indicativeTax":0, "breakEvenPrice":null, "isOpen":false, "riskValue":0, "posState":"", "varMargin":0, "realisedGrossPnl":7720, "timestamp":"2017-05-08T10:51:20.576Z", "account":25992, "foreignNotional":0, "openOrderSellPremium":0, "simpleValue":0, "lastValue":0, "riskLimit":20000000000, "openOrderSellQty":0, "grossOpenPremium":0, "marginCallPrice":null, "prevClosePrice":1562.74, "openOrderBuyPremium":0, "currentQty":0, "currentCost":-7720, "currentComm":31772, "markPrice":null, "posCost2":0, "realisedPnl":-24052, "prevRealisedPnl":-95, "execSellQty":2, "shortBankrupt":0, "simplePnl":0, "simplePnlPcnt":0, "lastPrice":null, "posAllowance":0, "targetExcessMargin":0, "indicativeTaxRate":0, "grossOpenCost":0, "maintMargin":0, "crossMargin":false, "openingCost":-7727, "longBankrupt":0, "avgEntryPrice":null, "symbol":"XBTUSD", "currency":"XBt"}

-

- Tutorial para principiantes de FMZ

- Comienzo rápido de las operaciones cuantitativas

- Solicita API de intercambio, ocasionalmente aparece un tiempo de espera

- Indicadores de Aroon: cómo usarlos para el comercio de criptomonedas

- ¿Cómo elegir una plataforma de intercambio cuantitativo?

- Implementación de MACD en Python

- OKEX obtener profundidad error

- ¿Puede hacerse una prueba?

- ZBG no está disponible

- ¿Cómo se puede programar un listado bajo el precio del mercado con Blockly para visualizar?

- Guía de uso de la plataforma de cuantificación de moneda digital websocket (más detalles después de la actualización de la función Dial)

- Obtener el parámetro 3 en la interfaz de robotdetail es una tontería

- ¿Cómo pueden los recién llegados pasar por el camino, cómo capturar las tendencias y hacer que las ganancias duren?

- Guía para principiantes del análisis de series temporales

- Prueba posterior de una estrategia de pronóstico para el S&P500 en Python con pandas

Sé siempre cuándo dejar de fumar 6 estrategias de salida - FMZ Interacciones Públicas

- ¿Cuáles son los diferentes tipos de fondos cuánticos?

- Prueba de una estrategia de pares de inversión de la media intradiaria entre SPY e IWM

- Prueba de un cruce de promedio móvil en Python con pandas