Estrategia de ruptura de medias móviles sobre Bandas de Bollinger

1

Follow

1802

Followers

Resumen

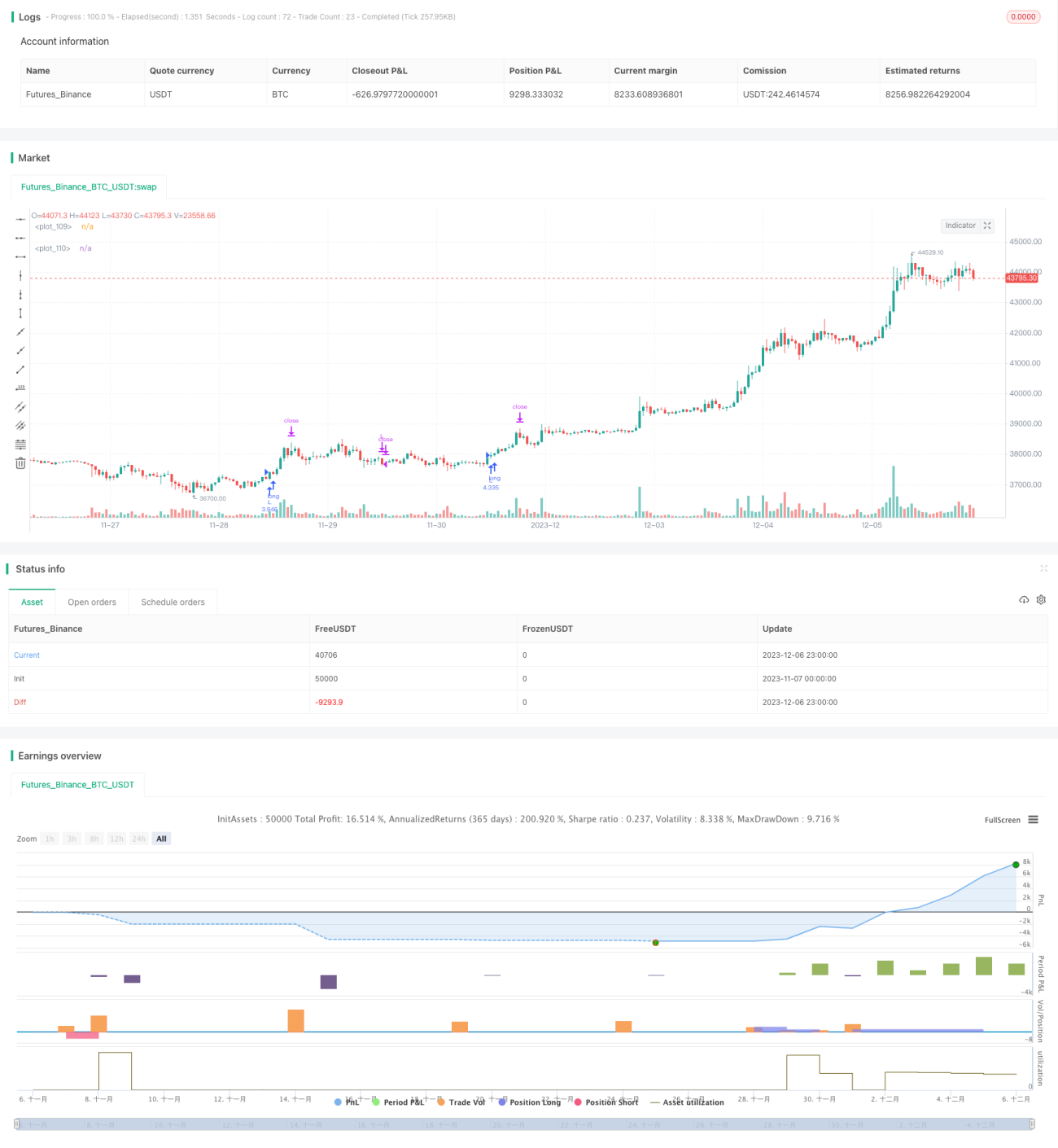

Esta estrategia combina el indicador de media móvil, el indicador de Bandas de Bollinger y el indicador UT Bot Alerts para implementar una estrategia simple de ruptura. Cuando el precio supera la banda superior de Bollinger, se toma una posición larga; cuando el precio supera la banda inferior de Bollinger, se toma una posición corta.

Principio de la estrategia

- Se utiliza una EMA de 200 períodos como eje central para determinar la tendencia. El precio por encima de la EMA es alcista, y por debajo es bajista.

- El indicador UT Bot Alerts, combinado con el ATR, genera señales de compra y venta. Cuando el precio y la EMA rápida cruzan la banda superior de Bollinger, se genera una señal de compra; cuando cruzan la banda inferior, se genera una señal de venta.

- El indicador de stop loss basado en ATR se utiliza para establecer el nivel de stop loss. La distancia del stop loss es 1,5 veces el valor del ATR.

- Tras la entrada, se establecen el stop loss, el take profit y el trailing stop hasta el precio de entrada según la relación riesgo-recompensa.

Análisis de ventajas

- El uso de las Bandas de Bollinger para determinar el momento adecuado para tomar posiciones largas o cortas puede aumentar la probabilidad de obtener ganancias.

- El indicador UT Bot Alerts puede generar señales bastante precisas.

- El uso de la relación riesgo-recompensa para establecer stop loss y take profit permite controlar el riesgo de manera efectiva.

Análisis de riesgos

- Las Bandas de Bollinger tienden a generar señales falsas en mercados laterales o de rango.

- El ATR tiene rezago, por lo que la distancia del stop loss puede ser demasiado amplia al inicio de una tendencia.

- Una relación riesgo-recompensa mal ajustada puede resultar en una estrategia demasiado agresiva o demasiado conservadora.

Direcciones de optimización

- Se puede probar reemplazar el indicador UT Bot Alerts por otros indicadores.

- Se puede optimizar el período y el multiplicador del ATR para que la distancia del stop loss sea más adecuada.

- Se pueden probar diferentes relaciones riesgo-recompensa para encontrar los parámetros óptimos.

Conclusión

Esta estrategia integra las ventajas de múltiples indicadores y tiene una gran utilidad práctica. Mediante la optimización de parámetros, puede convertirse en un sistema de ruptura estable y fiable. Sin embargo, también se debe prestar atención a los riesgos derivados de fallos en los indicadores o parámetros inadecuados.

Source

Pine

/*backtest

start: 2023-11-07 00:00:00

end: 2023-12-07 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

//@version=5

//Developed by StrategiesForEveryone

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1