Stratégie de point de rupture à moyenne mobile double des contrats à terme sur crypto-monnaie (enseignement)

Auteur:Je suis désolée., Créé à partir de: 2022-04-08 11:46:22, mis à jour à partir de: 2022-04-08 11:58:28Stratégie de point de rupture à moyenne mobile double des contrats à terme sur crypto-monnaie (enseignement)

Cet article explique la conception d'une stratégie de tendance simple, uniquement à partir du niveau de conception de la stratégie, pour aider les débutants à apprendre à concevoir une stratégie simple et à comprendre le processus d'exécution du programme de stratégie.

Conception de la stratégie

Lorsque l'on utilise les deux indicateurs EMA et que les deux moyennes mobiles ont un point de rupture, les points de rupture sont utilisés comme signal pour ouvrir des positions longues et courtes (ou inverser), pour concevoir une cible fixe pour le profit de l'écart de fermeture des positions.

Code de stratégie

/*backtest

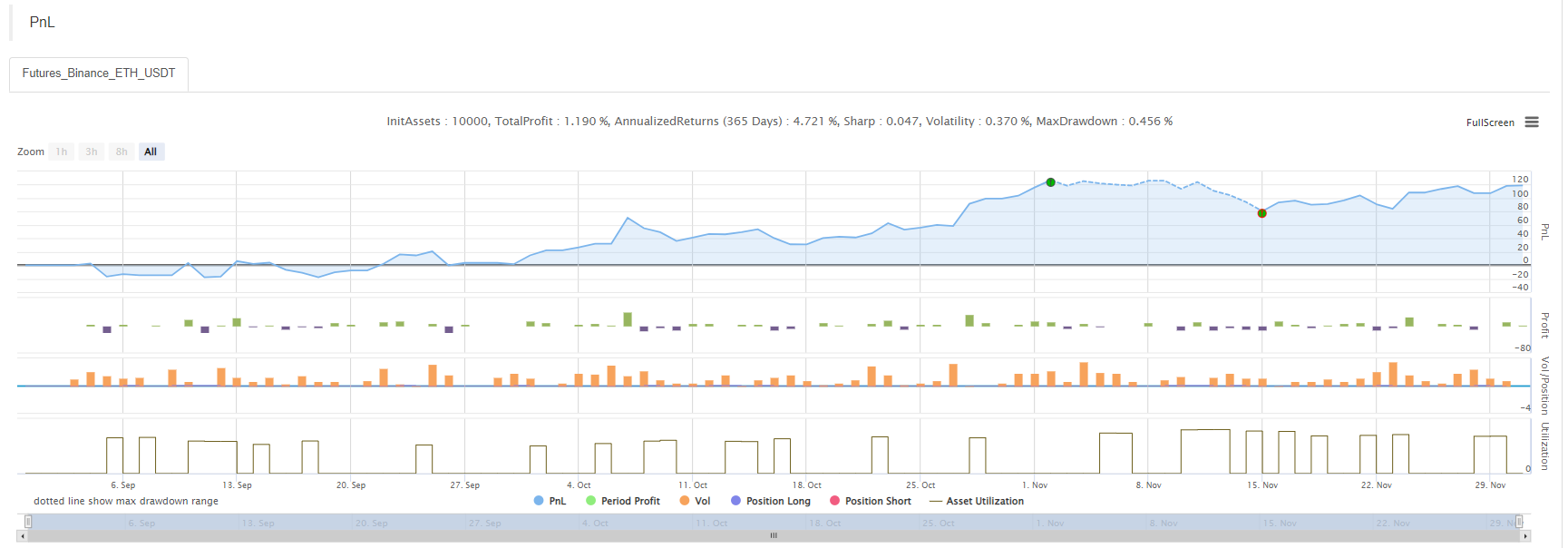

start: 2021-09-01 00:00:00

end: 2021-12-02 00:00:00

period: 1h

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"ETH_USDT"}]

*/

// above /**/ inside these are the default backtest settings; the backtest page can be reset by the related controls on the backtest page

var LONG = 1 // mark of holding long positions; enum constant

var SHORT = -1 // mark of holding short positions; enum constant

var IDLE = 0 // mark of not holding no position; enum constant

// obtain the positions with a specified direction; positions indicates position data; direction indicates the direction of the positions to be obtained

function getPosition(positions, direction) {

var ret = {Price : 0, Amount : 0, Type : ""} // define a structure when holding no position

// traverse positions, among which find the positions conforming to the direction

if (pos.Type == direction) {

ret = pos

}

})

// return the positions found

return ret

}

// cancel all pending orders of the current trading pair and contract

function cancellAll() {

// infinite loop, detect without stop, until break is triggered

while (true) {

// obtain the pending orders data of the current trading pair and contract, namely orders

var orders = _C(exchange.GetOrders)

if (orders.length == 0) {

// when orders is a null array, namely orders.length == 0, execute "break" statement to break the while loop

break

} else {

// traverse all the current pending orders, and cancel them one by one

for (var i = 0 ; i < orders.length ; i++) {

// the function to cancel a specified order, canceling the order with an ID of:orders[i].Id

exchange.CancelOrder(orders[i].Id, orders[i])

Sleep(500)

}

}

Sleep(500)

}

}

// function of closing position, which executes close position, according to the passed tradeFunc and direction

function cover(tradeFunc, direction) {

var mapDirection = {"closebuy": PD_LONG, "closesell": PD_SHORT}

var positions = _C(exchange.GetPosition) // obtain the position data of the current trading pair and contract

var pos = getPosition(positions, mapDirection[direction]) // find the position information of the specified close position direction

// when position volume is over 0 (only when there is a position, you can operate close position)

if (pos.Amount > 0) {

// cancel all possibly existing pending orders

cancellAll()

// set trading direction

exchange.SetDirection(direction)

// execute close position tradefunc

if (tradeFunc(-1, pos.Amount)) {

// if ordering successfully, return true

return true

} else {

// if the ordering fails, return false

return false

}

}

// no position returns true

return true

}

// strategy main function

function main() {

// used to switch to OKEX V5 simulated bot

if (okexSimulate) {

exchange.IO("simulate", true) // switch to OKEX V5 simulated bot to test

Log("switch to OKEX V5 simulated bot")

}

// set contract code; set ct to swap, namely set the current operated contract to a perpetual contract

exchange.SetContractType(ct)

// the initial status is no position

var state = IDLE

// the initial position price is 0

var holdPrice = 0

// innitialize the timestamp for comparison, to compare whether the current K-line BAR changes

var preTime = 0

// strategy main loop

while (true) {

// obtain the K-line data of the current trading pair and contract

var r = _C(exchange.GetRecords)

// obtain the K-line length, namely 1

var l = r.length

// judge the K-line length of 1, which has to be longer than the indicator period (if the length is less than the indicator period, the indicator function cannot calculate the effective indicatorr data); if not, the loop will be restarted

if (l < Math.max(ema1Period, ema2Period)) {

// wait 1000 miliseconds, namely 1 second, to avoid rotating too fast

Sleep(1000)

// ignore the code after "if" at the moment, and restart the while loop

continue

}

// calculate EMA indicator data

var ema1 = TA.EMA(r, ema1Period)

var ema2 = TA.EMA(r, ema2Period)

// plot

$.PlotRecords(r, 'K-line') // draw K-line chart

// when the timestamp of the last BAR changes, namely when the new K-line BAR is generated

if(preTime !== r[l - 1].Time){

// before the new K-line BAR is generated, it is the last update of the last BAR

$.PlotLine('ema1', ema1[l - 2], r[l - 2].Time)

$.PlotLine('ema2', ema2[l - 2], r[l - 2].Time)

// draw the EMA lines of the new BAR, namely the EMA indicator data on the current last BAR

$.PlotLine('ema1', ema1[l - 1], r[l - 1].Time)

$.PlotLine('ema2', ema2[l - 1], r[l - 1].Time)

// update the timestamp for comparison

preTime = r[l - 1].Time

} else {

// at the moment when there is no new BAR generated, just update the EMA indicator data of the last BAR in the chart

$.PlotLine('ema1', ema1[l - 1], r[l - 1].Time)

$.PlotLine('ema2', ema2[l - 1], r[l - 1].Time)

}

// condition of open long position, breakpoint

var up = (ema1[l - 2] > ema1[l - 3] && ema1[l - 4] > ema1[l - 3]) && (ema2[l - 2] > ema2[l - 3] && ema2[l - 4] > ema2[l - 3])

// condition of open short position, breakpoint

var down = (ema1[l - 2] < ema1[l - 3] && ema1[l - 4] < ema1[l - 3]) && (ema2[l - 2] < ema2[l - 3] && ema2[l - 4] < ema2[l - 3])

// when the condition of open long position is triggered and currently short positions are held, or when the condition of open long position is triggered but there is no position

if (up && (state == SHORT || state == IDLE)) {

// if holding short, close first

if (state == SHORT && cover(exchange.Buy, "closesell")) {

// after close positions, mark the status of no position

state = IDLE

// reset the position price to 0

holdPrice = 0

// mark on the chart

$.PlotFlag(r[l - 1].Time, 'coverShort', 'CS')

}

// after close positions, reverse to open long

exchange.SetDirection("buy")

if (exchange.Buy(-1, amount)) {

// mark the current status

state = LONG

// record the current price

holdPrice = r[l - 1].Close

$.PlotFlag(r[l - 1].Time, 'openLong', 'L')

}

} else if (down && (state == LONG || state == IDLE)) {

// similar to the judge of up condition

if (state == LONG && cover(exchange.Sell, "closebuy")) {

state = IDLE

holdPrice = 0

$.PlotFlag(r[l - 1].Time, 'coverLong', 'CL')

}

exchange.SetDirection("sell")

if (exchange.Sell(-1, amount)) {

state = SHORT

holdPrice = r[l - 1].Close

$.PlotFlag(r[l - 1].Time, 'openShort', 'S')

}

}

// stop profit

if (state == LONG && r[l - 1].Close - holdPrice > profitTarget && cover(exchange.Sell, "closebuy")) {

state = IDLE

holdPrice = 0

$.PlotFlag(r[l - 1].Time, 'coverLong', 'CL')

} else if (state == SHORT && holdPrice - r[l - 1].Close > profitTarget && cover(exchange.Buy, "closesell")) {

state = IDLE

holdPrice = 0

$.PlotFlag(r[l - 1].Time, 'coverShort', 'CS')

}

// display the time on the status bar

LogStatus(_D())

Sleep(500)

}

}

Le code source de la stratégie:https://www.fmz.com/strategy/333269

La stratégie n'est qu'un enseignement de conception de programme, alors s'il vous plaît ne l'utilisez pas dans un bot.

Plus de

- Réaliser un robot de supervision d'ordre simple de Cryptocurrency Spot

- Une plateforme de paiement basée sur FMZ

- Contrats de crypto-monnaie Robot simple de supervision des ordres

- Vous voulez obtenir le temps correspondant lorsque vous utilisez getdepth

- Ignoré, résolu

- Le problème de la valeur

- Exemple de conception de stratégie dYdX

- Exploration initiale de l'application de Python Crawler sur FMZ

Crawling Contenu de l'annonce de Binance - Définition de la stratégie de couverture Recherche et exemple d'ordres en attente au comptant et à terme

- Situation récente et fonctionnement recommandé de la stratégie de taux de financement

- Stratégie des moyennes mobiles doubles multi-symbole de crypto-monnaie (enseignement)

- Réalisation de l'indicateur Fisher en JavaScript et de la planification sur FMZ

- Le gérant

- 2021 Cryptocurrency TAQ Review & Stratégie manquée la plus simple d'augmentation de 10 fois

- Stratégie ART multi-symbole sur les contrats à terme de crypto-monnaie (enseignement)

- Mise à niveau! Stratégie de Martingale sur les contrats à terme de crypto-monnaie

- La fonction Getrecords n'arrive pas à récupérer le schéma de K en secondes

- Conception d'un système de gestion synchrone basé sur les ordres FMZ (2)

- Les données de volume retournées par Getticker sont incorrectes.

- Conception d'un système de gestion synchrone basé sur les ordres FMZ (1)