Stratégie de stop suiveur sur retournement de tendance

Aperçu

Cette stratégie est basée sur un indicateur de retournement de tendance, combiné à un mécanisme de stop-loss suiveur de tendance. Elle permet de suivre la tendance sur les marchés en tendance et de réduire les pertes sur les marchés en consolidation.

Principe de la stratégie

La stratégie utilise la moyenne mobile de Hull comme indicateur principal de tendance. Lorsque le prix franchit la moyenne de Hull à la hausse, on prend une position longue ; lorsqu'il la franchit à la baisse, on prend une position courte. Parallèlement, la moyenne de McGinley est utilisée pour confirmer la tendance.

Après l'ouverture d'une position, si le prix s'inverse, c'est-à-dire lorsque la moyenne mobile de Hull indique un croisement, la logique de changement de tendance s'exécute et la position actuelle est fermée.

La stratégie intègre également un mécanisme de stop-loss suiveur. Après l'ouverture d'une position, le niveau de stop-loss dynamique est calculé en fonction de l'ATR. Au fur et à mesure de l'évolution des prix, la ligne de stop-loss s'ajuste dynamiquement pour assurer un stop-loss suiveur des bénéfices.

Avantages de la stratégie

- Utilisation de la moyenne mobile de Hull pour détecter les points de retournement de tendance, avec une grande sensibilité aux signaux de cassure.

- Combinaison avec la moyenne de McGinley pour confirmer la tendance, ce qui permet de filtrer certaines fausses cassures.

- Mécanisme de stop-loss suiveur dynamique, ajustant l'amplitude du stop-loss en fonction de la volatilité du marché, contrôlant efficacement les pertes.

- Réaction rapide aux retournements de tendance en surveillant la moyenne mobile de Hull, évitant ainsi l'aggravation des pertes.

- Possibilité de tester facilement différentes combinaisons de paramètres pour trouver les paramètres optimaux.

Risques et solutions

-

Le stop-loss peut être déclenché en période de marché agité.

- Augmenter l'amplitude du stop-loss ou ajouter une zone tampon.

-

Sur les marchés très volatils, le stop-loss suiveur peut ne pas suivre les mouvements de prix assez rapidement.

- Réduire la période de lissage pour que le stop-loss s'adapte plus rapidement.

-

Les fausses cassures peuvent entraîner des pertes inutiles.

- Ajouter d'autres indicateurs de confirmation pour éviter les faux signaux.

-

Des paramètres inappropriés peuvent dégrader les performances de la stratégie.

- Effectuer des backtests sur différentes périodes de marché pour déterminer les paramètres optimaux.

Pistes d'optimisation

- Ajouter d'autres indicateurs de confirmation (figures de chandeliers, bandes de Bollinger, RSI, etc.) pour améliorer la qualité des signaux.

- Optimiser les paramètres en fonction des différents instruments et périodes pour trouver la meilleure combinaison.

- Envisager des méthodes d'apprentissage automatique pour une optimisation adaptative des paramètres.

- Optimiser l'algorithme de stop-loss afin de réduire les stop-loss inutiles tout en garantissant la protection.

- Combiner une gestion de capital optimisée pour la stratégie de dimensionnement des positions.

- Envisager l'ajout d'un mécanisme de take-profit automatique.

Conclusion

Dans l'ensemble, cette stratégie est une stratégie de suivi de tendance relativement robuste. Contrairement à un stop-loss fixe, elle utilise un stop-loss dynamique qui s'adapte à la volatilité du marché, réduisant ainsi la probabilité de se faire prendre par un stop-loss. Par ailleurs, l'introduction de la moyenne mobile de Hull et de la logique de changement de tendance permet une réaction rapide aux retournements de tendance. Cependant, cette stratégie présente certains risques, comme les stop-loss en période de consolidation ou les fausses cassures. En optimisant davantage les paramètres des indicateurs, l'algorithme de stop-loss et la gestion des positions, la stratégie peut obtenir des performances plus stables sur différents marchés.

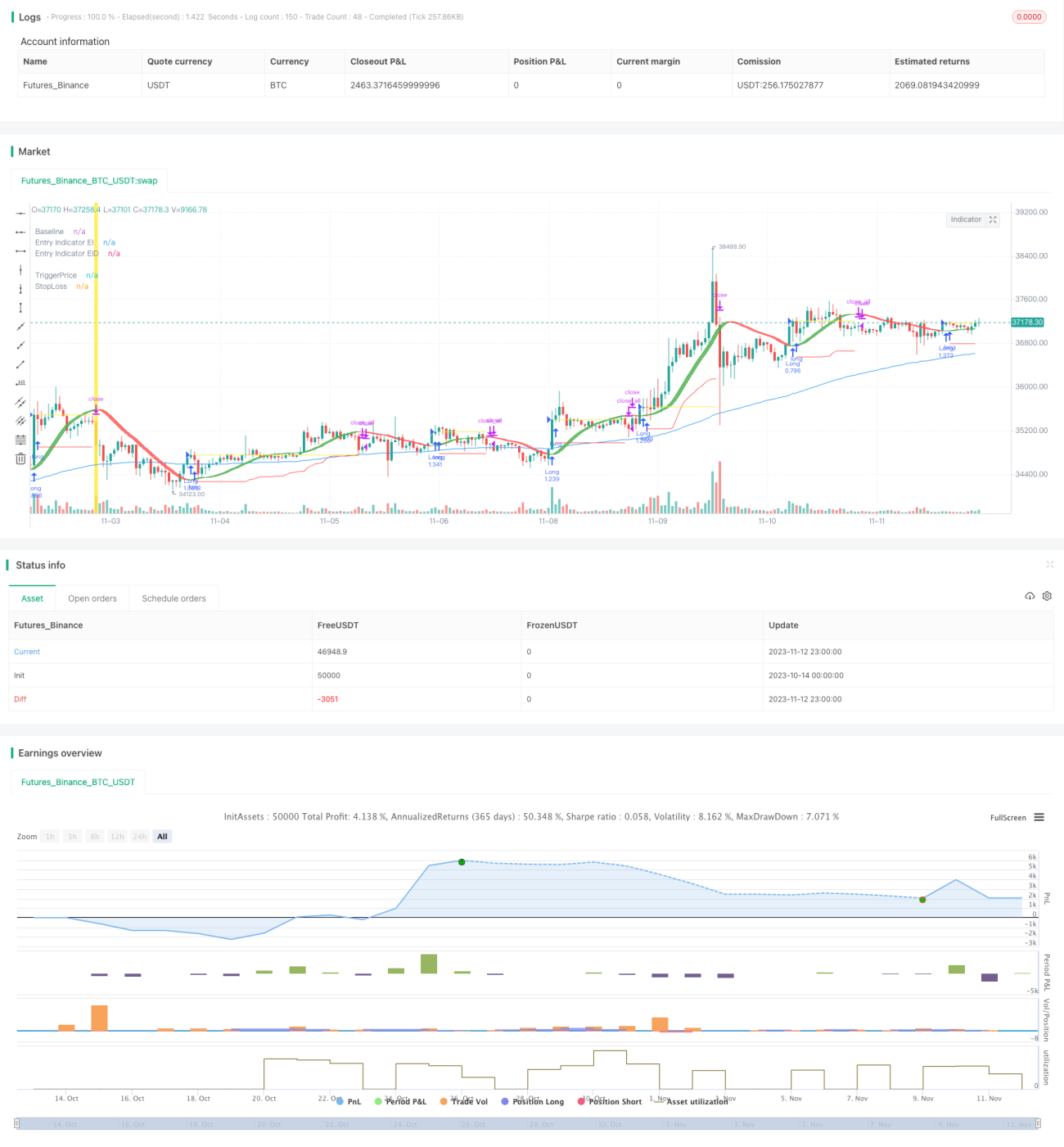

/*backtest

start: 2023-10-14 00:00:00

end: 2023-11-13 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// © Milleman

//@version=4

strategy("MilleMachine", overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, initial_capital=10000, commission_type=strategy.commission.percent, commission_value=0.06)

- 1