概要

本戦略は反転戦略とボリンジャーバンドの強気戦略を組み合わせ、複合的な取引シグナルを生成することで、トレンド追跡と反転キャッチの二重機能を実現します。

戦略の原理

反転部分

丘晨の著書『私はいかにして先物市場で3倍の利益を上げたか』(第183ページ)の反転戦略ロジックに基づき、終値が前日終値を2日連続で上回り、かつ9日ストキャスティクスのスローラインが50未満の場合に買い、終値が前日終値を2日連続で下回り、かつ9日ストキャスティクスのファストラインが50超の場合に売りとします。

強気部分

アレクサンダー・エルダー博士のボリンジャーバンド強気指標を使用します。13日指数平滑移動平均線で市場価値のコンセンサスを表し、買い強気指標は買い手が価格を価値コンセンサスより上に押し上げる能力を、売り強気指標は売り手が価格を価値コンセンサスより下に押し下げる能力を反映します。買い強気指標は当日高値から13日指数平滑移動平均線を引いた値、売り強気指標は当日安値から13日指数平滑移動平均線を引いた値として計算します。

本戦略では強気指標の閾値を0と設定し、強気指標が0を超えた場合に取引シグナルを発生させます。

複合シグナル

反転戦略と強気戦略の取引シグナルが一致した場合に、最終的な取引シグナルを生成します。買いシグナルは反転シグナルの買いと強気シグナルの買いの組み合わせ、売りシグナルは反転シグナルの売りと強気シグナルの売りの組み合わせです。

優位性分析

本戦略は複合型戦略であり、反転戦略とトレンド追跡戦略を同時に使用して取引シグナルを形成するため、リバウンドのキャッチとトレンドの追跡という両方の利点を併せ持ちます。

反転部分はギャップ後の反転機会を捉えることができます。強気部分はトレンドが存在する場合にのみポジションを取ることを保証します。両者を組み合わせることで、偽のブレイクアウトを効果的にフィルタリングし、ポジションが拘束されるリスクを回避できます。

パラメータ最適化の柔軟性が高く、異なる銘柄や期間に合わせて調整し、最適なパラメータ組み合わせを見つけることが可能です。

リスク分析

反転戦略と強気戦略が同時に買いまたは売りを示す確率は低く、シグナル発生頻度が低い可能性があり、一定程度のシグナル不足リスクがあります。

反転部分は、相場の調整を反転と誤認し、早期にポジションを構築する可能性があります。強気部分は一部の反転機会を逃す可能性があります。両者を組み合わせることで、これらのリスクをある程度緩和できます。後段では��세判断モジュールの導入を検討し、さらなる最適化を図ることができます。

最適化の方向性

- より多くのパラメータ組み合わせを試し、最適なパラメータを見つける

- トレンド判断モジュールを追加し、明確なトレンドがない場合にポジションを繰り返し構築するのを回避する

- ストップロス戦略を導入し、1回の損失を抑制することを検討する

まとめ

本戦略はトレンド追跡と反転取引の特性を併せ持ち、複合型戦略の中でも優れたものと言えます。パラメータ最適化により、良好な安定した収益が期待できます。同時に、シグナル不足や誤認のリスクに注意する必要があり、後段ではトレンド判断やストップロスモジュールの導入などによる最適化を行い、戦略の実戦性能をより一層高めることが可能です。

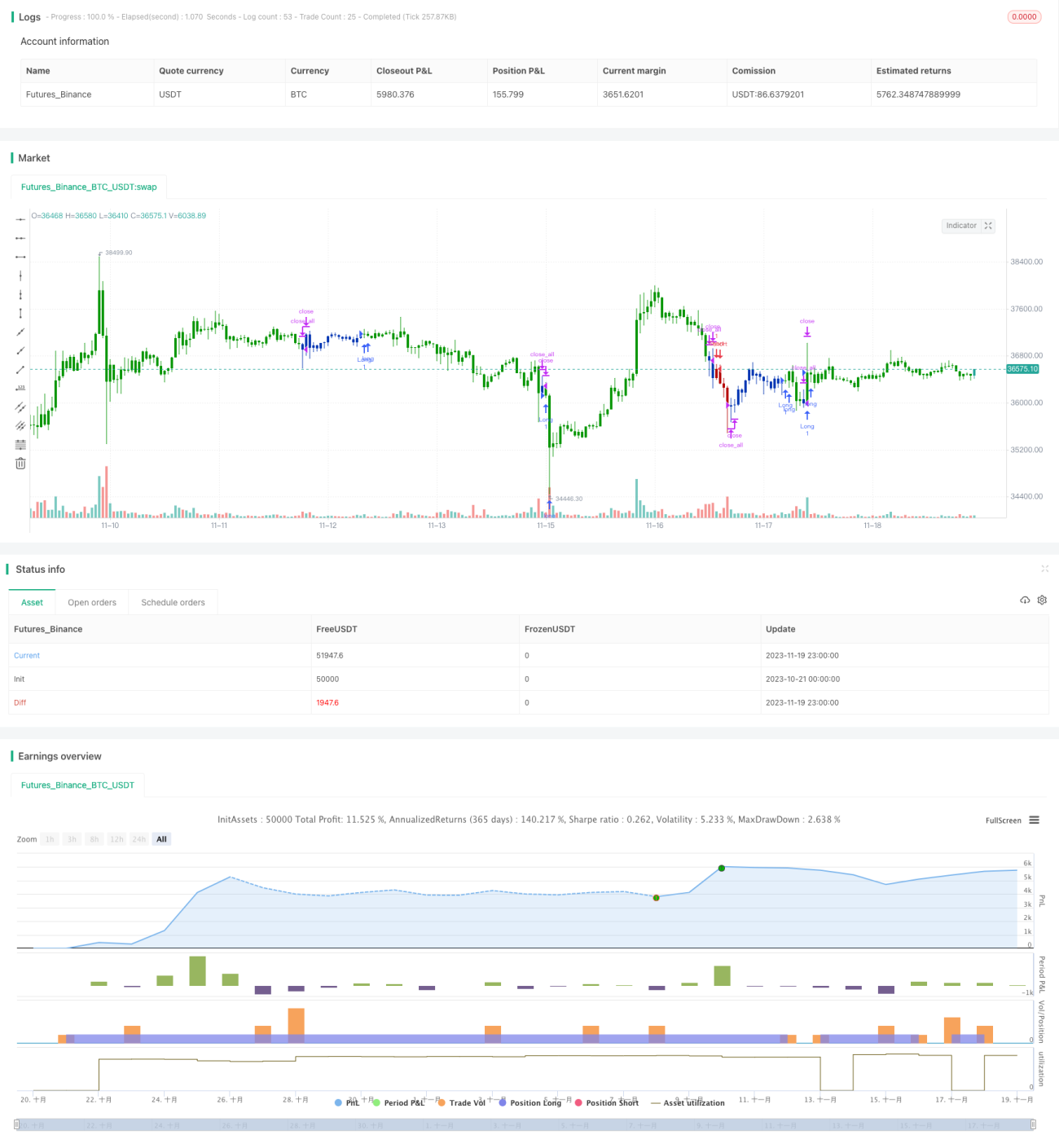

/*backtest

start: 2023-10-21 00:00:00

end: 2023-11-20 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 15/06/2020

// This is combo strategies for get a cumulative signal. - 1