Strategi Pengesanan Trend Pelbagai Penunjuk

Gambaran Keseluruhan

Strategi ini menggabungkan tiga penunjuk sumber terbuka untuk menentukan arah aliran dalam pelbagai jangka masa, dan menetapkan stop loss serta take profit untuk mengunci keuntungan. Secara khusus, strategi ini menggunakan penunjuk AK MACD BB untuk menentukan arah aliran jangka pendek, penunjuk SSL untuk menapis isyarat palsu, dan akhirnya menggabungkan penunjuk volum VSF untuk menilai kekuatan sebenar belian dan jualan, seterusnya menentukan masa masuk. Pada masa yang sama, strategi ini telah menetapkan titik stop loss dan take profit untuk mengunci keuntungan, yang dapat mengurangkan risiko kerugian bagi setiap dagangan secara ketara.

Prinsip Strategi

- Penunjuk AK MACD BB

Penunjuk ini menggunakan Bollinger Bands pada penunjuk MACD. Apabila garis MACD menembusi jalur atas Bollinger Bands, ia menghasilkan isyarat beli; apabila menembusi jalur bawah, ia menghasilkan isyarat jual.

- Penunjuk SSL

Penunjuk SSL menentukan sama ada harga menembusi purata bergerak, dan mengesan isyarat pengujian semula. Apabila harga menembusi purata bergerak ke atas dan penunjuk SSL berwarna biru, ia adalah arah aliran menaik; apabila harga menembusi purata bergerak ke bawah dan penunjuk SSL berwarna merah, ia adalah arah aliran menurun, dan isyarat dagangan dikeluarkan.

- Penunjuk VSF

Penunjuk VSF menilai kekuatan pihak beli dan jual. Strategi hanya mengeluarkan isyarat apabila kekuatan pihak beli atau jual melebihi 50%, untuk mengelakkan penembusan palsu.

- Stop Loss dan Take Profit

Strategi ini mengandungi 4 peringkat take profit progresif, dengan jarak keuntungan dari 1.5 kali hingga 3 kali. Pada masa yang sama, stop loss tetap 2% ditetapkan untuk mengawal kerugian maksimum bagi setiap dagangan secara berkesan.

Analisis Kelebihan

- Gabungan pelbagai penunjuk, ketepatan tinggi

Dengan menggunakan penunjuk berbeza untuk menentukan arah aliran dalam pelbagai jangka masa, isyarat palsu dapat ditapis, dan ketepatan penentuan lebih tinggi.

- Take profit dan stop loss automatik, risiko terkawal

Strategi ini dilengkapi dengan tetapan take profit dan stop loss, yang dapat mengawal kerugian setiap dagangan sekitar 2%, mengelakkan kerugian besar.

- Data ujian semula yang cemerlang

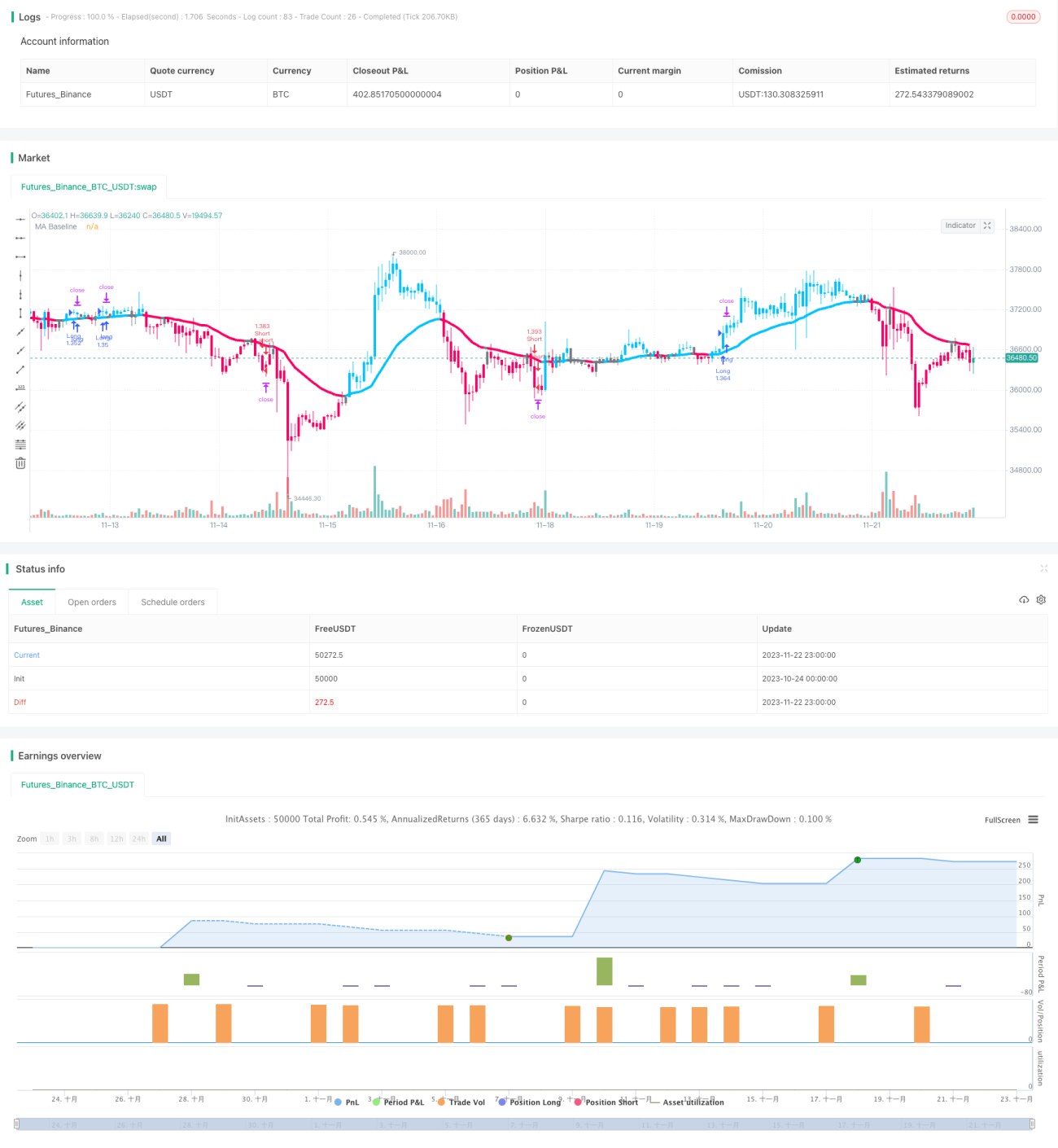

Menurut ujian semula penerbit, daripada 100 dagangan, dagangan yang menguntungkan mencapai 74%, dengan jumlah keuntungan 427%.

Analisis Risiko dan Langkah Penanggulangan

- Risiko turun naik pasaran yang melampau

Semasa pasaran berayun dalam julat besar, mungkin berlaku beberapa kerugian kecil. Pada masa ini, had stop loss tetap boleh dilaraskan, atau dagangan boleh dihentikan.

- Risiko sekatan beli dan jual

Pada masa ini, strategi membolehkan kedua-dua beli dan jual. Jika hanya terhad kepada beli atau jual sahaja, peluang untuk mendapat keuntungan akan berkurang separuh.

- Risiko sesi dagangan

Strategi menggunakan data 5 minit untuk membuat keputusan. Jika hanya terdapat beberapa jam data dalam satu hari dagangan, sampel tidak mencukupi, dan isyarat mungkin tidak boleh dipercayai.

Hala Tuju Pengoptimuman Strategi

- Mengoptimumkan parameter stop loss dan take profit

Pelbagai tahap stop loss dan take profit boleh diuji untuk mencari parameter optimum. Stop loss yang terlalu kecil tidak dapat mengawal risiko dengan berkesan, manakala stop loss yang terlalu besar mungkin menyebabkan kehilangan keuntungan yang lebih besar.

- Menambah pelarasan kedudukan automatik

Trailing stop atau moving stop boleh ditetapkan untuk mengunci keuntungan. Atau, tambah kedudukan berdasarkan syarat tertentu untuk mendapatkan lebih banyak keuntungan.

- Menggabungkan penunjuk lain

Gabungan penunjuk yang berbeza boleh diuji untuk menentukan kombinasi yang paling berkesan. Lebih banyak penunjuk juga boleh ditambah untuk pengesahan silang.

- Pengoptimuman parameter

Ujian semula boleh dilakukan dengan parameter berbeza untuk mencari hala tuju pengoptimuman parameter. Dalam strategi ini, menukar parameter Bollinger Bands atau purata bergerak mungkin menghasilkan hasil yang lebih baik.

Kesimpulan

Strategi ini mengintegrasikan pelbagai penunjuk untuk menentukan arah aliran, menetapkan take profit dan stop loss automatik, mampu memperoleh keuntungan dalam arah aliran yang kukuh dan mengawal kerugian setiap dagangan dalam julat yang kecil. Berdasarkan data ujian semula penerbit, kadar keuntungan dan peratusan keuntungan adalah sangat ideal. Dengan pengoptimuman tertentu, kestabilan dan kemampuan keuntungan strategi ini berpotensi untuk ditingkatkan lagi.

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © myn

//@version=5

strategy('Strategy Myth-Busting #7 - MACDBB+SSL+VSF - [MYN]', max_bars_back=5000, overlay=true, pyramiding=0, initial_capital=1000, currency='USD', default_qty_type=strategy.percent_of_equity, default_qty_value=1.0, commission_value=0.075, use_bar_magnifier = false)

/////////////////////////////////////

//* Put your strategy logic below *//

/////////////////////////////////////

//nwVqTuPe6yo- 1