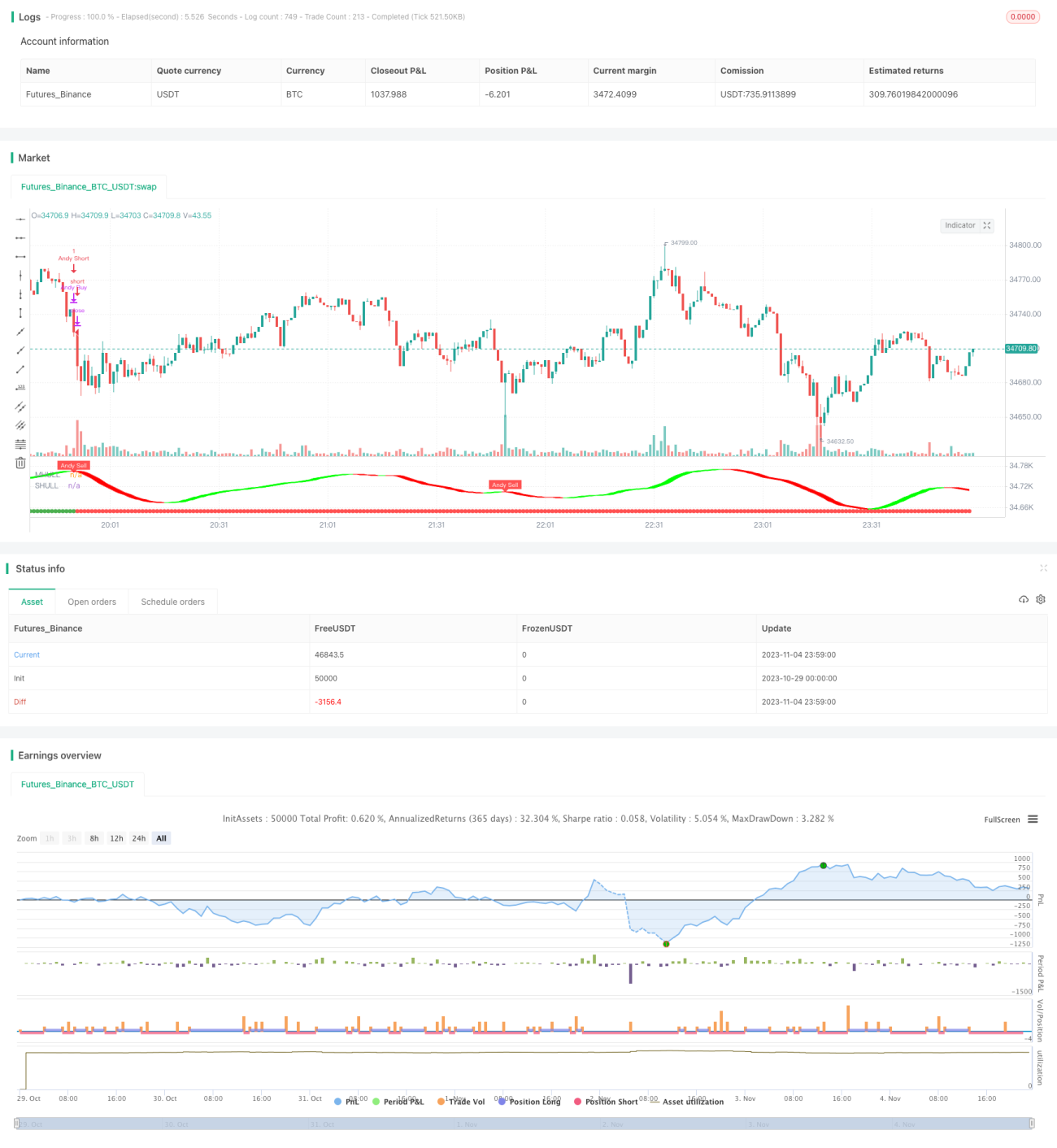

Estratégia de Rompimento de Momentum com Seguimento de Tendência

Visão Geral

Esta estratégia combina múltiplos indicadores técnicos para identificar a direção da tendência e rastreia os momentos de rompimento de momentum, buscando obter retornos excessivos.

Princípio da Estratégia

-

Utiliza o canal Donchian para determinar a direção geral da tendência. Quando o preço rompe esse canal, confirma-se uma mudança na tendência.

-

A Média Móvel de Hull auxilia na identificação da direção da tendência. Este indicador é sensível às mudanças de preço, permitindo detectar reversões de tendência com antecedência.

-

O sistema de semi-órbita gera sinais de compra e venda. Esse sistema, baseado em canais de preço e no Average True Range, evita falsos rompimentos.

-

Quando o canal Donchian, o indicador Hull e o sistema de semi-órbita emitem sinais simultaneamente, identifica-se um forte rompimento de momentum na tendência, momento de entrar no mercado.

-

Condição de saída: quando os indicadores acima emitem sinais contrários, determina-se uma reversão da tendência e a posição é fechada imediatamente com stop loss.

Análise de Vantagens

-

Combinação de múltiplos indicadores, maior capacidade de julgamento. O canal Donchian define a tendência geral, enquanto o Hull e a semi-órbita capturam os detalhes, identificando pontos precisos de reversão.

-

Participação em rompimentos de momentum, buscando retornos excessivos. A entrada ocorre apenas em fortes rompimentos, evitando ficar preso em mercados laterais.

-

Stop loss rigoroso, protegendo o capital. Assim que os indicadores emitem sinais contrários, a posição é encerrada para evitar perdas maiores.

-

Parâmetros ajustáveis, adaptáveis a diversos mercados. É possível ajustar comprimento do canal, faixa de volatilidade, etc., otimizando para diferentes períodos.

-

Fácil compreensão e implementação, acessível a iniciantes. A combinação de indicadores e condições é simples e clara, fácil de programar.

Análise de Riscos

-

Perda de oportunidades no início da tendência. A entrada é tardia, não capturando os ganhos iniciais.

-

Perdas por rompimento fracassado e reversão. Após a entrada, pode ocorrer falha no rompimento e reversão, gerando perdas.

-

Sinais falsos dos indicadores. Parâmetros inadequados podem levar a erros de julgamento.

-

Número limitado de negociações. A entrada ocorre apenas em rompimentos claros, resultando em poucas operações anuais.

Direções de Otimização

-

Otimizar combinações de parâmetros. Testar diferentes parâmetros para encontrar a melhor configuração.

-

Adicionar condição de trailing stop para evitar stops prematuros e perder oportunidades de tendência.

-

Incluir outros indicadores de filtro, como MACD, KDJ, para auxiliar no julgamento e reduzir sinais falsos.

-

Otimizar períodos de negociação. Parâmetros podem ser ajustados para diferentes faixas de tempo.

-

Aumentar a eficiência do uso de capital. Utilizar alavancagem, investimento periódico, etc., para melhorar a utilização do capital.

Resumo

Esta estratégia combina múltiplos indicadores para identificar o momento de rompimento de momentum em uma tendência, buscando retornos excessivos ao acompanhar a tendência já formada. Um mecanismo rigoroso de stop loss controla os riscos, e parâmetros flexíveis permitem adaptação a diferentes ambientes de mercado. Embora a frequência de negociação seja baixa, cada operação visa alto retorno. Através da otimização de parâmetros e introdução de indicadores auxiliares, esta estratégia pode ser continuamente aprimorada.

- 1