کریپٹوکرنسی اسپاٹ ملٹی علامت ڈبل چلتی اوسط حکمت عملی (تعلیم)

مصنف:نینا باداس, تخلیق: 2022-04-07 16:14:35, تازہ کاری: 2022-04-08 09:13:58کریپٹوکرنسی اسپاٹ ملٹی علامت ڈبل چلتی اوسط حکمت عملی (تعلیم)

فورموں میں ہمارے صارفین کی درخواست پر کہ وہ ڈیزائن ریفرنس کے طور پر ایک کثیر علامت ڈبل چلتی اوسط حکمت عملی رکھنے کی امید کرتے ہیں ، آج کے شیئرنگ میں ایک کثیر علامت ڈبل چلتی اوسط حکمت عملی نافذ کی جائے گی۔ حکمت عملی کو سمجھنے اور سیکھنے میں آپ کی سہولت کے لئے حکمت عملی کوڈ میں تبصرے لکھے جائیں گے ، جس سے پروگراماتی اور مقداری تجارت کے مزید نئے طلباء کو حکمت عملی کے ساتھ تیزی سے شروعات کرنے میں مدد ملے گی۔

حکمت عملی کا سوچنا

دوہری حرکت پذیر اوسط حکمت عملی کا منطق بہت آسان ہے ، یعنی دو حرکت پذیر اوسط۔ ایک چھوٹی مدت (فاسٹ لائن) کے ساتھ ایک حرکت پذیر اوسط اور ایک بڑی مدت (سست لائن) کے ساتھ ایک حرکت پذیر اوسط۔ جب دونوں لائنوں میں سنہری کراس ہوتا ہے (فاسٹ لائن اوپر سے سست لائن کو نیچے سے عبور کرتی ہے) ، تو طویل خریدیں ، اور جب دونوں لائنوں میں مردہ کراس ہوتا ہے (فاسٹ لائن نیچے سے سست لائن کو اوپر سے عبور کرتی ہے) ، تو مختصر فروخت کریں۔ حرکت پذیر اوسط کے لئے ، ہم ای ایم اے کا استعمال کرتے ہیں۔

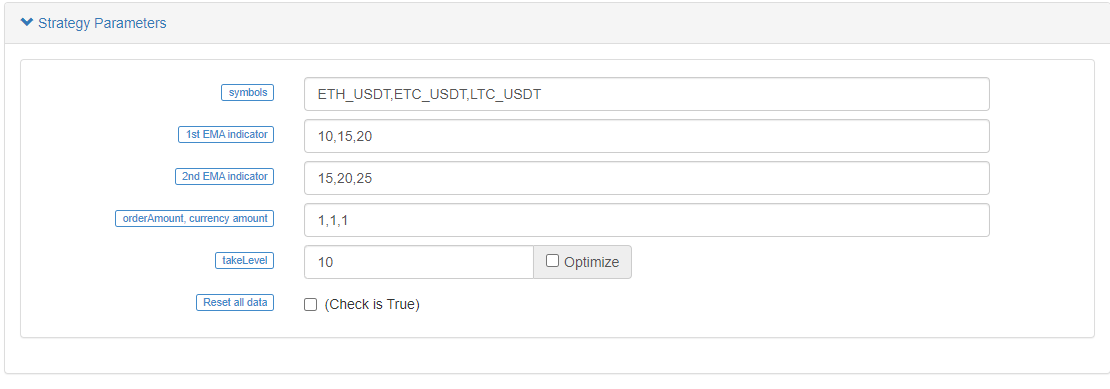

یہ صرف یہ ہے کہ حکمت عملی کو متعدد علامتوں کے لئے ڈیزائن کرنے کی ضرورت ہے ، لہذا مختلف علامتوں کے پیرامیٹرز مختلف ہوسکتے ہیں (مختلف علامتیں مختلف حرکت پذیر اوسط پیرامیٹرز استعمال کرتی ہیں) ، لہذا پیرامیٹرز کو

پیرامیٹرز کو ایک تار کی شکل میں ڈیزائن کیا گیا ہے ، ہر پیرامیٹر کو کوما سے تقسیم کیا جاتا ہے۔ جب حکمت عملی چلنا شروع ہوتی ہے تو ان تاروں کو تجزیہ کیا جاتا ہے ، جو ہر علامت (ٹریڈنگ جوڑی) کے لئے عملدرآمد منطق سے مماثل ہوگی۔ حکمت عملی پولنگ مارکیٹ کی قیمتوں کا تعین کرتی ہے ، تمام علامتوں ، ٹریڈنگ کی شرائط کو متحرک کرنے اور چارٹ پرنٹ کرتی ہے۔ تمام علامتوں کو ایک بار پولنگ کرنے کے بعد ، اعداد و شمار کو جمع کیا جاتا ہے اور ٹیبل کی معلومات اسٹیٹس بار پر ظاہر ہوتی ہیں۔

یہ حکمت عملی انتہائی آسان ڈیزائن کی گئی ہے اور ابتدائیوں کے لئے بہت موزوں ہے۔ یہ مجموعی طور پر صرف 200+ لائنوں پر مشتمل ہے۔

حکمت عملی کا کوڈ

// function effect: to cancel all pending orders of the current trading pair

function cancelAll(e) {

while (true) {

var orders = _C(e.GetOrders)

if (orders.length == 0) {

break

} else {

for (var i = 0 ; i < orders.length ; i++) {

e.CancelOrder(orders[i].Id, orders[i])

Sleep(500)

}

}

Sleep(500)

}

}

// function effect: to calculate the real-time profit and loss

function getProfit(account, initAccount, lastPrices) {

// account indicates the current account information; initAccount is the initial account information; lastPrices is the the latest prices of all current symbols

var sum = 0

_.each(account, function(val, key) {

// traverse the current total assets, and calculate asset currency (except USDT) difference and amount difference

if (key != "USDT" && typeof(initAccount[key]) == "number" && lastPrices[key + "_USDT"]) {

sum += (account[key] - initAccount[key]) * lastPrices[key + "_USDT"]

}

})

// return the asset profit and loss calculated by the current price

return account["USDT"] - initAccount["USDT"] + sum

}

// function effect: to generate chart configuration

function createChartConfig(symbol, ema1Period, ema2Period) {

// symbol indicates trading pair; ema1Period indicates the first EMA period; ema2Period indicates the second EMA period

var chart = {

__isStock: true,

extension: {

layout: 'single',

height: 600,

},

title : { text : symbol},

xAxis: { type: 'datetime'},

series : [

{

type: 'candlestick', // K-line date series

name: symbol,

id: symbol,

data: []

}, {

type: 'line', // EMA data series

name: symbol + ',EMA1:' + ema1Period,

data: [],

}, {

type: 'line', // EMA data series

name: symbol + ',EMA2:' + ema2Period,

data: []

}

]

}

return chart

}

function main() {

// reset all data

if (isReset) {

_G(null) // vacuum all persistently recorded data

LogReset(1) // vacuum all logs

LogProfitReset() // vacuum all profit logs

LogVacuum() // release the resource occupied by the bot database

Log("reset all data", "#FF0000") // print information

}

// parse parameters

var arrSymbols = symbols.split(",") // use comma to split the trading symbol strings

var arrEma1Periods = ema1Periods.split(",") // split the string of the first EMA parameter

var arrEma2Periods = ema2Periods.split(",") // split the string of the second EMA parameter

var arrAmounts = orderAmounts.split(",") // split the order amount of each symbol

var account = {} // the variable used to record the current asset information

var initAccount = {} // the variable used to record the initial asset information

var currTradeMsg = {} // the variable used to record whether the current BAR is executed

var lastPrices = {} // the variable used to record the latest price of the monitored symbol

var lastBarTime = {} // the variable used to record the time of the latest BAR, to judge the BAR update during plotting

var arrChartConfig = [] // the variable used to record the chart configuration information, to plot

if (_G("currTradeMsg")) { // for example, when restart, recover currTradeMsg data

currTradeMsg = _G("currTradeMsg")

Log("recover GetRecords", currTradeMsg)

}

// initialize account

_.each(arrSymbols, function(symbol, index) {

exchange.SetCurrency(symbol)

var arrCurrencyName = symbol.split("_")

var baseCurrency = arrCurrencyName[0]

var quoteCurrency = arrCurrencyName[1]

if (quoteCurrency != "USDT") {

throw "only support quoteCurrency: USDT"

}

if (!account[baseCurrency] || !account[quoteCurrency]) {

cancelAll(exchange)

var acc = _C(exchange.GetAccount)

account[baseCurrency] = acc.Stocks

account[quoteCurrency] = acc.Balance

}

// initialize the related data of chart

lastBarTime[symbol] = 0

arrChartConfig.push(createChartConfig(symbol, arrEma1Periods[index], arrEma2Periods[index]))

})

if (_G("initAccount")) {

initAccount = _G("initAccount")

Log("recover initial account information", initAccount)

} else {

// use the current asset information to initialize initAccount (variable)

_.each(account, function(val, key) {

initAccount[key] = val

})

}

Log("account:", account, "initAccount:", initAccount) // print asset information

// initialize the chart objects

var chart = Chart(arrChartConfig)

// reset chart

chart.reset()

// strategy logic of the main loop

while (true) {

// traverse all symbols, and execute the dual moving average logic one by one

_.each(arrSymbols, function(symbol, index) {

exchange.SetCurrency(symbol) // switch the trading pair to the trading pair recorded by by symbol string

var arrCurrencyName = symbol.split("_") // split trading pairs by "_"

var baseCurrency = arrCurrencyName[0] // string of base currency

var quoteCurrency = arrCurrencyName[1] // string of quote currency

// according to index, obtain the EMA paramater of the current trading pair

var ema1Period = parseFloat(arrEma1Periods[index])

var ema2Period = parseFloat(arrEma2Periods[index])

var amount = parseFloat(arrAmounts[index])

// obtain the K-line data of the current trading pair

var r = exchange.GetRecords()

if (!r || r.length < Math.max(ema1Period, ema2Period)) { // when the length of K-line is not long enough, return directly

Sleep(1000)

return

}

var currBarTime = r[r.length - 1].Time // record the current BAR timestamp

lastPrices[symbol] = r[r.length - 1].Close // record the current latest price

var ema1 = TA.EMA(r, ema1Period) // calculate EMA indicator

var ema2 = TA.EMA(r, ema2Period) // calculate EMA indicator

if (ema1.length < 3 || ema2.length < 3) { // when the length of EMA indicator array is too short, return derectly

Sleep(1000)

return

}

var ema1Last2 = ema1[ema1.length - 2] // EMA on the second last BAR

var ema1Last3 = ema1[ema1.length - 3] // EMA on the third last BAR

var ema2Last2 = ema2[ema2.length - 2]

var ema2Last3 = ema2[ema2.length - 3]

// write the chart data

var klineIndex = index + 2 * index

// traverse k-line data

for (var i = 0 ; i < r.length ; i++) {

if (r[i].Time == lastBarTime[symbol]) { // plot; update the current BAR and its indicator

// update

chart.add(klineIndex, [r[i].Time, r[i].Open, r[i].High, r[i].Low, r[i].Close], -1)

chart.add(klineIndex + 1, [r[i].Time, ema1[i]], -1)

chart.add(klineIndex + 2, [r[i].Time, ema2[i]], -1)

} else if (r[i].Time > lastBarTime[symbol]) { // plot; add BAR and its indicator

// add

lastBarTime[symbol] = r[i].Time // update the timestamp

chart.add(klineIndex, [r[i].Time, r[i].Open, r[i].High, r[i].Low, r[i].Close])

chart.add(klineIndex + 1, [r[i].Time, ema1[i]])

chart.add(klineIndex + 2, [r[i].Time, ema2[i]])

}

}

if (ema1Last3 < ema2Last3 && ema1Last2 > ema2Last2 && currTradeMsg[symbol] != currBarTime) {

// golden cross

var depth = exchange.GetDepth() // obtain the depth data of the current order book

var price = depth.Asks[Math.min(takeLevel, depth.Asks.length)].Price // select the 10th level price; taker

if (depth && price * amount <= account[quoteCurrency]) { // obtain that the depth data is normal, and the assets are enough to place an order

exchange.Buy(price, amount, ema1Last3, ema2Last3, ema1Last2, ema2Last2) // maker; buy

cancelAll(exchange) // cancel all pending orders

var acc = _C(exchange.GetAccount) // obtain the account asset information

if (acc.Stocks != account[baseCurrency]) { // detect the account assets changed

account[baseCurrency] = acc.Stocks // update assets

account[quoteCurrency] = acc.Balance // update assets

currTradeMsg[symbol] = currBarTime // record the current BAR has been executed

_G("currTradeMsg", currTradeMsg) // persistently record

var profit = getProfit(account, initAccount, lastPrices) // calculate profit

if (profit) {

LogProfit(profit, account, initAccount) // print profit

}

}

}

} else if (ema1Last3 > ema2Last3 && ema1Last2 < ema2Last2 && currTradeMsg[symbol] != currBarTime) {

// death cross

var depth = exchange.GetDepth()

var price = depth.Bids[Math.min(takeLevel, depth.Bids.length)].Price

if (depth && amount <= account[baseCurrency]) {

exchange.Sell(price, amount, ema1Last3, ema2Last3, ema1Last2, ema2Last2)

cancelAll(exchange)

var acc = _C(exchange.GetAccount)

if (acc.Stocks != account[baseCurrency]) {

account[baseCurrency] = acc.Stocks

account[quoteCurrency] = acc.Balance

currTradeMsg[symbol] = currBarTime

_G("currTradeMsg", currTradeMsg)

var profit = getProfit(account, initAccount, lastPrices)

if (profit) {

LogProfit(profit, account, initAccount)

}

}

}

}

Sleep(1000)

})

// variables in the table of status bar

var tbl = {

type : "table",

title : "account information",

cols : [],

rows : []

}

// write the data in the table structure of status bar

tbl.cols.push("--")

tbl.rows.push(["initial"])

tbl.rows.push(["current"])

_.each(account, function(val, key) {

if (typeof(initAccount[key]) == "number") {

tbl.cols.push(key)

tbl.rows[0].push(initAccount[key]) // initial

tbl.rows[1].push(val) // current

}

})

// display the status bar table

LogStatus(_D(), "\n", "profit:", getProfit(account, initAccount, lastPrices), "\n", "`" + JSON.stringify(tbl) + "`")

}

}

حکمت عملی کا بیک ٹیسٹ

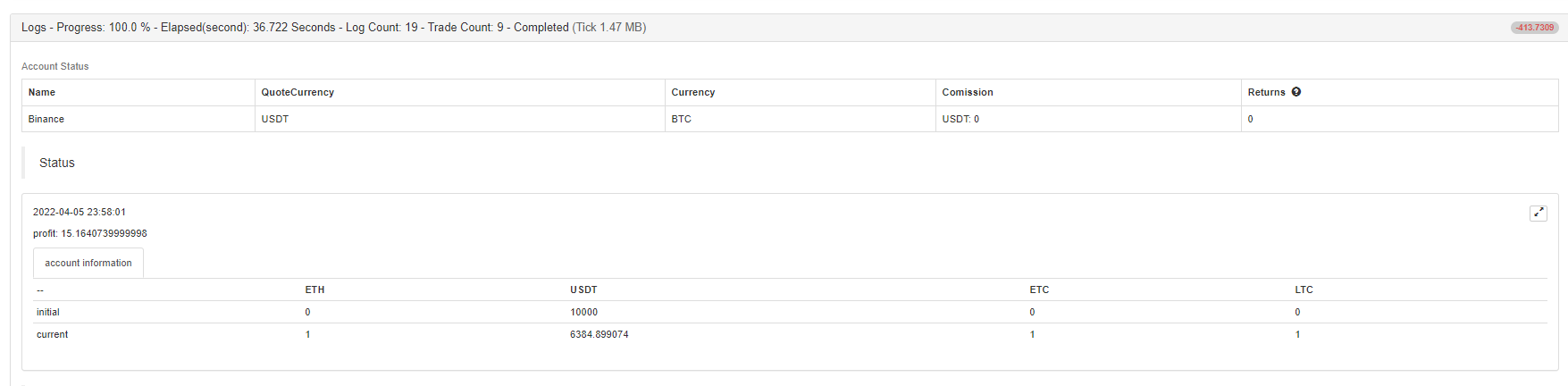

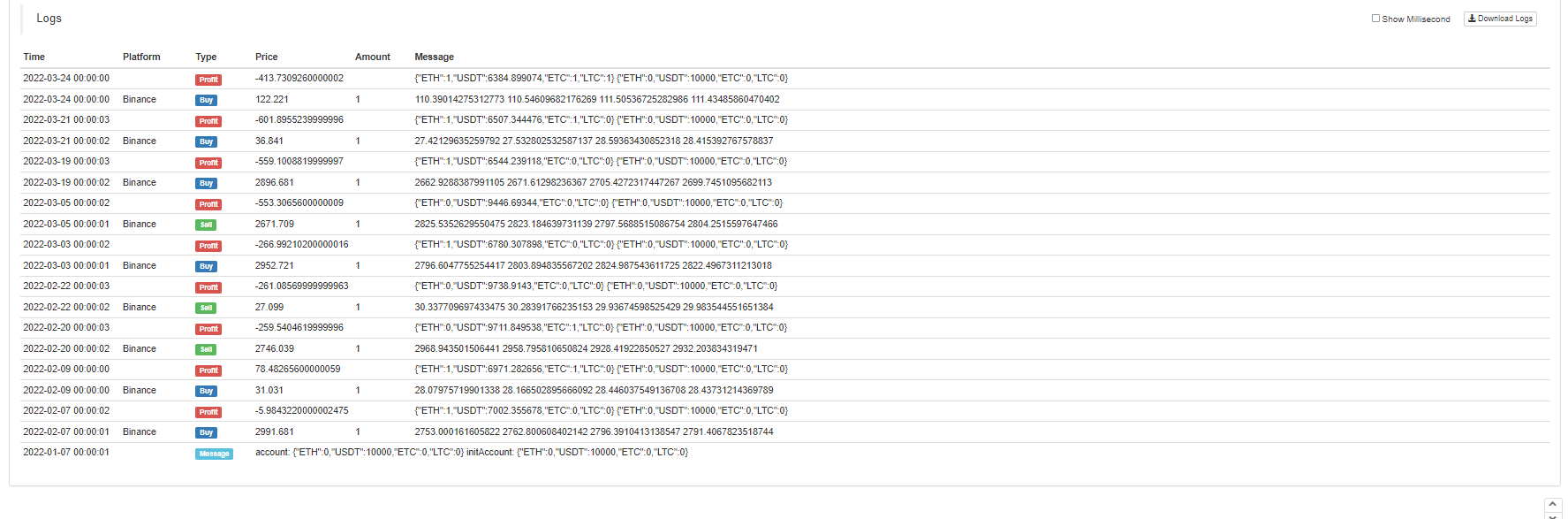

آپ دیکھ سکتے ہیں کہ ETH، LTC اور ETC سب نے گولڈن کراس اور موت کے کراس کے ٹرگرز کے مطابق تجارت کی.

آپ ٹیسٹ کرنے کے لئے مشابہ روبوٹ پر بھی انتظار کر سکتے ہیں.

حکمت عملی کا ماخذ کوڈ:https://www.fmz.com/strategy/333783

یہ حکمت عملی صرف بیک ٹیسٹ اور حکمت عملی ڈیزائن سیکھنے کے لئے استعمال کیا جاتا ہے، لہذا احتیاط کے ساتھ ایک بوٹ میں استعمال کریں.

- ایف ایم زیڈ پر مبنی ادائیگی پلیٹ فارم

- کریپٹوکرنسی معاہدہ سادہ آرڈر سپروائزنگ بوٹ

- جب آپ getdepth کا استعمال کرتے ہیں تو آپ کو وقت کی حد حاصل کرنے کی ضرورت ہے

- نظر انداز، حل

- قیمت کا سوال

- dYdX حکمت عملی ڈیزائن مثال

- ایف ایم زیڈ

کراولنگ بائننس اعلان مواد پر پائیتھون کرالر کا اطلاق کرنے کی ابتدائی تلاش - ہیج حکمت عملی ڈیزائن ریسرچ & زیر التواء اسپاٹ اور فیوچر آرڈرز کی مثال

- حالیہ صورت حال اور فنڈنگ ریٹ کی حکمت عملی کا تجویز کردہ آپریشن

- کریپٹوکرنسی فیوچر کی دوہری حرکت پذیر اوسط وقفے کی حکمت عملی (تعلیم)

- جاوا اسکرپٹ میں فشر اشارے کا احساس اور ایف ایم زیڈ پر پلاٹنگ

- نگہبان

- 2021 کریپٹوکرنسی ٹی اے کیو جائزہ اور 10 گنا اضافے کی سادہ ترین گمشدہ حکمت عملی

- کریپٹوکرنسی فیوچر ملٹی علامت ART حکمت عملی (تعلیم)

- اپ گریڈ کریں! کریپٹوکرنسی فیوچر مارٹنگیل حکمت عملی

- گیٹ ریکارڈز فنکشن سیکنڈ میں K سٹرنگ گراف حاصل نہیں کر سکا

- FMZ پر مبنی آرڈر سنکرون مینجمنٹ سسٹم ڈیزائن (2)

- گیٹیکر نے جو حجم واپس کیا ہے وہ غلط ہے۔

- ایف ایم زیڈ پر مبنی آرڈر سنکرون مینجمنٹ سسٹم ڈیزائن (1)

- ایک کثیر چارٹ پلاٹنگ لائبریری ڈیزائن کریں