دوہری الٹ رجحان کی پیروی کی حکمت عملی

خلاصہ

یہ ایک رجحان کی پیروی کرنے والی حکمت عملی ہے جو دوہرے الٹ جانے والے سگنلز کو یکجا کرتی ہے۔ اس میں 123 الٹ جانے کی حکمت عملی اور کارکردگی انڈیکس حکمت عملی کو شامل کیا گیا ہے، تاکہ قیمت میں الٹ جانے والے نکات کا سراغ لگایا جا سکے اور زیادہ قابل اعتماد رجحان کا تعین کیا جا سکے۔

حکمت عملی کا اصول

یہ حکمت عملی دو ذیلی حکمت عملیوں پر مشتمل ہے:

-

123 الٹ جانے کی حکمت عملی

14 دن کی K لائن کا استعمال کرتے ہوئے الٹ جانے کے سگنل کا تعین کیا جاتا ہے۔ تفصیلی اصول یہ ہیں:

- تیزی کا سگنل: پچھلے دو دنوں میں بند ہونے والی قیمت میں کمی، موجودہ K لائن کی بند ہونے والی قیمت پچھلے دن کی بند ہونے والی قیمت سے زیادہ، 9 دن کا Stochastic Slow 50 سے کم

- مندی کا سگنل: پچھلے دو دنوں میں بند ہونے والی قیمت میں اضافہ، موجودہ K لائن کی بند ہونے والی قیمت پچھلے دن کی بند ہونے والی قیمت سے کم، 9 دن کا Stochastic Fast 50 سے زیادہ

-

کارکردگی انڈیکس حکمت عملی

پچھلے 14 دنوں کے منافع/نقصان کی شرح کو ایک اشاریہ کے طور پر شمار کیا جاتا ہے۔ اصول درج ذیل ہیں:

- کارکردگی انڈیکس > (0) ہو تو تیزی کا سگنل پیدا ہوتا ہے

- کارکردگی انڈیکس < (0) ہو تو مندی کا سگنل پیدا ہوتا ہے

حتمی سگنل دونوں سگنلز کا مجموعہ ہے۔ یعنی ایک ہی سمت میں تیزی یا مندی کے سگنلز کی ضرورت ہوتی ہے تاکہ اصل خرید و فروخت کا عمل شروع ہو سکے۔

اس طرح کچھ شور کو فلٹر کیا جا سکتا ہے، جس سے سگنلز زیادہ قابل اعتماد ہو جاتے ہیں۔

حکمت عملی کے فوائد

اس دوہرے الٹ جانے والے نظام کے درج ذیل فوائد ہیں:

- دوہرے عوامل کو ملا کر فیصلہ کرنا، سگنلز زیادہ قابل اعتماد ہوتے ہیں

- مارکیٹ کے شور کو مؤثر طریقے سے فلٹر کرنے اور جعلی سگنلز سے بچنے کی صلاحیت

- 123 کی شکل کلاسک اور عملی ہے، جس کا تعین اور دوبارہ پیش کرنا آسان ہے

- کارکردگی انڈیکس مستقبل کے رجحان کا تعین کر سکتا ہے

- پیرامیٹرز کا مجموعہ لچکدار ہے، جسے مزید بہتر بنایا جا سکتا ہے

حکمت عملی کے خطرات

اس حکمت عملی میں کچھ خطرات بھی ہیں:

- اچانک الٹ جانے والے رجحان کو پکڑنے میں ناکامی، رجحان کو مکمل طور پر گرفت میں نہیں لا سکتا

- دوہرے شرائط کے نتیجے میں سگنلز کم ہو جاتے ہیں، جس سے منافع کی صلاحیت متاثر ہو سکتی ہے

- ایک ہی سمت میں فیصلے کی ضرورت، جس کی وجہ سے انفرادی اسٹاک کی خاص اتار چڑھاؤ سے متاثر ہونے کا امکان

- پیرامیٹر کی ترتیب کے مسائل سگنل میں انحراف کا سبب بن سکتے ہیں

مندرجہ ذیل پہلوؤں پر بہتری لائی جا سکتی ہے:

- پیرامیٹرز کو ایڈجسٹ کرنا، جیسے K لائن کی لمبائی، Stochastic کا دورانیہ وغیرہ

- دوہرے سگنل کے فیصلے کی منطق کو بہتر بنانا

- مزید عوامل کو شامل کرنا، جیسے تجارتی حجم وغیرہ

- نقصان کو روکنے کا طریقہ کار شامل کرنا

خلاصہ

یہ حکمت عملی دوہرے الٹ جانے والے فیصلوں کو یکجا کرتی ہے، جو قیمت میں تبدیلی کے نکات کو مؤثر طریقے سے دریافت کر سکتی ہے۔ اگرچہ سگنل کے وقوع پذیر ہونے کا امکان کم ہو جاتا ہے، لیکن قابل اعتمادی زیادہ ہوتی ہے، اور یہ درمیانی اور طویل مدتی رجحان کو پکڑنے کے لیے موزوں ہے۔ پیرامیٹرز کی ایڈجسٹمنٹ اور کثیر عوامل کی اصلاح کے ذریعے حکمت عملی کے اثرات کو مزید بڑھایا جا سکتا ہے۔

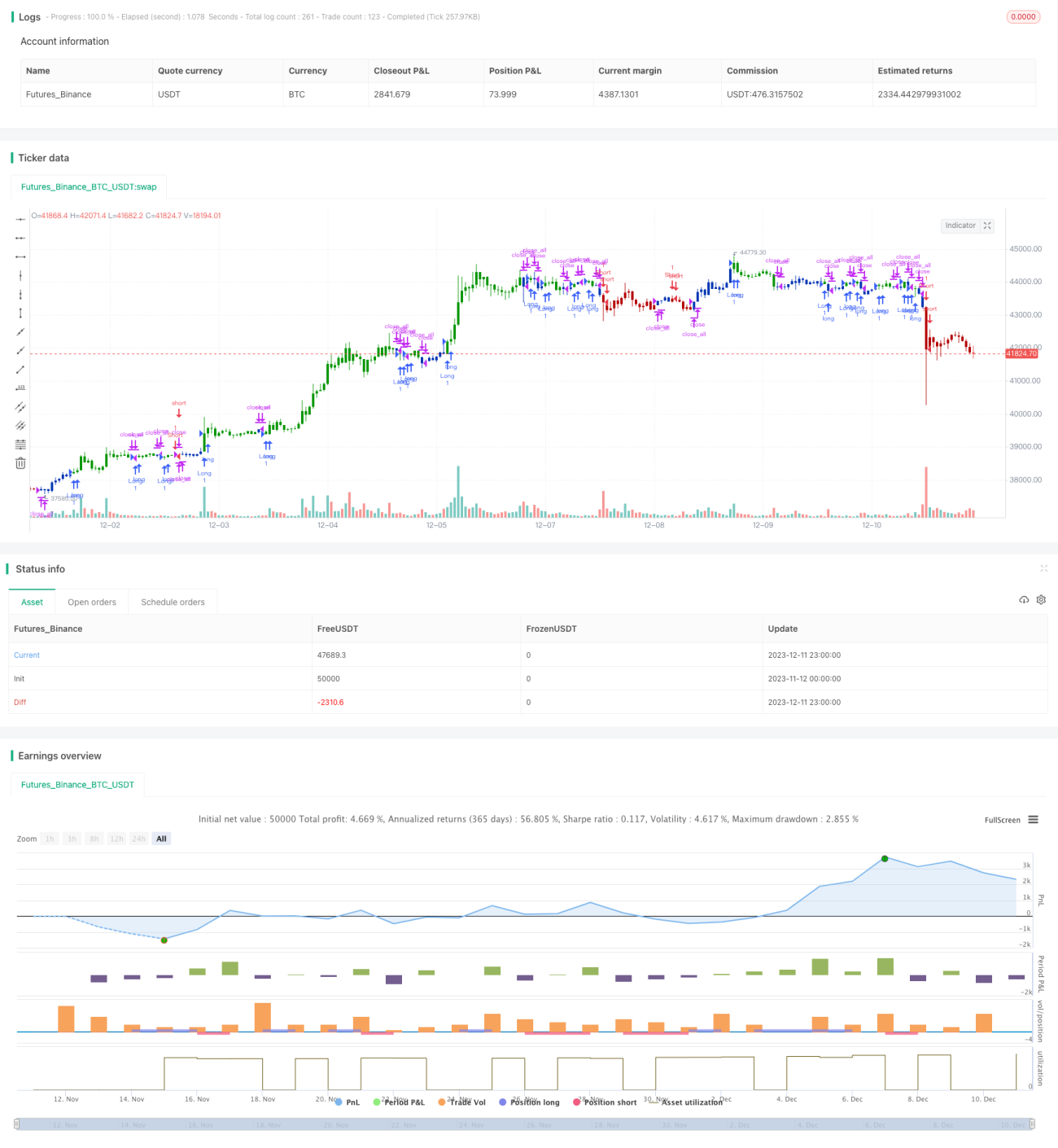

/*backtest

start: 2023-11-12 00:00:00

end: 2023-12-12 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 15/04/2021

// This is combo strategies for get a cumulative signal. - 1