Cryptocurrency Spot Multi-Symbol Dual Moving Average Strategy (Teaching)

Tác giả:Ninabadass, Tạo: 2022-04-07 16:14:35, Cập nhật: 2022-04-08 09:13:58Cryptocurrency Spot Multi-Symbol Dual Moving Average Strategy (Teaching)

Theo yêu cầu của người dùng của chúng tôi trong Diễn đàn rằng họ hy vọng có một chiến lược trung bình chuyển động kép đa biểu tượng như một tham chiếu thiết kế, một chiến lược trung bình chuyển động kép đa biểu tượng sẽ được thực hiện trong chia sẻ ngày hôm nay.

Suy nghĩ chiến lược

Lý thuyết của chiến lược đường trung bình động kép rất đơn giản, đó là hai đường trung bình động. Một đường trung bình động với một khoảng thời gian nhỏ (đường nhanh) và một đường trung bình động với một khoảng thời gian lớn (đường chậm). Khi hai đường có đường chéo vàng (đường nhanh vượt qua đường chậm từ dưới), mua dài, và khi hai đường có đường chéo chết (đường nhanh xuống vượt qua đường chậm từ trên), bán ngắn. Đối với đường trung bình di chuyển, Chúng tôi sử dụng EMA.

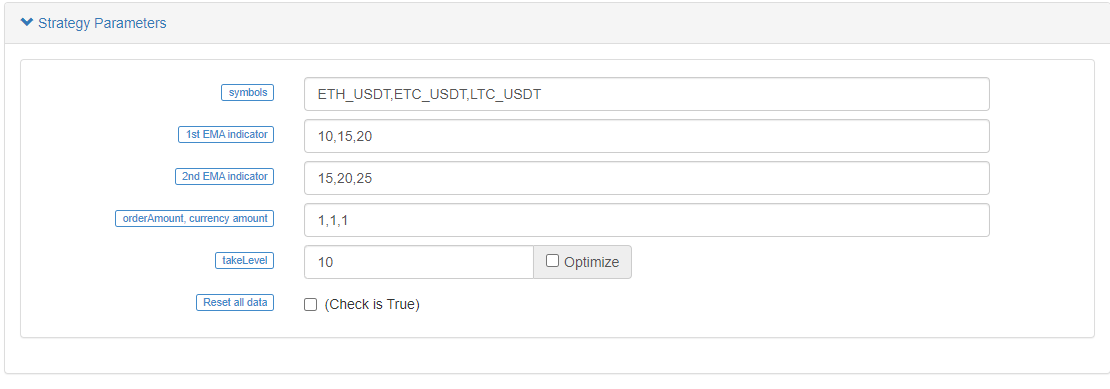

Chỉ là chiến lược cần được thiết kế cho nhiều biểu tượng, vì vậy các tham số của các biểu tượng khác nhau có thể khác nhau (các biểu tượng khác nhau sử dụng các tham số trung bình động khác nhau), vì vậy cần thiết để thiết kế các tham số trong một mảng

Các thông số được thiết kế dưới dạng chuỗi, với mỗi thông số được chia bằng dấu phẩy. Các chuỗi này được phân tích khi chiến lược bắt đầu chạy, sẽ được khớp với logic thực thi cho mỗi biểu tượng (cặp giao dịch).

Chiến lược được thiết kế rất đơn giản và rất phù hợp với người mới bắt đầu; nó chỉ có hơn 200 dòng tổng cộng.

Mã chiến lược

// function effect: to cancel all pending orders of the current trading pair

function cancelAll(e) {

while (true) {

var orders = _C(e.GetOrders)

if (orders.length == 0) {

break

} else {

for (var i = 0 ; i < orders.length ; i++) {

e.CancelOrder(orders[i].Id, orders[i])

Sleep(500)

}

}

Sleep(500)

}

}

// function effect: to calculate the real-time profit and loss

function getProfit(account, initAccount, lastPrices) {

// account indicates the current account information; initAccount is the initial account information; lastPrices is the the latest prices of all current symbols

var sum = 0

_.each(account, function(val, key) {

// traverse the current total assets, and calculate asset currency (except USDT) difference and amount difference

if (key != "USDT" && typeof(initAccount[key]) == "number" && lastPrices[key + "_USDT"]) {

sum += (account[key] - initAccount[key]) * lastPrices[key + "_USDT"]

}

})

// return the asset profit and loss calculated by the current price

return account["USDT"] - initAccount["USDT"] + sum

}

// function effect: to generate chart configuration

function createChartConfig(symbol, ema1Period, ema2Period) {

// symbol indicates trading pair; ema1Period indicates the first EMA period; ema2Period indicates the second EMA period

var chart = {

__isStock: true,

extension: {

layout: 'single',

height: 600,

},

title : { text : symbol},

xAxis: { type: 'datetime'},

series : [

{

type: 'candlestick', // K-line date series

name: symbol,

id: symbol,

data: []

}, {

type: 'line', // EMA data series

name: symbol + ',EMA1:' + ema1Period,

data: [],

}, {

type: 'line', // EMA data series

name: symbol + ',EMA2:' + ema2Period,

data: []

}

]

}

return chart

}

function main() {

// reset all data

if (isReset) {

_G(null) // vacuum all persistently recorded data

LogReset(1) // vacuum all logs

LogProfitReset() // vacuum all profit logs

LogVacuum() // release the resource occupied by the bot database

Log("reset all data", "#FF0000") // print information

}

// parse parameters

var arrSymbols = symbols.split(",") // use comma to split the trading symbol strings

var arrEma1Periods = ema1Periods.split(",") // split the string of the first EMA parameter

var arrEma2Periods = ema2Periods.split(",") // split the string of the second EMA parameter

var arrAmounts = orderAmounts.split(",") // split the order amount of each symbol

var account = {} // the variable used to record the current asset information

var initAccount = {} // the variable used to record the initial asset information

var currTradeMsg = {} // the variable used to record whether the current BAR is executed

var lastPrices = {} // the variable used to record the latest price of the monitored symbol

var lastBarTime = {} // the variable used to record the time of the latest BAR, to judge the BAR update during plotting

var arrChartConfig = [] // the variable used to record the chart configuration information, to plot

if (_G("currTradeMsg")) { // for example, when restart, recover currTradeMsg data

currTradeMsg = _G("currTradeMsg")

Log("recover GetRecords", currTradeMsg)

}

// initialize account

_.each(arrSymbols, function(symbol, index) {

exchange.SetCurrency(symbol)

var arrCurrencyName = symbol.split("_")

var baseCurrency = arrCurrencyName[0]

var quoteCurrency = arrCurrencyName[1]

if (quoteCurrency != "USDT") {

throw "only support quoteCurrency: USDT"

}

if (!account[baseCurrency] || !account[quoteCurrency]) {

cancelAll(exchange)

var acc = _C(exchange.GetAccount)

account[baseCurrency] = acc.Stocks

account[quoteCurrency] = acc.Balance

}

// initialize the related data of chart

lastBarTime[symbol] = 0

arrChartConfig.push(createChartConfig(symbol, arrEma1Periods[index], arrEma2Periods[index]))

})

if (_G("initAccount")) {

initAccount = _G("initAccount")

Log("recover initial account information", initAccount)

} else {

// use the current asset information to initialize initAccount (variable)

_.each(account, function(val, key) {

initAccount[key] = val

})

}

Log("account:", account, "initAccount:", initAccount) // print asset information

// initialize the chart objects

var chart = Chart(arrChartConfig)

// reset chart

chart.reset()

// strategy logic of the main loop

while (true) {

// traverse all symbols, and execute the dual moving average logic one by one

_.each(arrSymbols, function(symbol, index) {

exchange.SetCurrency(symbol) // switch the trading pair to the trading pair recorded by by symbol string

var arrCurrencyName = symbol.split("_") // split trading pairs by "_"

var baseCurrency = arrCurrencyName[0] // string of base currency

var quoteCurrency = arrCurrencyName[1] // string of quote currency

// according to index, obtain the EMA paramater of the current trading pair

var ema1Period = parseFloat(arrEma1Periods[index])

var ema2Period = parseFloat(arrEma2Periods[index])

var amount = parseFloat(arrAmounts[index])

// obtain the K-line data of the current trading pair

var r = exchange.GetRecords()

if (!r || r.length < Math.max(ema1Period, ema2Period)) { // when the length of K-line is not long enough, return directly

Sleep(1000)

return

}

var currBarTime = r[r.length - 1].Time // record the current BAR timestamp

lastPrices[symbol] = r[r.length - 1].Close // record the current latest price

var ema1 = TA.EMA(r, ema1Period) // calculate EMA indicator

var ema2 = TA.EMA(r, ema2Period) // calculate EMA indicator

if (ema1.length < 3 || ema2.length < 3) { // when the length of EMA indicator array is too short, return derectly

Sleep(1000)

return

}

var ema1Last2 = ema1[ema1.length - 2] // EMA on the second last BAR

var ema1Last3 = ema1[ema1.length - 3] // EMA on the third last BAR

var ema2Last2 = ema2[ema2.length - 2]

var ema2Last3 = ema2[ema2.length - 3]

// write the chart data

var klineIndex = index + 2 * index

// traverse k-line data

for (var i = 0 ; i < r.length ; i++) {

if (r[i].Time == lastBarTime[symbol]) { // plot; update the current BAR and its indicator

// update

chart.add(klineIndex, [r[i].Time, r[i].Open, r[i].High, r[i].Low, r[i].Close], -1)

chart.add(klineIndex + 1, [r[i].Time, ema1[i]], -1)

chart.add(klineIndex + 2, [r[i].Time, ema2[i]], -1)

} else if (r[i].Time > lastBarTime[symbol]) { // plot; add BAR and its indicator

// add

lastBarTime[symbol] = r[i].Time // update the timestamp

chart.add(klineIndex, [r[i].Time, r[i].Open, r[i].High, r[i].Low, r[i].Close])

chart.add(klineIndex + 1, [r[i].Time, ema1[i]])

chart.add(klineIndex + 2, [r[i].Time, ema2[i]])

}

}

if (ema1Last3 < ema2Last3 && ema1Last2 > ema2Last2 && currTradeMsg[symbol] != currBarTime) {

// golden cross

var depth = exchange.GetDepth() // obtain the depth data of the current order book

var price = depth.Asks[Math.min(takeLevel, depth.Asks.length)].Price // select the 10th level price; taker

if (depth && price * amount <= account[quoteCurrency]) { // obtain that the depth data is normal, and the assets are enough to place an order

exchange.Buy(price, amount, ema1Last3, ema2Last3, ema1Last2, ema2Last2) // maker; buy

cancelAll(exchange) // cancel all pending orders

var acc = _C(exchange.GetAccount) // obtain the account asset information

if (acc.Stocks != account[baseCurrency]) { // detect the account assets changed

account[baseCurrency] = acc.Stocks // update assets

account[quoteCurrency] = acc.Balance // update assets

currTradeMsg[symbol] = currBarTime // record the current BAR has been executed

_G("currTradeMsg", currTradeMsg) // persistently record

var profit = getProfit(account, initAccount, lastPrices) // calculate profit

if (profit) {

LogProfit(profit, account, initAccount) // print profit

}

}

}

} else if (ema1Last3 > ema2Last3 && ema1Last2 < ema2Last2 && currTradeMsg[symbol] != currBarTime) {

// death cross

var depth = exchange.GetDepth()

var price = depth.Bids[Math.min(takeLevel, depth.Bids.length)].Price

if (depth && amount <= account[baseCurrency]) {

exchange.Sell(price, amount, ema1Last3, ema2Last3, ema1Last2, ema2Last2)

cancelAll(exchange)

var acc = _C(exchange.GetAccount)

if (acc.Stocks != account[baseCurrency]) {

account[baseCurrency] = acc.Stocks

account[quoteCurrency] = acc.Balance

currTradeMsg[symbol] = currBarTime

_G("currTradeMsg", currTradeMsg)

var profit = getProfit(account, initAccount, lastPrices)

if (profit) {

LogProfit(profit, account, initAccount)

}

}

}

}

Sleep(1000)

})

// variables in the table of status bar

var tbl = {

type : "table",

title : "account information",

cols : [],

rows : []

}

// write the data in the table structure of status bar

tbl.cols.push("--")

tbl.rows.push(["initial"])

tbl.rows.push(["current"])

_.each(account, function(val, key) {

if (typeof(initAccount[key]) == "number") {

tbl.cols.push(key)

tbl.rows[0].push(initAccount[key]) // initial

tbl.rows[1].push(val) // current

}

})

// display the status bar table

LogStatus(_D(), "\n", "profit:", getProfit(account, initAccount, lastPrices), "\n", "`" + JSON.stringify(tbl) + "`")

}

}

Chiến lược Backtest

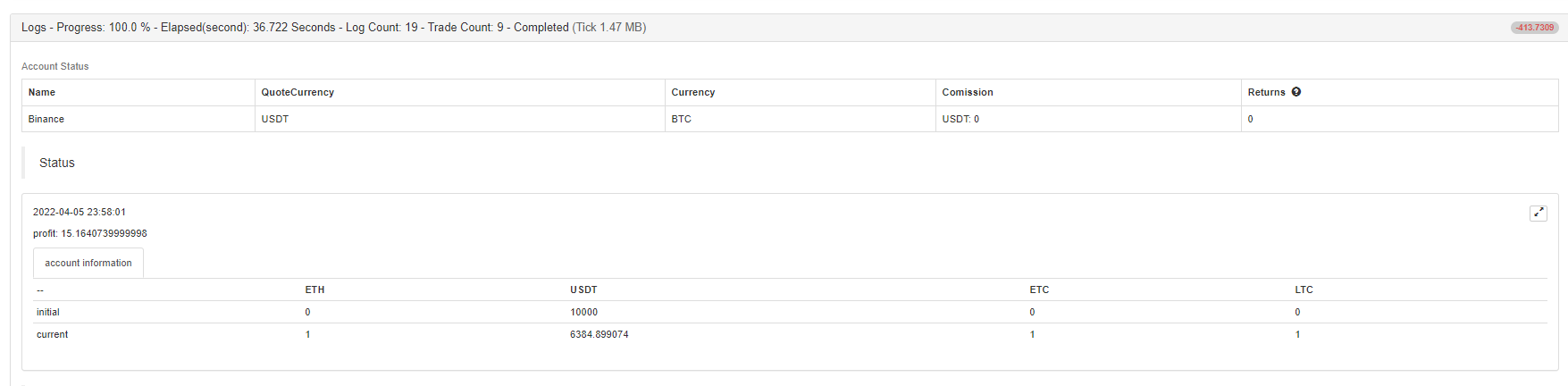

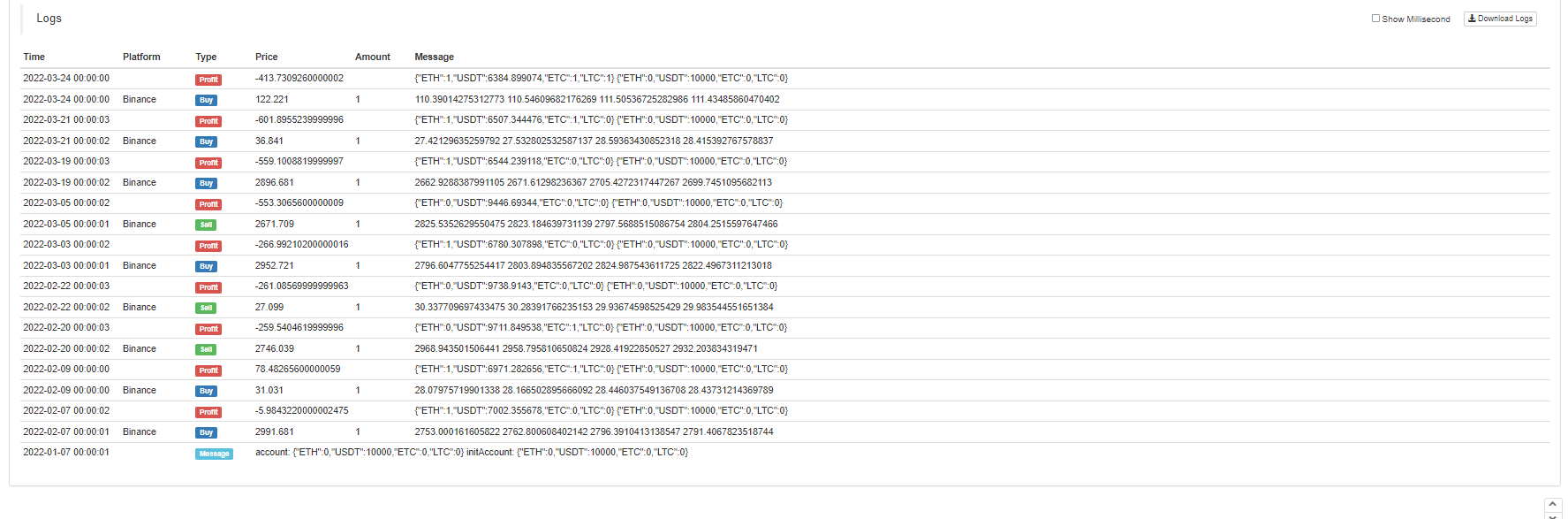

Bạn có thể thấy ETH, LTC và ETC tất cả đều có giao dịch theo các kích hoạt của thập tự vàng và thập tự chết của đường trung bình động.

Bạn cũng có thể chờ trên robot mô phỏng để thử nghiệm.

Mã nguồn chiến lược:https://www.fmz.com/strategy/333783

Chiến lược này chỉ được sử dụng để kiểm tra lại và học thiết kế chiến lược, vì vậy hãy sử dụng nó trong bot một cách thận trọng.

- FMZ là nền tảng để trả tiền

- Cryptocurrency Contract Simple Order-Supervising Bot

- Bạn muốn lấy một khung thời gian tương ứng khi sử dụng getdepth

- Bỏ qua, giải quyết

- Vấn đề giá trị mặt

- Ví dụ thiết kế chiến lược dYdX

- Khám phá ban đầu về ứng dụng Python Crawler trên FMZ

Crawling Binance Content Announcement - Nghiên cứu thiết kế chiến lược phòng ngừa rủi ro & Ví dụ về lệnh chờ giao dịch tại chỗ và tương lai

- Tình hình gần đây và hoạt động khuyến nghị của chiến lược tỷ lệ tài trợ

- Chiến lược điểm cắt trung bình động kép của hợp đồng tương lai tiền điện tử (Giảng dạy)

- Thực hiện Fisher Indicator trong JavaScript & Plotting trên FMZ

- Người quản lý

- 2021 Cryptocurrency TAQ Review & Chiến lược bỏ lỡ đơn giản nhất tăng 10 lần

- Cryptocurrency Futures Multi-Symbol ART Strategy (Giảng dạy)

- Nâng cấp! Cryptocurrency tương lai chiến lược Martingale

- Chức năng Getrecords không thể lấy biểu đồ K theo giây

- Thiết kế hệ thống quản lý đồng bộ dựa trên FMZ (2)

- Dữ liệu về khối lượng mà Getticker trả về không đúng

- Thiết kế hệ thống quản lý đồng bộ dựa trên lệnh FMZ (1)

- Thiết kế một thư viện vẽ nhiều biểu đồ