This is my BTCUSDTPERP 15 min bot

Best results are on BTCUSDTPERP at binancefutures

Results depends of specific volume indicators that works best at binancefutures

15min bots are really fast, Its hard to find a good configurations, becouse of 15min backtesting which least around 3-4 months

This bot is specyfic got really high % profitable trades . Profit net is alsmo really good. However 15min bots are extremly hard to use in long-term, so I made as deflaut settings as I can.

So,

This bot using 11 difrent indicators:

-

ADX

-

RANGE FILTER

-

SAR

-

RSI

-

TWAP

-

JMA

-

MACD

-

VOLUME DELTA

-

VOLUME WEIGHT

-

MA

and the last one for the better results at qucik charts (15min) I decided to add : -

STOCH

-

ADX - - makes a solid view to trend without any scam wick : Long only on green bars, Shorts only on red bars. That's helps my strategy to define a right trend, there is also a orange option for unidentified trends.

-

RANGE FILTER - this indicator is for the better view of trends, define trends, that is important for every bull/bear traps which helps a lot becouse of the very variable trends.

-

SAR - The parabolic SAR is a technical indicator used to determine the price direction of an asset, as well as draw attention to when the price direction is changing. SAR supporting bot, to not open new trades when the trends are slowly changing

-

RSI- value helps strategy to stop trade in right time. When RSI is overbought strategy don't open new longs , also when RSI is oversold strategy don't open new shorts

-

TWAP - has the same task like Range filter, is only for better view of trends, define trends.

-

JMA - The Jurik Moving Average indicator is one of the surest ways to smoothen price curves within a minimum time lag. The indicator offers currency traders one of the best price filters during strong price moves. In this time, when bitcoin price action is so strong, this indicator is necessary.

-

MACD - Moving average convergence divergence ( MACD ) is a trend-following momentum indicator that shows the relationship between two moving averages of a security’s price. The MACD is calculated by subtracting the 26-period exponential moving average ( EMA ) from the 12-period EMA .

Today, macd just like JMA is neccessary to make a profitable bots. -

Volume Delta - A Cumulative Volume Delta approach based on the Bull and Bear Balance Indicator by Vadim Gimelfarb published in the October 2003 issue of the S&C Magazine. Adjust the length of the moving average according to your needs (Symbol, Timeframe, etc.)

-

Volume Weight - is the most important indicator for the strategy, to avoid open trades on flat chart, new trades are open after a strong volume bars.

-

MA 5-10-30 - like previous ones this is for better view of trends, and correctly define the trends, also Speed_MA are using for predict the future price action.

-

Stochastic- stoch is useful for predicting trend reversals. It also focuses on price momentum and can be used to identify overbought and oversold levels

Enjoy ;)

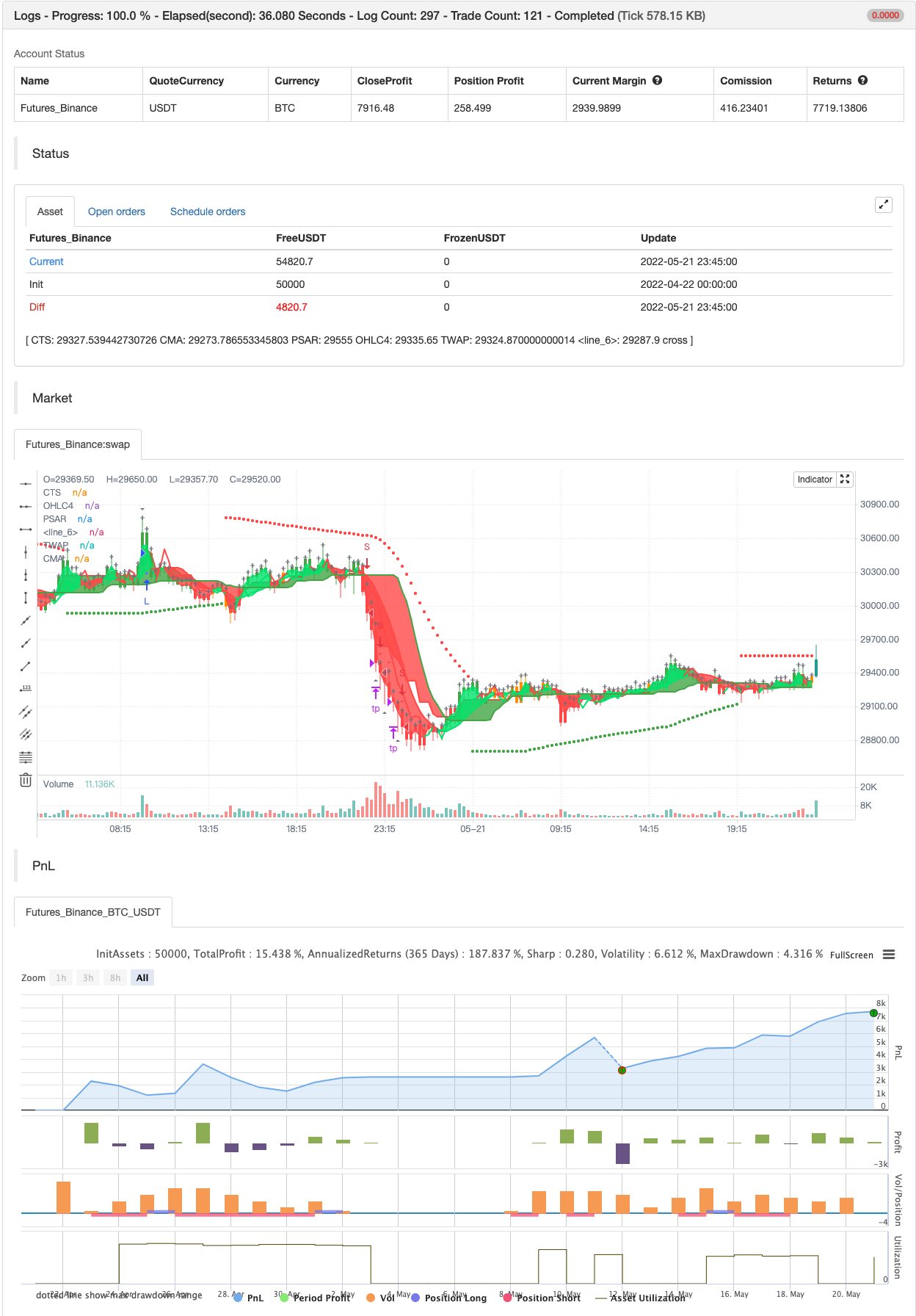

backtest

- 1