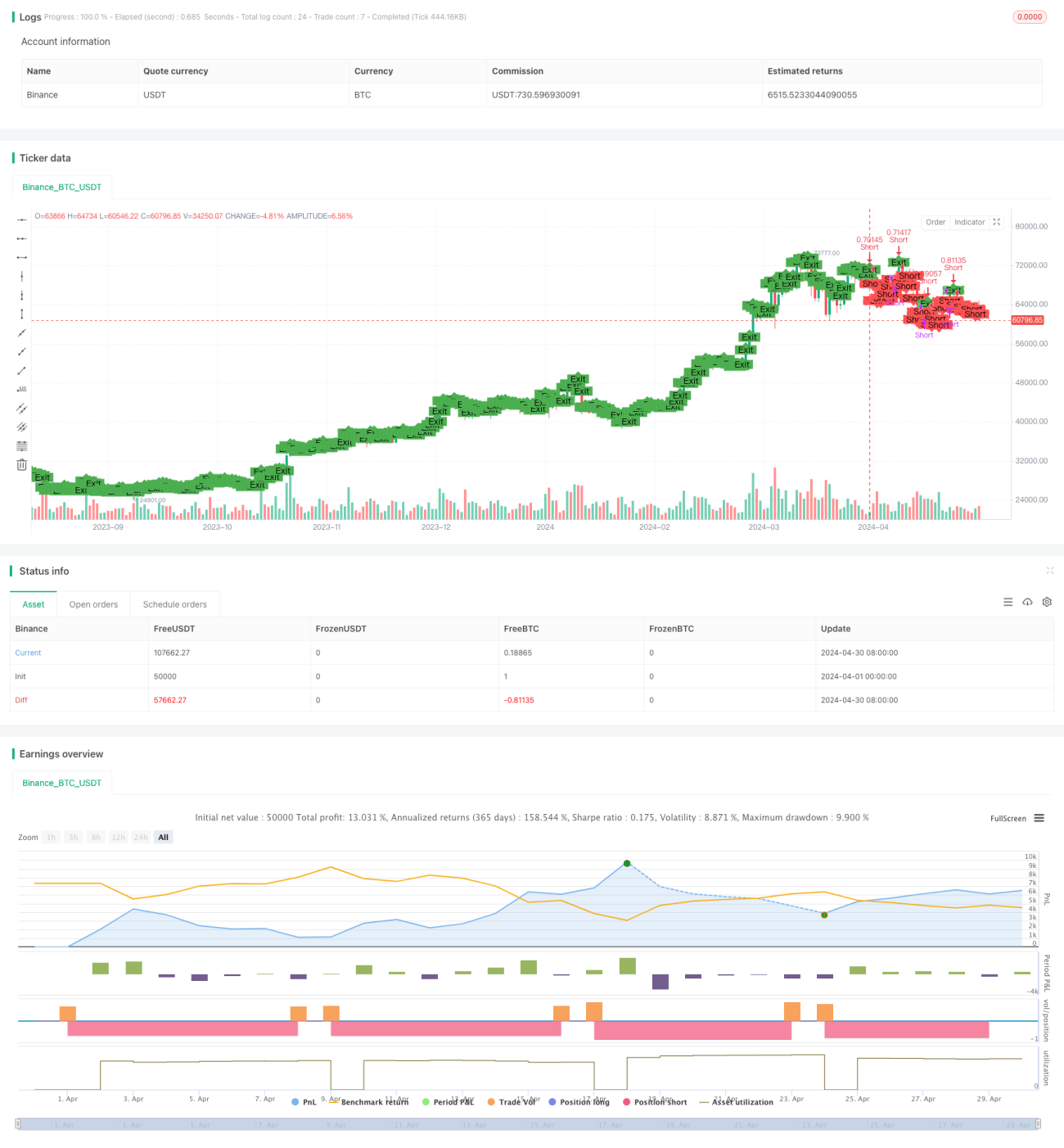

Overview

This strategy is a short-term forex trading strategy that focuses on enhancing risk management by dynamically adjusting position sizes. The strategy calculates the dynamic position size based on the current account equity and the risk percentage per trade. Additionally, it sets strict stop-loss and take-profit conditions to quickly close positions when prices move unfavorably and lock in profits when prices move in a favorable direction.

Strategy Principles

- Initialize relevant variables based on user input parameters, such as the number of days for short-term holding, price drop percentage, risk percentage per trade, stop-loss percentage, and take-profit percentage.

- When there is no open position, calculate the dynamic position size based on the current account equity and risk percentage per trade, and then open a short position at the market price.

- Record the entry price and the expected exit time.

- During the holding period, continuously monitor price movements. If the price reaches the stop-loss price, take-profit price, or the preset holding time, close the short position.

- Mark the entry and exit points on the chart to visually display the trading situation.

Advantage Analysis

- Dynamic Position Sizing: By dynamically adjusting the position size for each trade based on account equity and risk percentage, the strategy improves capital utilization while controlling risks.

- Strict Stop-Loss and Take-Profit: Setting tight stop-loss and take-profit levels effectively controls the risk exposure of individual trades while timely locking in profits.

- Short-Term Trading: The strategy focuses on short-term trading opportunities with shorter holding periods, allowing quick adaptation to market changes and capturing short-term price fluctuations.

- Simple and User-Friendly: The strategy logic is clear, and parameter settings are simple, making it suitable for beginners to learn and use.

Risk Analysis

- Market Risk: The forex market is highly dynamic, with intense short-term price fluctuations that may cause the strategy to frequently trigger stop-losses.

- Parameter Setting Risk: Inappropriate parameter settings, such as excessively high risk percentages or overly narrow stop-loss and take-profit ranges, may lead to rapid account blowouts.

- Position Size Risk: Although the strategy employs dynamic position sizing, it is still necessary to cautiously set the risk percentage for each trade to avoid allocating too much capital to a single trade.

Optimization Directions

- Introduce more technical indicators, such as moving averages and MACD, to assist in judging trends and entry/exit timing.

- Optimize the stop-loss and take-profit logic, such as using trailing stop-losses and partial take-profits, to improve the strategy's risk-reward ratio.

- Set different parameter combinations for various currency pairs and market conditions to enhance the adaptability and stability of the strategy.

- Incorporate position management logic, such as using the Kelly Criterion, to dynamically adjust the risk percentage for each trade.

Summary

By utilizing dynamic position sizing and strict stop-loss and take-profit rules, this strategy achieves a balance between risk control and profit pursuit in short-term trading. The strategy logic is simple and clear, making it suitable for beginners to learn and master. However, caution is still needed in practical application, with attention paid to risk control and continuous optimization and improvement based on market changes. By introducing more technical indicators, optimizing stop-loss and take-profit logic, setting parameters for different market conditions, and incorporating position management, the strategy's robustness and profitability can be further enhanced.

- 1