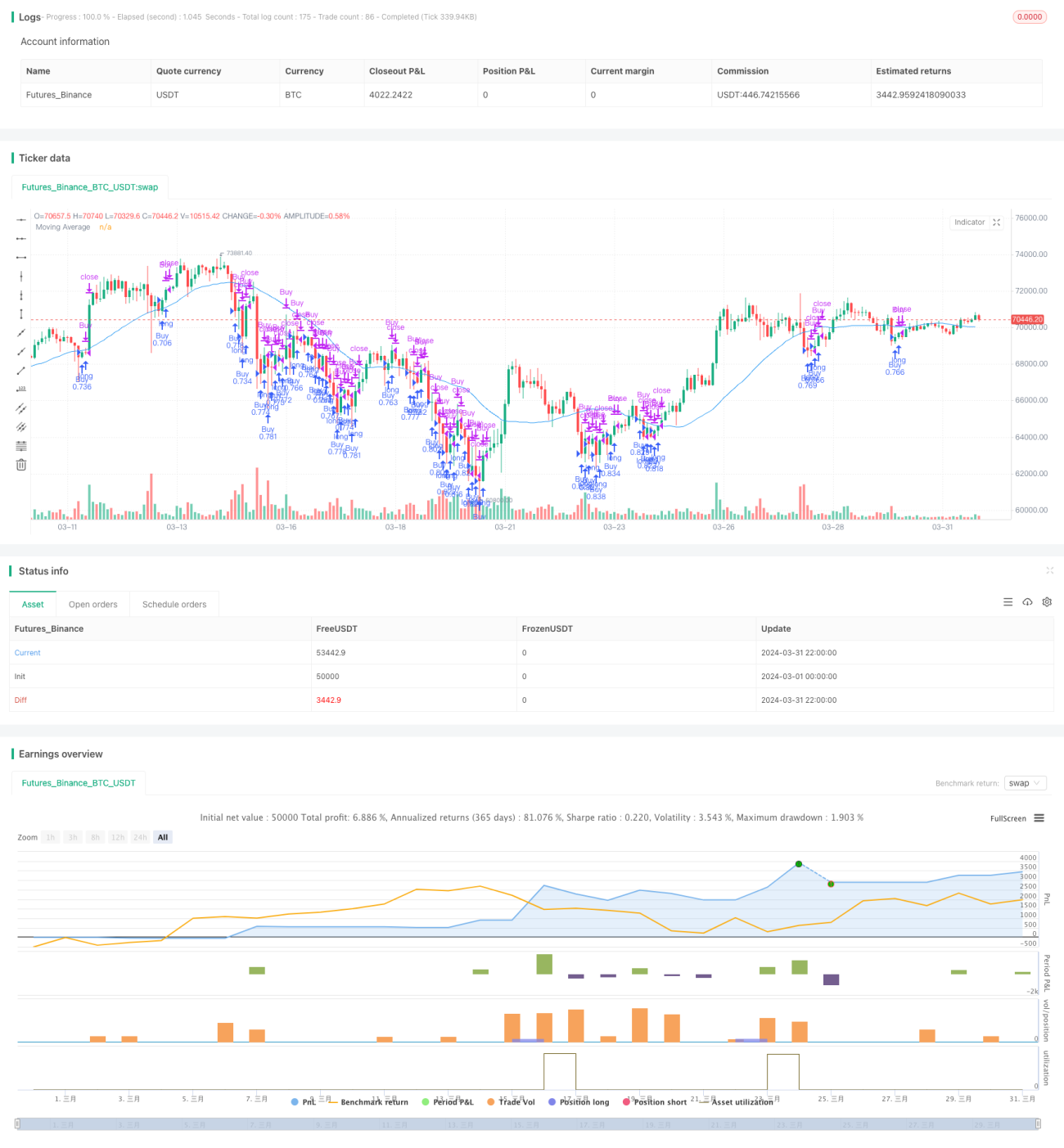

Turnaround Tuesday Strategy (Weekend Filter)

Overview

The strategy is named "Turnaround Tuesday Strategy (Weekend Filter)". The main idea is to buy at the Monday open and sell at the Wednesday open when certain conditions based on moving averages and other filters are met, in order to capture the Tuesday turnaround. By filtering with RSI, ATR, and excluding specific times like May, the strategy aims to improve its win rate and risk-reward ratio.

Strategy Principles

- Use the 30-day moving average as a trend determination basis. When the previous trading day's close is below the 30-day MA, it is considered a downtrend and meets one of the buying conditions.

- Use the 3-day RSI and 10-day ATR as filter conditions. When the 3-day RSI is less than 51 and the close relative to the 10-day ATR is less than 95%, the market sentiment is considered pessimistic but without extreme conditions, meeting the buying conditions.

- Exclude the month of May due to the "Sell in May and go away" effect, as the stock market tends to be sluggish.

- Combining the above conditions, buy on Monday when all filter conditions are met, and sell at the Wednesday open.

Strategy Advantages

- The combination of moving average and sentiment indicators can effectively capture the Tuesday turnaround.

- The dual filtering of RSI and ATR excludes trades in extreme conditions, improving the strategy's win rate and risk-reward ratio.

- Excluding May avoids trading during typically underperforming periods, enhancing strategy performance.

- Trading only from Monday to Wednesday results in low trading frequency and small commission costs.

Strategy Risks

- The strategy may underperform when the trend is strong and the reversal is not evident.

- Fixed buying and selling times may miss better entry and exit points, limiting the strategy's flexibility and profit potential.

- Relying on indicator judgments risks invalidity when the market changes drastically.

- Monthly judgments based on historical experience do not guarantee future situations will be the same, posing a timeliness risk.

Strategy Optimization Directions

- Consider introducing more effective filtering indicators, such as volume and volatility, to improve the strategy's robustness and adaptability.

- Optimize the selection of buying and selling timings, such as adding intraday breakout confirmation conditions, to increase flexibility and profit potential.

- For holding period optimization, consider longer holding times to more fully capture trends.

- Set different parameters for different market conditions to enhance the strategy's adaptability.

- Incorporate position management and risk control modules to cope with extreme market situations.

Summary

The Turnaround Tuesday Strategy (Weekend Filter) uses a combination of moving averages, RSI, ATR, and other indicators to buy and sell at specific times, aiming to capture the Tuesday turnaround. The strategy has low trading frequency, small commission costs, and improves its win rate and risk-reward ratio through time period and indicator filtering. However, the strategy also has certain limitations and risks, such as underperformance in trending markets and fixed buying/selling times and holding periods. Future optimizations can introduce more filtering conditions, optimize exit timings, dynamically adjust parameters, manage positions, and control risk to better adapt to changing market conditions.

- 1