Overview

This is an adaptive trend-following strategy that combines volatility and Williams Percent Range indicators. The strategy adjusts trend determination sensitivity by calculating price range and custom counters, achieving better adaptability in different market conditions. The core mechanism involves dynamically adjusting Williams indicator parameters based on price volatility to more accurately capture market trend transition points.

Strategy Principles

The strategy begins by calculating price range and its moving average (AvgRange) within a period. By comparing real-time price changes with average volatility range, it establishes two counters (TrueCount and TrueCount2) to record significant volatility frequency. These counters are used to dynamically adjust Williams indicator calculation parameters, allowing the strategy to automatically adapt its sensitivity based on market volatility conditions. Buy or sell signals are generated when the adjusted Williams indicator values break through preset thresholds.

Strategy Advantages

- Strong Adaptability - Strategy maintains stable performance across different market environments through volatility adaptation mechanism

- Comprehensive Risk Control - Built-in RISK parameter allows traders to adjust strategy aggressiveness based on risk preference

- Clear Signals - Uses clear breakthrough signal mechanism to avoid false signals

- Good Scalability - Strategy framework allows integration of other technical indicators for optimization

- High Computational Efficiency - Uses simple and efficient calculation methods suitable for real-time trading

Strategy Risks

- Parameter Sensitivity - Choice of ASClength and RISK parameters significantly affects strategy performance

- Market Environment Dependency - May generate excessive trading signals in oscillating markets

- Latency - Use of moving averages may cause entry and exit delays

- False Breakouts - False signals may occur during high volatility periods

Recommend optimizing parameters through backtesting and combining with other confirmation indicators to reduce risks.

Optimization Directions

- Incorporate Volume Indicators - Confirm trend change validity through volume analysis

- Optimize Counter Logic - Consider using more complex statistical methods to evaluate market volatility

- Add Stop Loss Mechanism - Suggest implementing dynamic stop loss for better risk control

- Market Environment Filtering - Add market condition assessment module to avoid trading in unsuitable conditions

- Parameter Adaptation - Develop parameter auto-optimization mechanism to improve strategy adaptability

Summary

This innovative strategy combines volatility analysis and trend following, improving strategy stability and reliability through adaptive mechanisms. While inherent risks exist, the strategy can maintain stable performance across various market conditions through proper parameter settings and optimization implementation. The strategy framework allows for further expansion and optimization, showing good development potential.

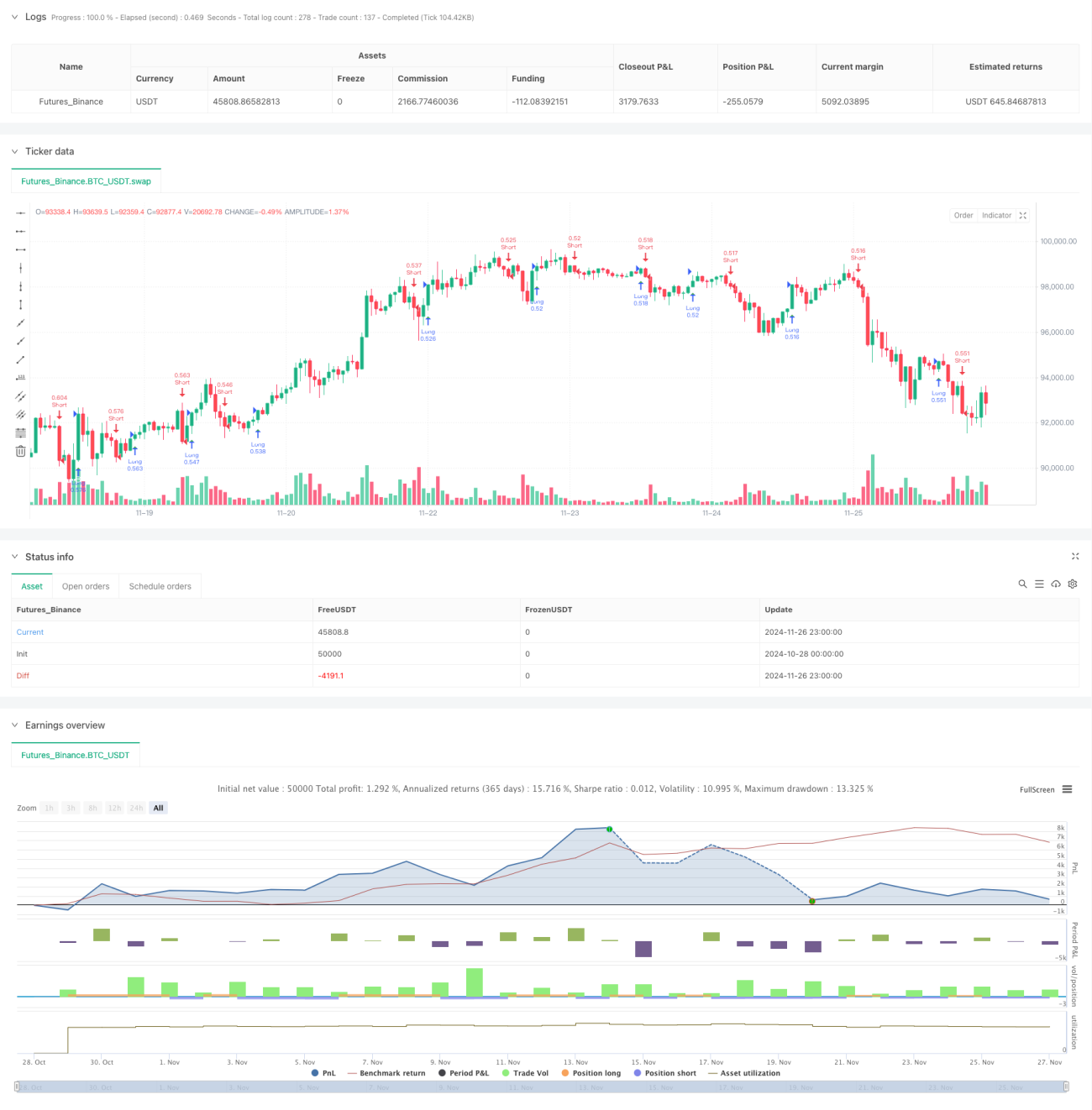

/*backtest

start: 2024-10-28 00:00:00

end: 2024-11-27 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("ASCTrend", shorttitle="ASCTrend", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

eternalfg = input(false, title="eternal 確定")- 1