Overview

This strategy is a comprehensive trading system based on the Relative Strength Index (RSI), Moving Averages (MA), and price momentum. It identifies potential trading opportunities by monitoring RSI trend changes, multiple timeframe moving average crossovers, and price momentum changes. The strategy particularly focuses on RSI uptrends and consecutive price increases, using multiple confirmations to enhance trading accuracy.

Strategy Principles

The core logic of the strategy is based on the following key components:

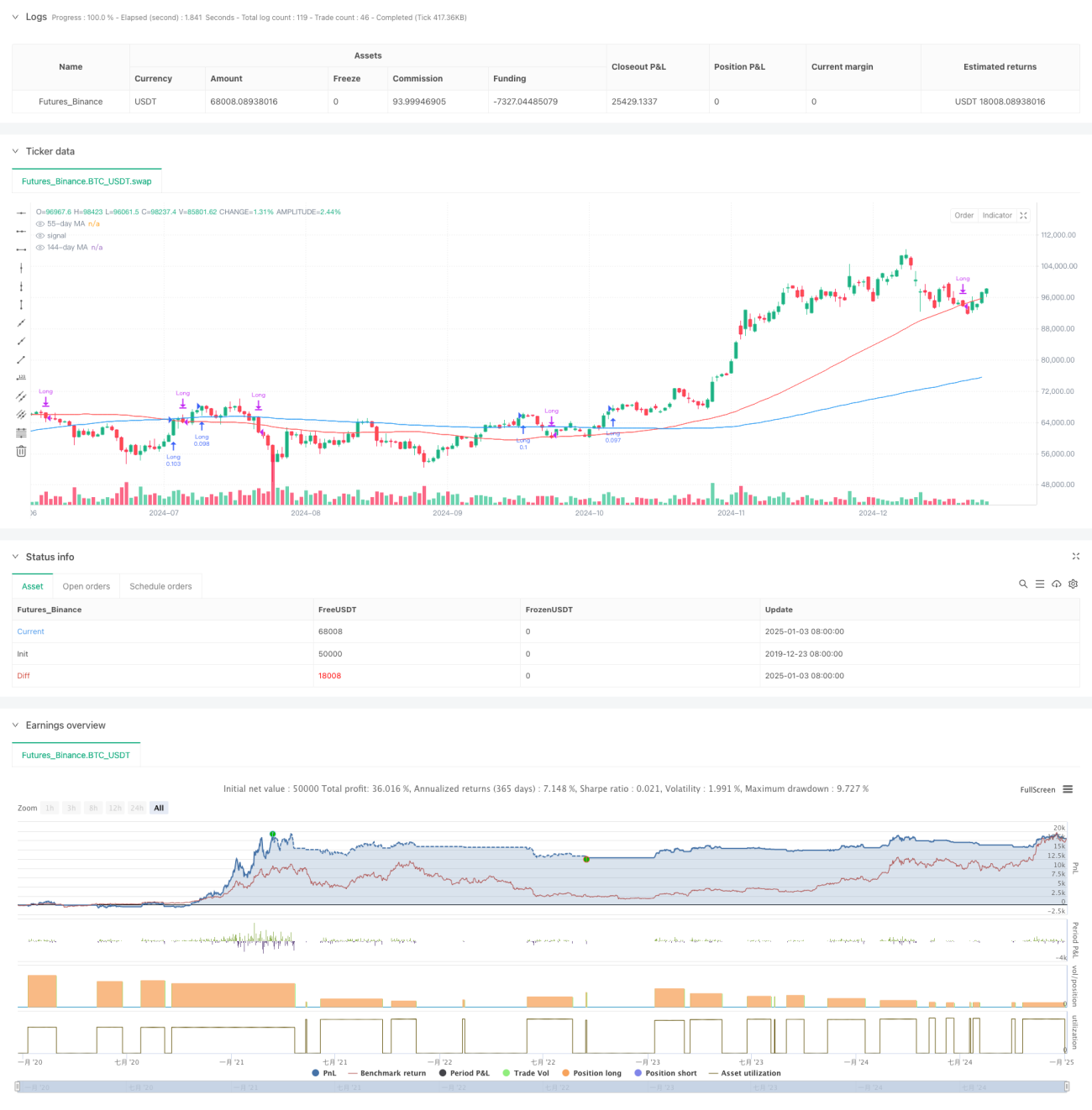

- RSI Trend Analysis: Uses 13-period RSI and its moving average to confirm price strength

- Price Momentum Confirmation: Requires three consecutive higher highs to validate trend continuation

- Multiple Moving Average System: Employs 21-day, 55-day, and 144-day moving averages as trend filters

- Money Management: Uses 10% of account equity for position sizing

Buy conditions require: RSI above its average, consecutive higher highs formation, and maintaining RSI uptrend

Sell conditions include: Price breaking below 55-day MA or RSI crossing below average with price below 55-day MA

Strategy Advantages

- Multiple Confirmation Mechanism: Enhances signal reliability through RSI, price momentum, and MA system verification

- Trend Following Capability: Effectively captures medium to long-term trends while avoiding false breakouts

- Comprehensive Risk Control: Controls risk through position management and clear stop-loss conditions

- High Adaptability: Applicable to different timeframes and market conditions

- Rational Money Management: Uses account equity percentage for position sizing, avoiding fixed position risks

Strategy Risks

- Lag Risk: Moving averages and RSI indicators have inherent lag, potentially causing delayed entries and exits

- Sideways Market Risk: May generate frequent false signals in ranging markets

- Consecutive Loss Risk: May face consecutive stops during market regime changes

Solutions:

- Add market environment filters

- Optimize indicator parameters

- Introduce volatility adaptive mechanisms

Strategy Optimization Directions

- Indicator Parameter Optimization:

- Consider adaptive RSI periods

- Adjust moving average parameters based on market cycles

- Enhanced Market Environment Recognition:

- Introduce volatility indicators

- Add trend strength filters

- Improved Risk Control:

- Implement dynamic stop-loss mechanisms

- Add profit target management

- Position Management Optimization:

- Adjust position size based on signal strength

- Implement scaled entry and exit mechanisms

Summary

This strategy constructs a relatively complete trading system through the comprehensive use of technical analysis indicators and momentum analysis methods. Its strengths lie in its multiple confirmation mechanisms and comprehensive risk control, though market environment adaptability and parameter optimization remain important considerations. Through continuous optimization and improvement, this strategy has the potential to become a robust trading system.

- 1