2

关注

502

关注者

概述

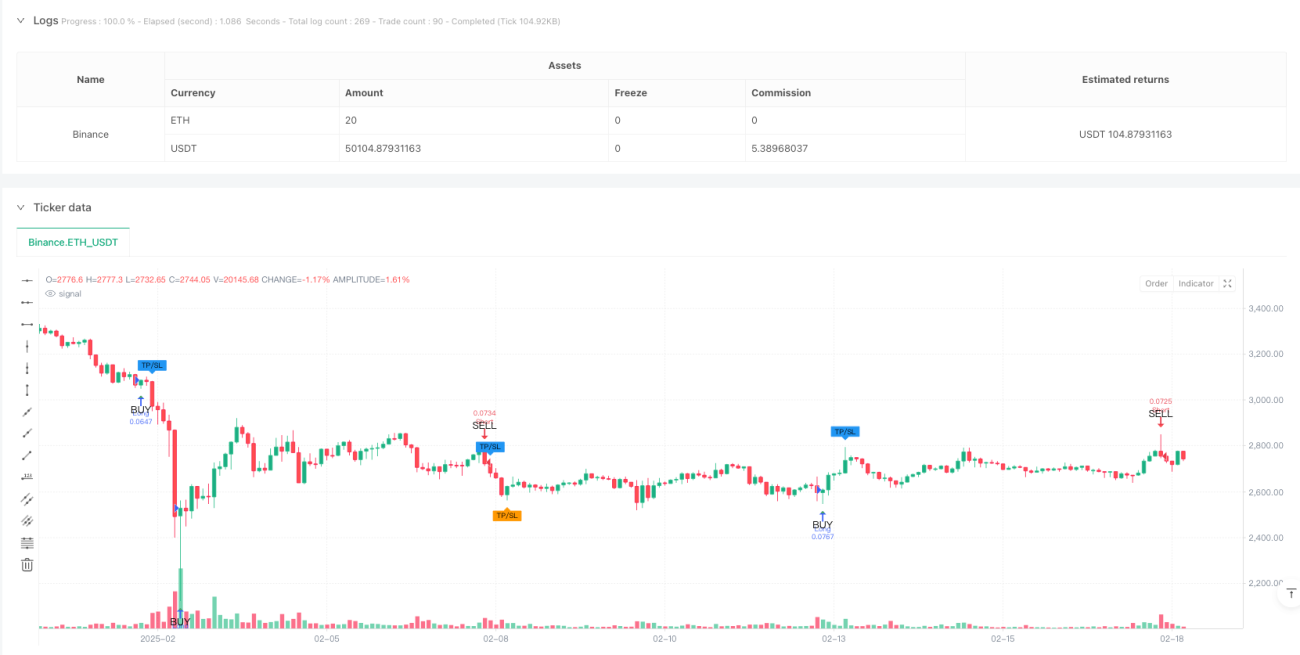

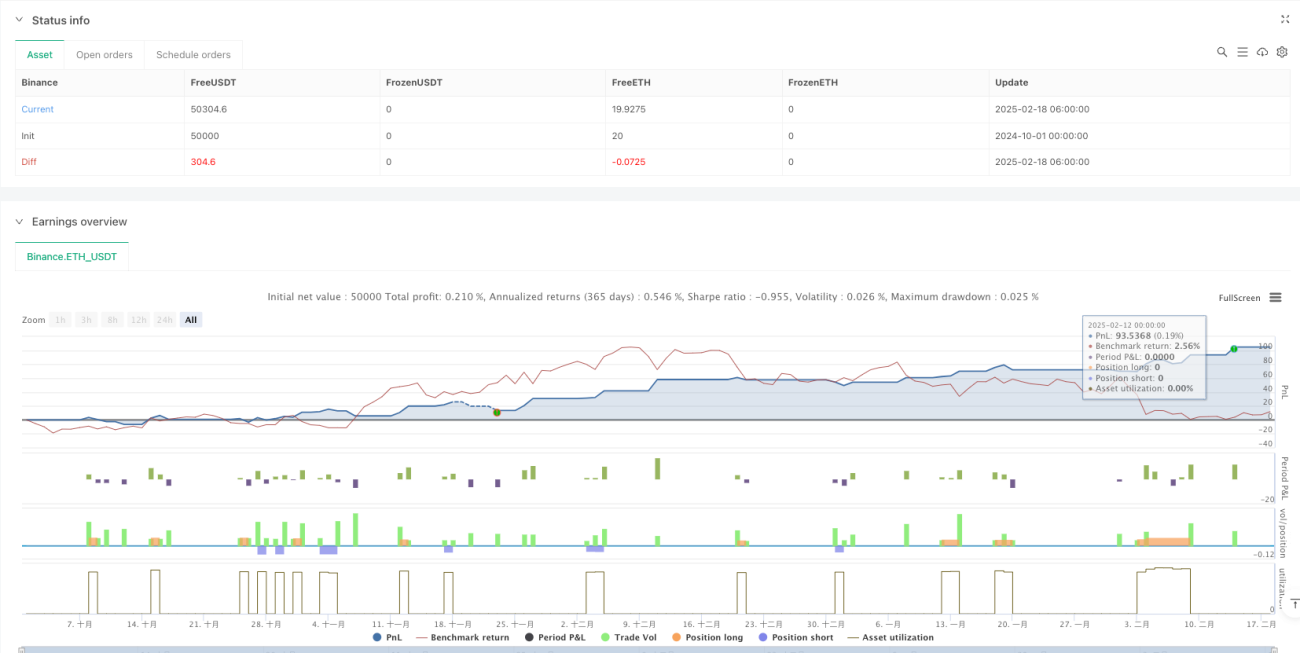

该策略是一个结合了多个技术指标的完整交易系统,主要基于Z分数来衡量交易量和K线实体大小的异常值,并使用ATR(平均真实波幅)来设置动态止损位。系统还整合了风险收益比(RR)来优化获利目标,通过多维度的技术分析提供可靠的交易信号。

策略原理

策略的核心逻辑基于以下几个关键组件:

- Z分数分析:计算交易量和K线实体的标准差,识别市场异常活跃度

- 趋势确认:通过分析相邻K线的高低点和收盘价来确认趋势方向

- ATR止损:使用动态ATR值设置止损位置,提供更灵活的风险控制

- 风险收益比:基于设定的RR比例自动计算获利目标

- 可视化标记:在图表上标注交易信号和关键价格水平

策略优势

- 多维度信号确认:结合成交量、价格动量和趋势方向,提高交易信号的可靠性

- 动态风险管理:通过ATR实现自适应止损,better适应市场波动

- 灵活的参数配置:允许调整Z分数阈值、ATR倍数和风险收益比

- 精确的入场时机:使用Z分数异常值识别关键交易机会

- 清晰的可视化:在图表上明确标注入场点、止损位和获利目标

策略风险

- 参数敏感性:Z分数阈值和ATR倍数的设置直接影响交易频率和风险控制

- 市场环境依赖:在低波动率环境下可能产生较少的交易信号

- 计算复杂性:多重指标计算可能导致信号生成延迟

- 滑点风险:在快速市场中可能面临实际执行价格与信号价格的偏差

- 假突破风险:在盘整市场中可能触发错误的突破信号

策略优化方向

- 市场环境过滤:添加市场波动率过滤器,在不同市场环境下动态调整参数

- 信号确认机制:引入更多技术指标进行交叉验证,如RSI或MACD

- 仓位管理优化:基于波动率和账户风险实现动态仓位调整

- 多时间周期分析:整合更高时间周期的趋势确认,提高交易成功率

- 信号过滤优化:增加额外的过滤条件以减少假信号

总结

该策略通过结合Z分数分析、ATR止损和风险收益比优化,构建了一个完整的交易系统。系统的优势在于多维度的信号确认和灵活的风险管理,但仍需注意参数设置和市场环境的影响。通过建议的优化方向,策略可以进一步提升其稳定性和适应性。

策略源码

Pine

/*backtest

start: 2024-10-01 00:00:00

end: 2025-02-18 08:00:00

period: 2h

basePeriod: 2h

exchanges: [{"eid":"Binance","currency":"ETH_USDT"}]

*/

//@version=5

strategy("admbrk | Candle Color & Price Alarm with ATR Stop", overlay=true, initial_capital=50, default_qty_type=strategy.cash, default_qty_value=200, commission_type=strategy.commission.percent, commission_value=0.05, pyramiding=3)

// **Risk/Reward ratio (RR) as input**策略参数

相关策略

评论

全部评论 (0)

暂无数据

- 1