2

关注

502

关注者

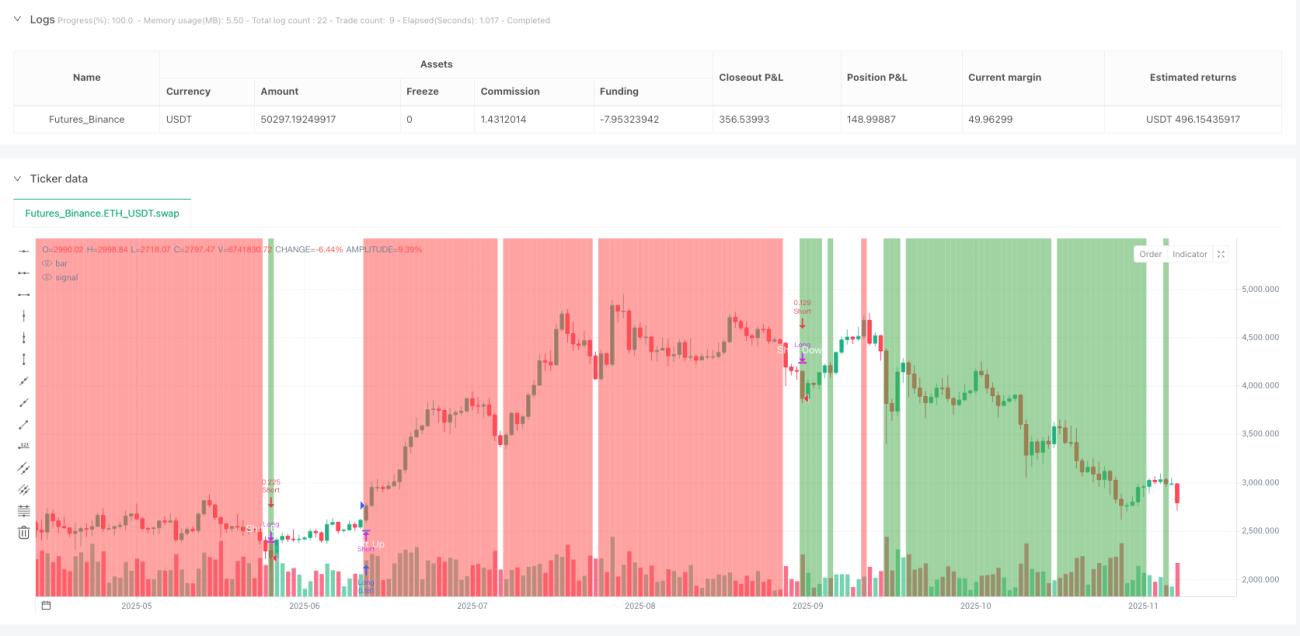

🎯 这个策略到底在干什么?

你知道吗?这个策略就像是市场的"情绪识别器"!📊 它专门捕捉那些让散户措手不及的关键转折点。想象一下,如果你能提前知道股价什么时候要"变脸",是不是就像拥有了交易的超能力?

这个策略的核心思路超级简单:当价格突破重要的高点或低点时,市场结构就发生了转变。就像你在爬山时突然发现前面是下坡路一样,趋势的改变往往就在这一瞬间!

🔍 划重点!三大核心机制

1. 摆动点识别系统 🎢

策略会自动找出过去一段周期内的重要高点和低点,就像给市场画出"山峰"和"山谷"。当价格突破这些关键位置时,就是趋势可能转变的信号!

2. ATR过滤器 📏

这里有个超聪明的设计!策略不会被小幅波动忽悠,必须要突破幅度达到ATR的一定倍数才算有效。这就像设置了一个"最低门槛",过滤掉那些假突破。

3. 溢价/折价区间框架 💎

最有趣的来了!策略会在价格区间内划分出"便宜区"和"昂贵区"。在便宜区买入,在昂贵区卖出,这不就是投资的黄金法则吗?

🚀 实战优势在哪里?

避坑指南一:告别追涨杀跌!这个策略专门在趋势转折的第一时间入场,让你成为"聪明钱"而不是"接盘侠"。

避坑指南二:风险控制超贴心!可以根据账户比例自动计算仓位大小,还能设置基于区间的止损位,让你睡得安稳。

避坑指南三:视觉化超棒!图表上会自动标记转折点,背景还会变色提示当前是便宜区还是昂贵区,一目了然!

💡 适合什么样的交易者?

如果你是那种喜欢"低买高卖"但总是把握不好时机的交易者,这个策略简直就是为你量身定制的!它特别适合中长期交易者,因为它关注的是市场结构的根本性变化,而不是短期噪音。

记住,最好的策略不是让你每天都交易,而是让你在对的时间做对的事情!🎯

策略源码

Pine

策略参数

相关策略

评论

全部评论 (0)

暂无数据

- 1