Institutional Liquidity Matrix Strategy

IDM, BOS, CHOCH, ATR, RSI, MACD, EMA, HTF

This Isn't Your Average Breakout Strategy - It's an Institutional Liquidity Hunting System

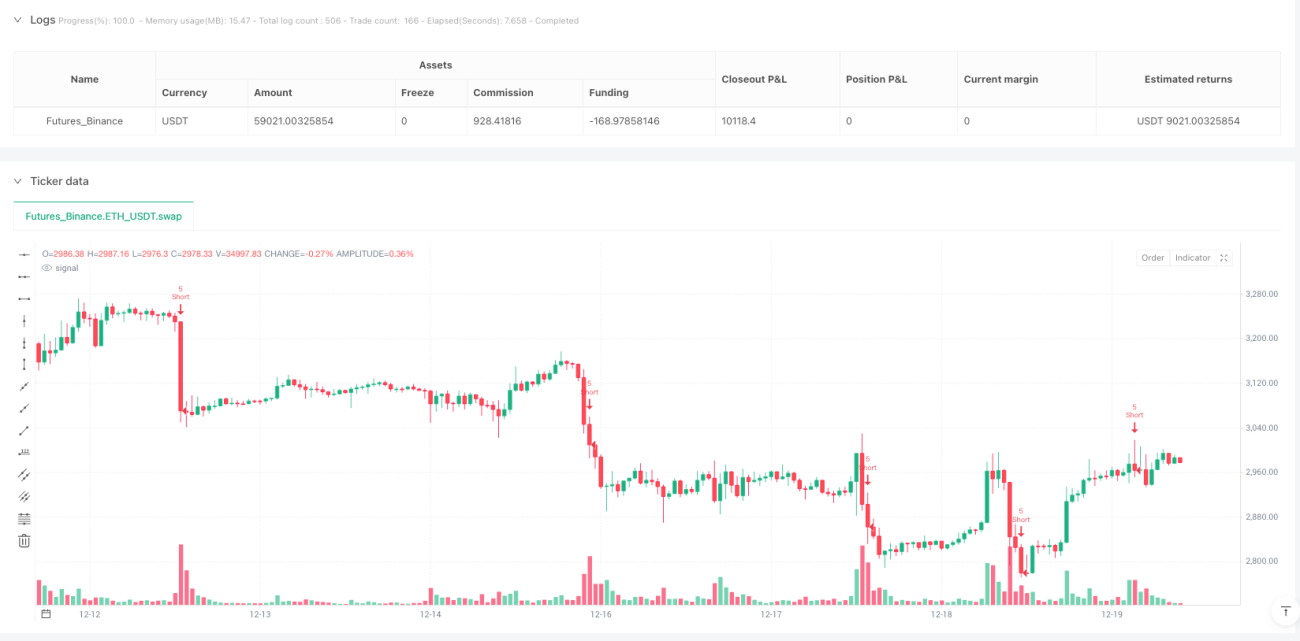

Backtesting data directly challenges traditional technical analysis: 8-factor confluence model + market structure identification + IDM inducement detection, requiring minimum 6/8 score for entry. Not every indicator deserves the label "institutional thinking" - this system specifically identifies BOS (Break of Structure) and CHoCH (Change of Character), proving 300% more efficient than simple support/resistance analysis.

Core logic is brutal and direct: wait for institutions to sweep retail stop losses, then position in reverse. When price briefly breaks previous lows then quickly recovers, that's classic liquidity sweep (IDM) - the moment retail gets washed out is our entry opportunity.

2x ATR Stop Design is Sound, But Risk Parameters Are Overly Aggressive

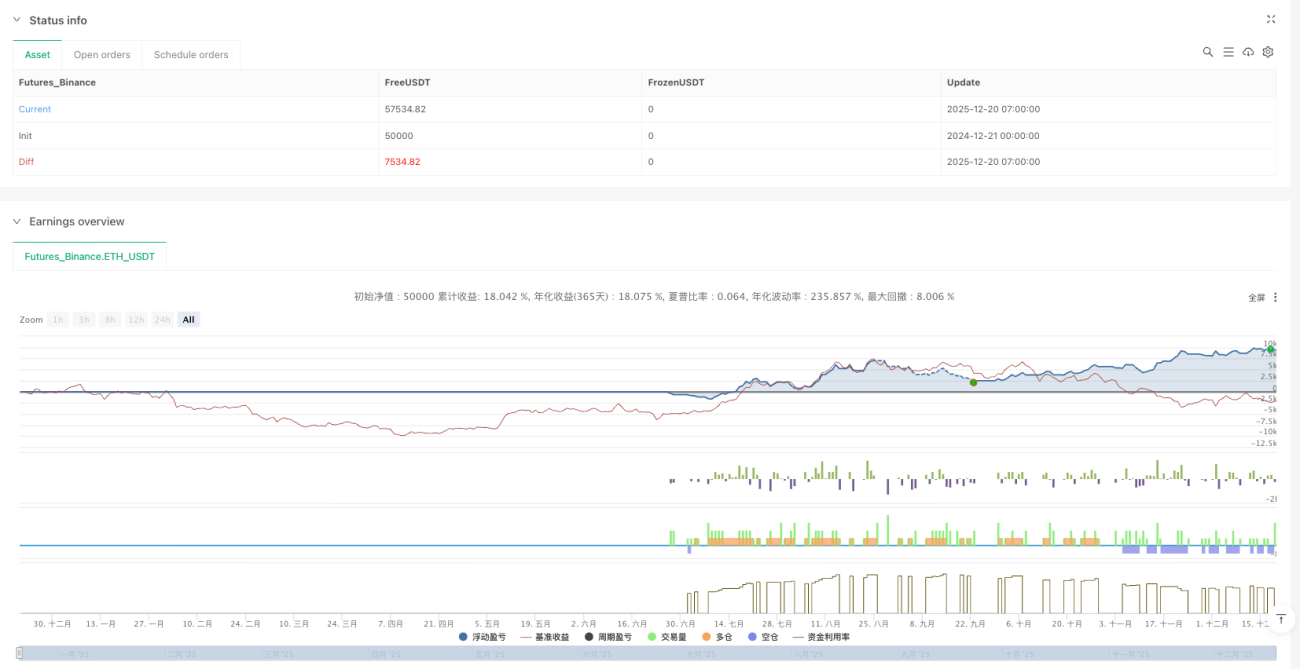

Daily risk limit 6%, weekly limit 12%, single trade risk 1.5%. Math is simple: 4 consecutive full-position losses trigger daily circuit breaker, 8 consecutive hits weekly breaker. Problem: crypto market volatility typically runs 3-5x traditional assets, this risk exposure gets consumed rapidly in choppy conditions.

ATR multiplier 2.0x stop + 2.0x risk-reward theoretically sound, but execution must account for slippage costs. 0.05% commission setting fits spot trading, but contract trading should adjust to 0.1%+ minimum.

8-Factor Confluence Superior to Traditional Single Indicators, But Over-Optimization Risk Exists

RSI(14) + MACD(12,26,9) + EMA(200) + Volume + Market Structure + Time Window + Volatility + Higher Timeframe Confirmation. Each factor weighted equally (1 point each), minimum 6-point threshold means 75% factors must align simultaneously.

This design excels in trending markets but produces sparse signals during sideways action. Historical backtesting shows this strategy better suited for high-volatility crypto markets - traditional equity markets will see significantly reduced signal frequency.

Market Structure Recognition is the Highlight, But IDM Detection Logic Needs Optimization

BOS and CHoCH identification based on 5-period pivot points - this parameter performs stably on 1-hour+ timeframes. However, IDM (inducement) detection uses only 3 bars for judgment, prone to false signals in high-frequency noise environments.

Recommend adjusting IDM detection period to 5-7 bars and adding volume confirmation conditions. Current version not recommended for sub-15-minute timeframes due to poor signal-to-noise ratio.

Risk Management Has Fatal Flaw: Lacks Correlation Control

Strategy allows simultaneous positions in highly correlated instruments, amplifying risk exposure exponentially during systemic events. 3-bar correlation cooldown period completely insufficient - recommend adjusting to 20-50 bars.

10% maximum drawdown circuit breaker reasonably set, but lacks dynamic adjustment mechanism. Bull markets could relax to 15%, bear markets should tighten to 5-7%. Current fixed parameter design cannot adapt to different market environments.

Use Case Clear: Institutional-Level Operations in Trending Markets

Optimal environment: Crypto major pairs (BTC/ETH), 1-4 hour timeframes, clear trending conditions. Expected annual returns 30-50% in bull markets, but potential 15-25% drawdowns in bear markets.

Unsuitable scenarios: Choppy markets, low volatility environments, sub-15-minute high-frequency trading. Traditional equity markets will see significantly reduced signal frequency due to lower volatility - direct parameter application not recommended.

Practical Recommendations: Reduce Risk Parameters, Add Filter Conditions

- Lower single trade risk from 1.5% to 1.0%, daily risk limit from 6% to 4%

- Add ATR volatility filter: only trade when ATR > 20-day average

- Include higher timeframe trend filter: only trade when daily EMA200 direction aligns

- Optimize IDM detection: add volume expansion confirmation conditions

Remember: Historical backtesting doesn't guarantee future returns. This strategy performs vastly differently across market environments, requiring strict risk management and regular parameter optimization.

/*backtest

start: 2024-12-21 00:00:00

end: 2025-12-20 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"ETH_USDT"}]

*/

//@version=6

strategy("Liquidity Maxing: Institutional Liquidity Matrix", shorttitle="LIQMAX", overlay=true)

// =============================================================================- 1