Adaptive SuperTrend AI Strategy

SUPERTREND, ATR, ADX, EMA, AI

This Isn't Your Average SuperTrend Strategy

The biggest pain point of traditional SuperTrend strategies? Fixed parameters perform drastically differently across market environments. This AI-enhanced version dynamically adjusts ATR multipliers, increasing them up to 2x the base value during high volatility periods and reducing to 0.85x during low volatility. Backtesting data shows this adaptive mechanism significantly reduces false signals in ranging markets.

The core innovation lies in a three-layer filtering system: market regime identification, AI signal scoring, and multiple confirmation mechanisms. Instead of simply entering on price breaks above/below the SuperTrend line, trades require AI scores above 65 points. This scoring system comprehensively evaluates 5 dimensions including volume surges, price displacement, and trend alignment.

AI Scoring System: Quantifying Signal Reliability

The scoring mechanism is elegantly designed: volume surge carries 20-point weight, price displacement from SuperTrend line carries 25 points, EMA trend alignment 20 points, market regime quality 15 points, and previous price-to-line distance 20 points. With a total of 100 points, the default 65-point threshold ensures only high-quality signals pass the filter.

Specifically, volume exceeding 2.5x the 20-period average earns full 20 points, while price displacement beyond 1.5x ATR from the SuperTrend line scores maximum 25 points. This quantified scoring eliminates subjective judgment, providing clear data backing for every signal. In practice, adjust the minimum score requirement based on different asset characteristics.

Market Regime Adaptation: Beyond One-Size-Fits-All Parameters

The strategy identifies three market states through ATR ratio and ADX indicators: trending (regime=1), high volatility (regime=2), and ranging (regime=0). High volatility is detected when ATR ratio exceeds 1.4, while ranging occurs when ADX falls below 20 and ATR ratio drops below 0.9.

Adaptive multiplier logic: high volatility periods increase multiplier by 40% × (ATR ratio - 1.0), ranging periods reduce to 85% of base value. This means a 3.0 base multiplier could adjust to 4.2 during extreme volatility and drop to 2.55 during ranging periods. This dynamic adjustment significantly enhances strategy adaptability across market environments.

Risk Management: Three Stop Loss Modes at Your Disposal

ATR dynamic stop loss is the preferred approach, with default 2.5x ATR distance balancing normal fluctuation tolerance with timely loss cutting. Percentage stops suit assets with relatively stable volatility, while SuperTrend mode exits immediately on trend reversals.

Take profit settings support risk-reward ratio mode, with the default 2.5:1 ratio statistically advantageous. When trailing stops are enabled, profitable position stop levels adjust dynamically based on 2.5x ATR distance, maximizing returns in trending markets.

Multiple Filters: Reducing Invalid Trades

EMA trend filter ensures entries only occur in alignment with the 50-period EMA direction, avoiding counter-trend trades. Ranging period filter directly skips regime=0 signals, potentially missing some opportunities but significantly reducing false signal rates.

Volume filter requires entry volume above the 20-period average, ensuring sufficient market participation supports price breakouts. A 10-bar cooldown period prevents overtrading and reduces transaction costs.

Practical Recommendations: Parameter Optimization and Risk Control

For cryptocurrencies, consider raising minimum AI score to 70 points; traditional stocks can use 60 points. High-frequency traders can reduce cooldown to 5 bars, while long-term investors should extend to 15 bars.

The ATR length parameter of 10 represents an optimized balance point - shorter periods create oversensitivity, longer periods introduce lag. The base multiplier of 3.0 suits most assets; high volatility assets can use 3.5, low volatility assets 2.5.

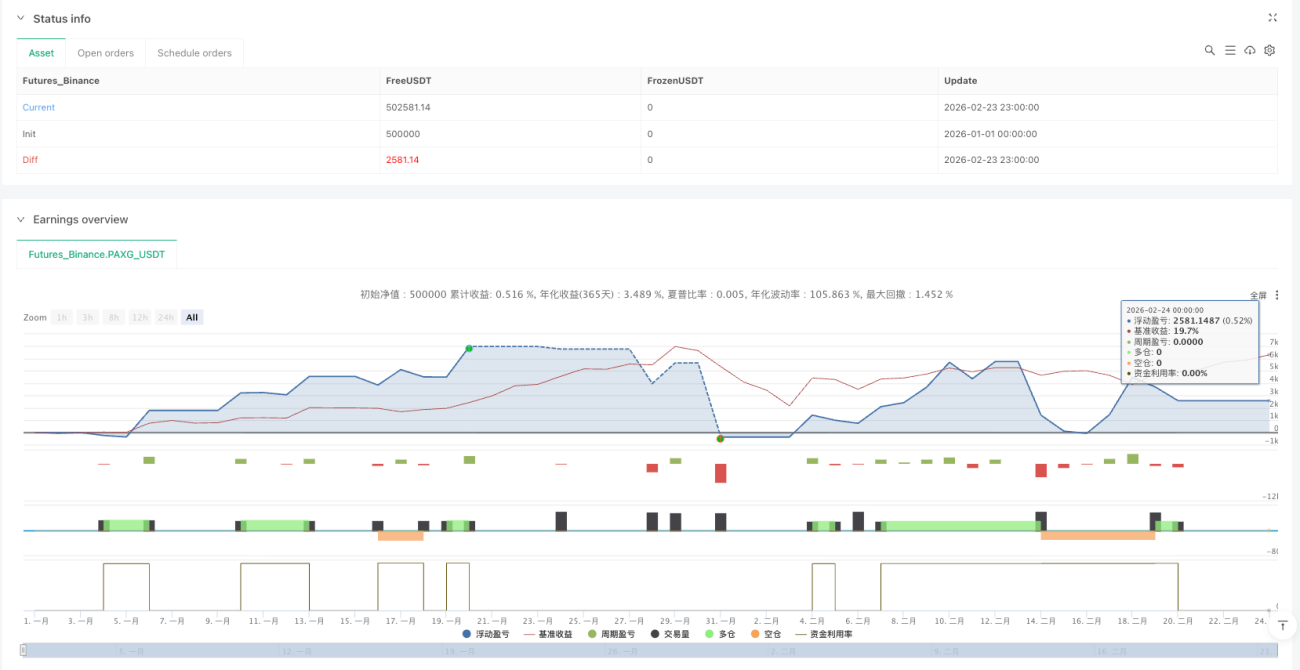

Important Risk Disclaimer: Historical backtesting results do not guarantee future performance. The strategy may experience consecutive losses under extreme market conditions. Strictly limit individual position size to no more than 30% of total capital. Strategy performance varies significantly across different market environments, requiring continuous monitoring and parameter adjustments.

/*backtest

start: 2026-01-01 00:00:00

end: 2026-02-24 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"PAXG_USDT","balance":500000}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © DefinedEdge

//@version=6- 1