dYdX কৌশল নকশা উদাহরণ

লেখক:লিডিয়া, সৃষ্টিঃ ২০২২-১১-০৭ 10:59:29, আপডেটঃ ২০২৩-০৯-১৫ 21:03:43

অনেক ব্যবহারকারীর চাহিদার জবাবে, এফএমজেড প্ল্যাটফর্মটি সম্প্রতি ডিওয়াইডএক্স অ্যাক্সেস করেছে, একটি বিকেন্দ্রীভূত বিনিময়। যে কারও কাছে কৌশল রয়েছে তারা ডিজিটাল মুদ্রা ডিওয়াইডএক্স অর্জনের প্রক্রিয়াটি উপভোগ করতে পারে। আমি দীর্ঘদিন ধরে একটি স্টোকাস্টিক ট্রেডিং কৌশল লিখতে চেয়েছিলাম, এটি লাভজনক কিনা তা বিবেচ্য নয়। সুতরাং পরবর্তী আমরা একসাথে একটি স্টোকাস্টিক এক্সচেঞ্জ কৌশল ডিজাইন করতে আসি, কৌশলটি ভাল সম্পাদন করে কিনা তা বিবেচ্য নয়, আমরা কেবল কৌশল নকশাটি শিখি।

স্টোকাস্টিক ট্রেডিং কৌশল নকশা

আসুন একটি মস্তিষ্ক ঝড় আছে! এটা এলোমেলো সূচক এবং দাম সঙ্গে এলোমেলো অর্ডার স্থাপন একটি কৌশল ডিজাইন করার পরিকল্পনা করা হয়। অর্ডার স্থাপন লং বা শর্ট যাচ্ছে ছাড়া আর কিছুই নয়, শুধু সম্ভাব্যতা উপর বাজি। তারপর আমরা র্যান্ডম সংখ্যা 1 ~ 100 ব্যবহার করা হবে দীর্ঘ বা শর্ট যেতে কিনা তা নির্ধারণ করতে।

লং যাওয়ার শর্তঃ র্যান্ডম নম্বর 1 ~ 50। শর্ট হওয়ার শর্তঃ র্যান্ডম নম্বর 51~100।

সুতরাং লং এবং শর্ট উভয়ই ৫০ টি সংখ্যা। এরপরে, আসুন কীভাবে অবস্থানটি বন্ধ করা যায় তা নিয়ে চিন্তা করি, যেহেতু এটি একটি বাজি, তাই জয়ের বা হারানোর জন্য অবশ্যই একটি মানদণ্ড থাকতে হবে। আমরা লেনদেনে স্থির স্টপ লাভ এবং ক্ষতির জন্য একটি মানদণ্ড সেট করি। জয়ের জন্য স্টপ লাভ, হারানোর জন্য স্টপ ক্ষতি। স্টপ লাভ এবং ক্ষতির পরিমাণ হিসাবে, এটি আসলে লাভ এবং ক্ষতির অনুপাতের প্রভাব, ওহ হ্যাঁ! এটি জয়ের হারকেও প্রভাবিত করে! (এই কৌশল নকশা কার্যকর? এটি ইতিবাচক গাণিতিক প্রত্যাশা হিসাবে গ্যারান্টিযুক্ত হতে পারে? প্রথমে এটি করুন! (তারপরে, এটি কেবল শেখার জন্য, গবেষণা!

ট্রেডিং খরচ মুক্ত নয়, আমাদের স্টোকাস্টিক ট্রেডিং জয়ের হারকে ৫০% এর নিচে নিয়ে যাওয়ার জন্য পর্যাপ্ত স্লিপ, ফি ইত্যাদি রয়েছে। তাহলে কীভাবে এটিকে ধারাবাহিকভাবে ডিজাইন করা যায়? পজিশন বাড়ানোর জন্য মাল্টিপ্লাইকার ডিজাইন করলে কেমন হয়? যেহেতু এটি একটি বাজি, তাই একটানা 8 ~ 10 বার এলোমেলো ট্রেডের জন্য হারানোর সম্ভাবনা কম হওয়া উচিত। সুতরাং প্রথম লেনদেনটি একটি ছোট পরিমাণ অর্ডার দেওয়ার জন্য ডিজাইন করা হয়েছিল, যতটা সম্ভব ছোট। তারপর যদি আমি হেরে যাই, আমি অর্ডার পরিমাণ বাড়াব এবং এলোমেলোভাবে অর্ডার দেওয়া চালিয়ে যাব।

ঠিক আছে, কৌশলটি সহজভাবে ডিজাইন করা হয়েছে।

সোর্স কোড ডিজাইন করা হয়েছেঃ

var openPrice = 0

var ratio = 1

var totalEq = null

var nowEq = null

function cancelAll() {

while (1) {

var orders = _C(exchange.GetOrders)

if (orders.length == 0) {

break

}

for (var i = 0 ; i < orders.length ; i++) {

exchange.CancelOrder(orders[i].Id, orders[i])

Sleep(500)

}

Sleep(500)

}

}

function main() {

if (isReset) {

_G(null)

LogReset(1)

LogProfitReset()

LogVacuum()

Log("reset all data", "#FF0000")

}

exchange.SetContractType(ct)

var initPos = _C(exchange.GetPosition)

if (initPos.length != 0) {

throw "Strategy starts with a position!"

}

exchange.SetPrecision(pricePrecision, amountPrecision)

Log("set the pricePrecision", pricePrecision, amountPrecision)

if (!IsVirtual()) {

var recoverTotalEq = _G("totalEq")

if (!recoverTotalEq) {

var currTotalEq = _C(exchange.GetAccount).Balance // equity

if (currTotalEq) {

totalEq = currTotalEq

_G("totalEq", currTotalEq)

} else {

throw "failed to obtain initial interest"

}

} else {

totalEq = recoverTotalEq

}

} else {

totalEq = _C(exchange.GetAccount).Balance

}

while (1) {

if (openPrice == 0) {

// Update account information and calculate profits

var nowAcc = _C(exchange.GetAccount)

nowEq = IsVirtual() ? nowAcc.Balance : nowAcc.Balance // equity

LogProfit(nowEq - totalEq, nowAcc)

var direction = Math.floor((Math.random()*100)+1) // 1~50 , 51~100

var depth = _C(exchange.GetDepth)

if (depth.Asks.length <= 2 || depth.Bids.length <= 2) {

Sleep(1000)

continue

}

if (direction > 50) {

// long

openPrice = depth.Bids[1].Price

exchange.SetDirection("buy")

exchange.Buy(Math.abs(openPrice) + slidePrice, amount * ratio)

} else {

// short

openPrice = -depth.Asks[1].Price

exchange.SetDirection("sell")

exchange.Sell(Math.abs(openPrice) - slidePrice, amount * ratio)

}

Log("place", direction > 50 ? "buying order" : "selling order", ", price:", Math.abs(openPrice))

continue

}

var orders = _C(exchange.GetOrders)

if (orders.length == 0) {

var pos = _C(exchange.GetPosition)

if (pos.length == 0) {

openPrice = 0

continue

}

// Test for closing the position

while (1) {

var depth = _C(exchange.GetDepth)

if (depth.Asks.length <= 2 || depth.Bids.length <= 2) {

Sleep(1000)

continue

}

var stopLossPrice = openPrice > 0 ? Math.abs(openPrice) - stopLoss : Math.abs(openPrice) + stopLoss

var stopProfitPrice = openPrice > 0 ? Math.abs(openPrice) + stopProfit : Math.abs(openPrice) - stopProfit

var winOrLoss = 0 // 1 win , -1 loss

// drawing the line

$.PlotLine("bid", depth.Bids[0].Price)

$.PlotLine("ask", depth.Asks[0].Price)

// stop loss

if (openPrice > 0 && depth.Bids[0].Price < stopLossPrice) {

exchange.SetDirection("closebuy")

exchange.Sell(depth.Bids[0].Price - slidePrice, pos[0].Amount)

winOrLoss = -1

} else if (openPrice < 0 && depth.Asks[0].Price > stopLossPrice) {

exchange.SetDirection("closesell")

exchange.Buy(depth.Asks[0].Price + slidePrice, pos[0].Amount)

winOrLoss = -1

}

// stop profit

if (openPrice > 0 && depth.Bids[0].Price > stopProfitPrice) {

exchange.SetDirection("closebuy")

exchange.Sell(depth.Bids[0].Price - slidePrice, pos[0].Amount)

winOrLoss = 1

} else if (openPrice < 0 && depth.Asks[0].Price < stopProfitPrice) {

exchange.SetDirection("closesell")

exchange.Buy(depth.Asks[0].Price + slidePrice, pos[0].Amount)

winOrLoss = 1

}

// Test the pending orders

Sleep(2000)

var orders = _C(exchange.GetOrders)

if (orders.length == 0) {

pos = _C(exchange.GetPosition)

if (pos.length == 0) {

if (winOrLoss == -1) {

ratio++

} else if (winOrLoss == 1) {

ratio = 1

}

break

}

} else {

// cancel pending orders

cancelAll()

Sleep(2000)

pos = _C(exchange.GetPosition)

// update the position after cancellation, and check it again

if (pos.length == 0) {

if (winOrLoss == -1) {

ratio++

} else if (winOrLoss == 1) {

ratio = 1

}

break

}

}

var tbl = {

"type" : "table",

"title" : "info",

"cols" : ["totalEq", "nowEq", "openPrice", "bid1Price", "ask1Price", "ratio", "pos.length"],

"rows" : [],

}

tbl.rows.push([totalEq, nowEq, Math.abs(openPrice), depth.Bids[0].Price, depth.Asks[0].Price, ratio, pos.length])

tbl.rows.push(["pos", "type", "amount", "price", "--", "--", "--"])

for (var j = 0 ; j < pos.length ; j++) {

tbl.rows.push([j, pos[j].Type, pos[j].Amount, pos[j].Price, "--", "--", "--"])

}

LogStatus(_D(), "\n", "`" + JSON.stringify(tbl) + "`")

}

} else {

// cancel the pending orders

// reset openPrice

cancelAll()

openPrice = 0

}

Sleep(1000)

}

}

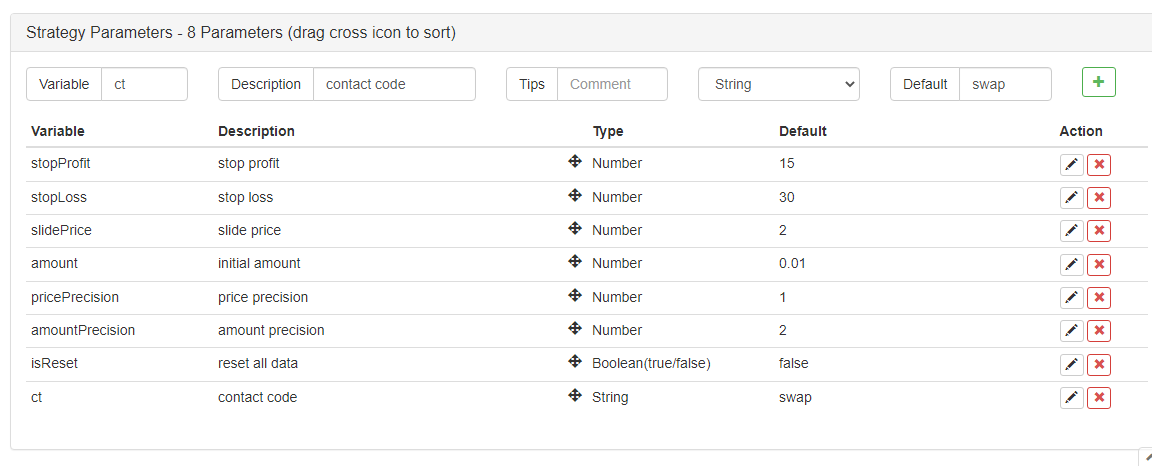

কৌশলগত পরামিতি:

ওহ হ্যাঁ! কৌশলটির একটি নাম দরকার, আসুন এটিকে "আকার অনুমান করুন (ডিওয়াইডিএক্স সংস্করণ) " বলি।

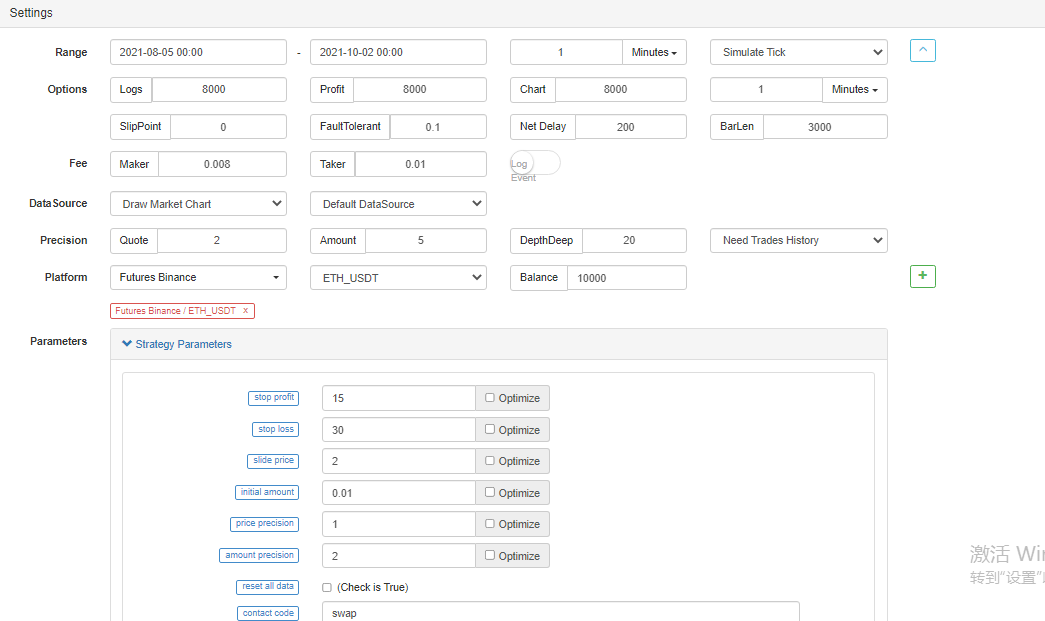

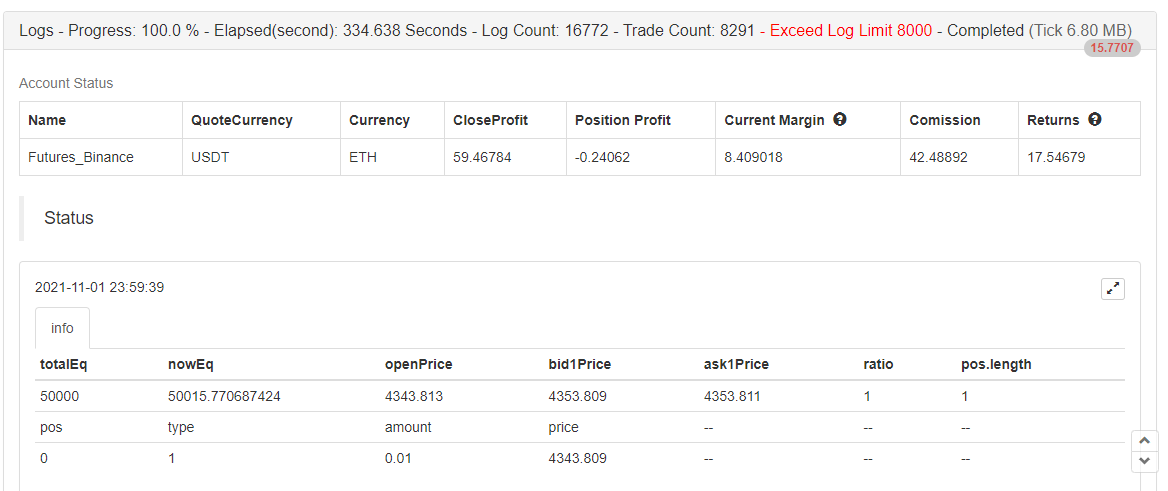

ব্যাকটেস্ট

ব্যাকটেস্টিং শুধুমাত্র রেফারেন্সের জন্য, >_

ব্যাকটেস্ট শেষ, কোন বাগ নেই।

এই কৌশল শুধুমাত্র শেখার এবং রেফারেন্সের জন্য ব্যবহার করা হয়, বাস্তব বট এটি ব্যবহার করবেন না!

- ক্রিপ্টোকারেন্সি মার্কেটে মৌলিক বিশ্লেষণের পরিমাণ নির্ধারণঃ তথ্য নিজের জন্য কথা বলতে দিন!

- মুদ্রাচক্রের মৌলিক পরিমাণগত গবেষণা - এখন আর সব ধরনের ধাঁধাবাদী শিক্ষকদের বিশ্বাস করা বন্ধ করুন, তথ্য অবজেক্টিভভাবে কথা বলছে!

- কোয়ালিফাইড লেনদেনের জন্য একটি অপরিহার্য সরঞ্জাম - উদ্ভাবক কোয়ালিফাইড ডেটা এক্সপ্লোরার মডিউল

- সবকিছু আয়ত্ত করা - এফএমজেড ট্রেডিং টার্মিনালের নতুন সংস্করণে ভূমিকা (টিআরবি আর্বিট্রেজ সোর্স কোড সহ)

- এফএমজেডের নতুন ট্রেডিং টার্মিনালের সাথে পরিচিত হোন (ট্র্যাফিক কোড সহ)

- FMZ Quant: ক্রিপ্টোকারেন্সি মার্কেটে সাধারণ প্রয়োজনীয়তা ডিজাইন উদাহরণগুলির বিশ্লেষণ (II)

- কিভাবে 80 লাইন কোডে একটি উচ্চ ফ্রিকোয়েন্সি কৌশল সঙ্গে মস্তিষ্কহীন বিক্রয় বট শোষণ

- এফএমজেড পরিমাণঃ ক্রিপ্টোকারেন্সি বাজারের সাধারণ চাহিদা ডিজাইন উদাহরণ বিশ্লেষণ (২)

- ৮০ লাইন কোডের উচ্চ-প্রবাহের কৌশল ব্যবহার করে মস্তিষ্কবিহীন রোবটকে কীভাবে বিক্রি করা যায়

- FMZ Quant: ক্রিপ্টোকারেন্সি মার্কেটে সাধারণ প্রয়োজনীয়তা ডিজাইন উদাহরণগুলির বিশ্লেষণ (I)

- এফএমজেড কোয়াটিফিকেশনঃ ক্রিপ্টোকারেন্সি মার্কেটের সাধারণ চাহিদা ডিজাইন উদাহরণ বিশ্লেষণ