Mit dem alten Weiß JavaScript spielen - einen kleinen Partner schaffen, der einkaufen und verkaufen kann (4) und ihm ein paar einfache Dinge beibringen

Schriftsteller:Kleine Träume, Erstellt: 2017-03-08 11:52:02, aktualisiert: 2017-10-11 10:37:23Mit dem alten Weiß spielt man mit dem JavaScript-Macher und schafft einen kleinen Partner, der einkaufen und verkaufen kann.

Er lernt einfaches Wissen (Gleichlinienanwendungen)

In der letzten Kapitel haben wir einige interessante Codes im Sandbox-System geübt, und heute müssen wir unsere Programme aus der Sandbox holen, um die Welt zu sehen, und natürlich müssen wir ihnen etwas beibringen!

-

Einheitliche Kauf- und Verkaufslogik

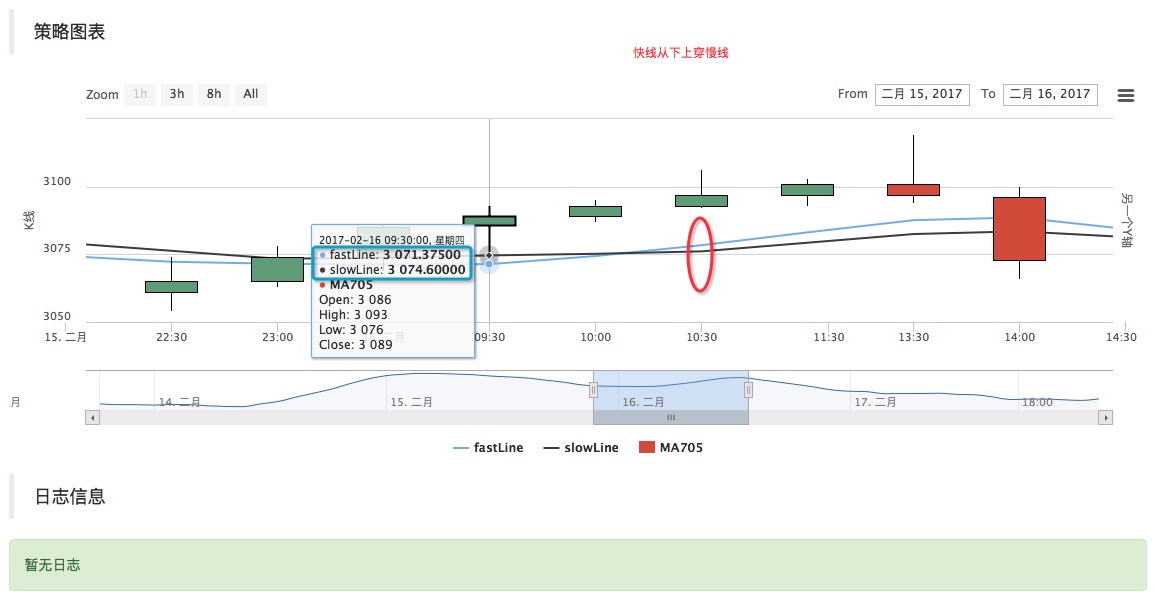

Diese Kauf- und Verkaufslogik ist wahrscheinlich die einfachste und grundlegendste Strategie in der Welt des programmatisierten Handels, der quantitativen Handel. Das heißt: ein Kennzeichen, z. B. MA705 Vertrag (Methanol-Vertrag) Zyklus ist der Durchschnitt von 10 Bar (K-Linien-Säulen) und der Zyklus ist der Durchschnitt von 8 Bar, der Unterschied des Vergleichs.

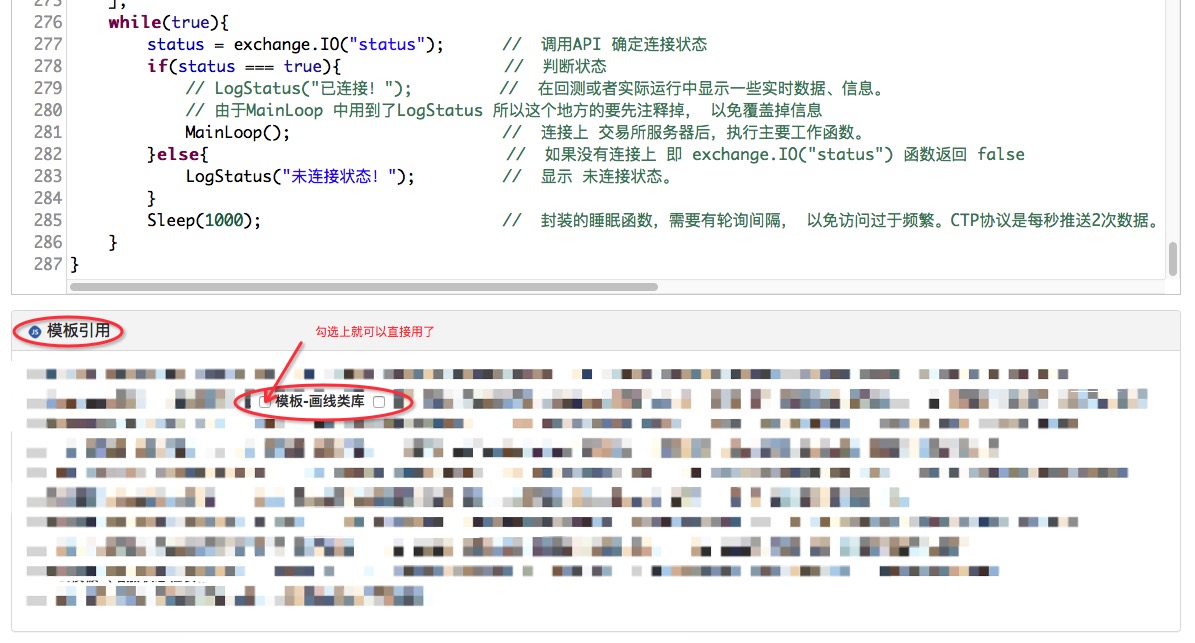

Die Adresse dieses Bildmodells ist:https://www.fmz.com/strategy/27293

Die Kopie erscheint dann in der Referenzzappe, direkt zu verwenden, und nicht vergessen, sie zu ticken.

Der Code ist einfach:

var PreRecordTime = 0; var isFirst = true; function MainLoop(){ var info = exchange.SetContractType("MA705"); if(!info){ return; } var records = exchange.GetRecords(); if(!records || records.length < 10){ // 因为长周期 为10 所以要计算10个Bar的均值, 必须要有10个K线才能计算出来。 return; // 不满足的情况,返回,重新来。 } if(isFirst){ PreRecordTime = records[records.length - 1].Time; isFirst = false; } var fastLine = TA.MA(records, 8); // 均线指标,计算出给定 的K线数据 8个 Bar 的均值, 按顺序压入数组(随时间序列,和K线Bar时间同步形成一条线,所以叫快线) 返回这个数组给变量fastLine var slowLine = TA.MA(records, 10); // 同上 区别是10个Bar ,所以叫慢线(周期大,均值变化的慢)。 var current_fastLine = fastLine[fastLine.length - 1]; // 这个数组的 倒数第一个索引 fastLine.length - 1 ,也就是表示的 快线的最后一个值 ,就是当前K线 对应的 快线均值。 var current_slowLine = slowLine[slowLine.length - 1]; // 同上 if(PreRecordTime !== records[records.length - 1].Time){ // K线更新了才确定当前最新的前一根Bar $.PlotLine("fastLine", fastLine[fastLine.length - 2], PreRecordTime); // 引用了模板,可以直接使用这个模块导出函数 画线。(其实就是封装成 模块了) $.PlotLine("slowLine", slowLine[slowLine.length - 2], PreRecordTime); // 同上 画指标线 PreRecordTime = records[records.length - 1].Time; $.PlotLine("fastLine", current_fastLine, records[records.length - 1].Time); $.PlotLine("slowLine", current_slowLine, records[records.length - 1].Time); }else{ $.PlotLine("fastLine", current_fastLine, records[records.length - 1].Time); // 当前的不停在变动。 $.PlotLine("slowLine", current_slowLine, records[records.length - 1].Time); } $.PlotRecords(records, "MA705"); // 画K线 } var cfg = $.GetCfg(); function main() { var status = null; cfg.yAxis = [{ title: {text: 'K线'}, //标题 style: {color: '#4572A7'}, //样式 opposite: false //生成右边Y轴 }, { title:{text: "另一个Y轴"}, opposite: true //生成右边Y轴 ceshi } ]; while(true){ status = exchange.IO("status"); // 调用API 确定连接状态 if(status === true){ // 判断状态 // LogStatus("已连接!"); // 在回测或者实际运行中显示一些实时数据、信息。 // 由于MainLoop 中用到了LogStatus 所以这个地方的要先注释掉, 以免覆盖掉信息 MainLoop(); // 连接上 交易所服务器后,执行主要工作函数。 }else{ // 如果没有连接上 即 exchange.IO("status") 函数返回 false LogStatus("未连接状态!"); // 显示 未连接状态。 } Sleep(1000); // 封装的睡眠函数,需要有轮询间隔, 以免访问过于频繁。CTP协议是每秒推送2次数据。 } }Das ist ein sehr schwieriges Problem, aber es ist nicht einfach, es zu lösen.

Man kann sehen, dass bei lokalen Anstiegen eine schnelle Linie von unten durch eine langsame Linie verläuft. Wie wird diese Form im Code beschrieben?

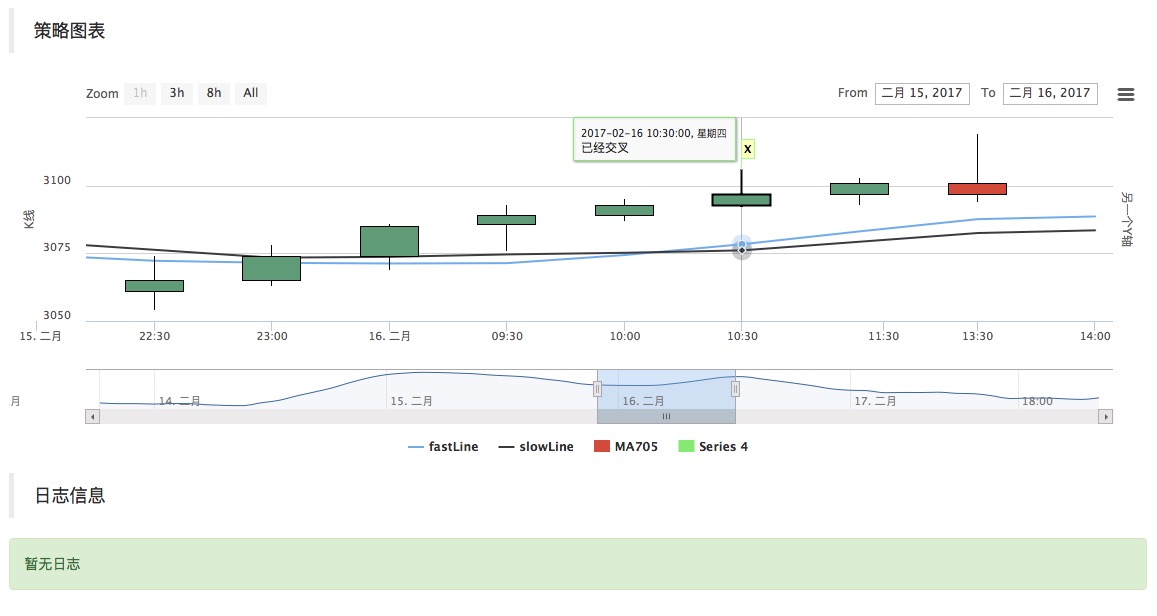

// 判断指标形态 if(fastLine.length > 3 && slowLine.length > 3 && fastLine[fastLine.length - 3] < slowLine[slowLine.length - 3] && fastLine[fastLine.length - 2] > slowLine[slowLine.length - 2]){ $.PlotFlag(records[records.length - 2].Time, '已经交叉', 'X'); // 在图表上打个标记 }

Die schnelle Linie führt von oben nach unten über die langsame Linie. Wir fügen dem Programm einen Codebeitrag hinzu, der dieser Logik entspricht.

-

Lehrer lernen, wie man reibungslos handelt

Hier benutzen wir ein anderes JavaScript-Modul, das wir direkt in unsere Programme integrieren. Die MA705-Konvention (Methanol) wird weiterhin als Handelszeichen verwendet.

// --------交易模块-------------

var Interval = 500;

var SlideTick = 1;

var RiskControl = false;

var __orderCount = 0

var __orderDay = 0

function CanTrade(tradeAmount) {

if (!RiskControl) {

return true

}

if (typeof(tradeAmount) == 'number' && tradeAmount > MaxTradeAmount) {

Log("风控模块限制, 超过最大下单量", MaxTradeAmount, "#ff0000 @");

throw "中断执行"

return false;

}

var nowDay = new Date().getDate();

if (nowDay != __orderDay) {

__orderDay = nowDay;

__orderCount = 0;

}

__orderCount++;

if (__orderCount > MaxTrade) {

Log("风控模块限制, 不可交易, 超过最大下单次数", MaxTrade, "#ff0000 @");

throw "中断执行"

return false;

}

return true;

}

function init() {

if (typeof(SlideTick) === 'undefined') {

SlideTick = 1;

} else {

SlideTick = parseInt(SlideTick);

}

Log("商品交易类库加载成功");

}

function GetPosition(e, contractType, direction, positions) {

var allCost = 0;

var allAmount = 0;

var allProfit = 0;

var allFrozen = 0;

var posMargin = 0;

if (typeof(positions) === 'undefined' || !positions) {

positions = _C(e.GetPosition);

}

for (var i = 0; i < positions.length; i++) {

if (positions[i].ContractType == contractType &&

(((positions[i].Type == PD_LONG || positions[i].Type == PD_LONG_YD) && direction == PD_LONG) || ((positions[i].Type == PD_SHORT || positions[i].Type == PD_SHORT_YD) && direction == PD_SHORT))

) {

posMargin = positions[i].MarginLevel;

allCost += (positions[i].Price * positions[i].Amount);

allAmount += positions[i].Amount;

allProfit += positions[i].Profit;

allFrozen += positions[i].FrozenAmount;

}

}

if (allAmount === 0) {

return null;

}

return {

MarginLevel: posMargin,

FrozenAmount: allFrozen,

Price: _N(allCost / allAmount),

Amount: allAmount,

Profit: allProfit,

Type: direction,

ContractType: contractType

};

}

function Open(e, contractType, direction, opAmount) {

var initPosition = GetPosition(e, contractType, direction);

var isFirst = true;

var initAmount = initPosition ? initPosition.Amount : 0;

var positionNow = initPosition;

while (true) {

var needOpen = opAmount;

if (isFirst) {

isFirst = false;

} else {

positionNow = GetPosition(e, contractType, direction);

if (positionNow) {

needOpen = opAmount - (positionNow.Amount - initAmount);

}

}

var insDetail = _C(e.SetContractType, contractType);

//Log("初始持仓", initAmount, "当前持仓", positionNow, "需要加仓", needOpen);

if (needOpen < insDetail.MinLimitOrderVolume) {

break;

}

if (!CanTrade(opAmount)) {

break;

}

var depth = _C(e.GetDepth);

var amount = Math.min(insDetail.MaxLimitOrderVolume, needOpen);

e.SetDirection(direction == PD_LONG ? "buy" : "sell");

var orderId;

if (direction == PD_LONG) {

orderId = e.Buy(depth.Asks[0].Price + (insDetail.PriceTick * SlideTick), Math.min(amount, depth.Asks[0].Amount), contractType, 'Ask', depth.Asks[0]);

} else {

orderId = e.Sell(depth.Bids[0].Price - (insDetail.PriceTick * SlideTick), Math.min(amount, depth.Bids[0].Amount), contractType, 'Bid', depth.Bids[0]);

}

// CancelPendingOrders

while (true) {

Sleep(Interval);

var orders = _C(e.GetOrders);

if (orders.length === 0) {

break;

}

for (var j = 0; j < orders.length; j++) {

e.CancelOrder(orders[j].Id);

if (j < (orders.length - 1)) {

Sleep(Interval);

}

}

}

}

var ret = {

price: 0,

amount: 0,

position: positionNow

};

if (!positionNow) {

return ret;

}

if (!initPosition) {

ret.price = positionNow.Price;

ret.amount = positionNow.Amount;

} else {

ret.amount = positionNow.Amount - initPosition.Amount;

ret.price = _N(((positionNow.Price * positionNow.Amount) - (initPosition.Price * initPosition.Amount)) / ret.amount);

}

return ret;

}

function Cover(e, contractType) {

var insDetail = _C(e.SetContractType, contractType);

while (true) {

var n = 0;

var opAmount = 0;

var positions = _C(e.GetPosition);

for (var i = 0; i < positions.length; i++) {

if (positions[i].ContractType != contractType) {

continue;

}

var amount = Math.min(insDetail.MaxLimitOrderVolume, positions[i].Amount);

var depth;

if (positions[i].Type == PD_LONG || positions[i].Type == PD_LONG_YD) {

depth = _C(e.GetDepth);

opAmount = Math.min(amount, depth.Bids[0].Amount);

if (!CanTrade(opAmount)) {

return;

}

e.SetDirection(positions[i].Type == PD_LONG ? "closebuy_today" : "closebuy");

e.Sell(depth.Bids[0].Price - (insDetail.PriceTick * SlideTick), opAmount, contractType, positions[i].Type == PD_LONG ? "平今" : "平昨", 'Bid', depth.Bids[0]);

n++;

} else if (positions[i].Type == PD_SHORT || positions[i].Type == PD_SHORT_YD) {

depth = _C(e.GetDepth);

opAmount = Math.min(amount, depth.Asks[0].Amount);

if (!CanTrade(opAmount)) {

return;

}

e.SetDirection(positions[i].Type == PD_SHORT ? "closesell_today" : "closesell");

e.Buy(depth.Asks[0].Price + (insDetail.PriceTick * SlideTick), opAmount, contractType, positions[i].Type == PD_SHORT ? "平今" : "平昨", 'Ask', depth.Asks[0]);

n++;

}

}

if (n === 0) {

break;

}

while (true) {

Sleep(Interval);

var orders = _C(e.GetOrders);

if (orders.length === 0) {

break;

}

for (var j = 0; j < orders.length; j++) {

e.CancelOrder(orders[j].Id);

if (j < (orders.length - 1)) {

Sleep(Interval);

}

}

}

}

}

var PositionManager = (function() {

function PositionManager(e) {

if (typeof(e) === 'undefined') {

e = exchange;

}

if (e.GetName() !== 'Futures_CTP') {

throw 'Only support CTP';

}

this.e = e;

this.account = null;

}

// Get Cache

PositionManager.prototype.Account = function() {

if (!this.account) {

this.account = _C(this.e.GetAccount);

}

return this.account;

};

PositionManager.prototype.GetAccount = function(getTable) {

this.account = _C(this.e.GetAccount);

if (typeof(getTable) !== 'undefined' && getTable) {

return AccountToTable(this.e.GetRawJSON())

}

return this.account;

};

PositionManager.prototype.GetPosition = function(contractType, direction, positions) {

return GetPosition(this.e, contractType, direction, positions);

};

PositionManager.prototype.OpenLong = function(contractType, shares) {

if (!this.account) {

this.account = _C(this.e.GetAccount);

}

return Open(this.e, contractType, PD_LONG, shares);

};

PositionManager.prototype.OpenShort = function(contractType, shares) {

if (!this.account) {

this.account = _C(this.e.GetAccount);

}

return Open(this.e, contractType, PD_SHORT, shares);

};

PositionManager.prototype.Cover = function(contractType) {

if (!this.account) {

this.account = _C(this.e.GetAccount);

}

return Cover(this.e, contractType);

};

PositionManager.prototype.CoverAll = function() {

if (!this.account) {

this.account = _C(this.e.GetAccount);

}

while (true) {

var positions = _C(this.e.GetPosition)

if (positions.length == 0) {

break

}

for (var i = 0; i < positions.length; i++) {

// Cover Hedge Position First

if (positions[i].ContractType.indexOf('&') != -1) {

Cover(this.e, positions[i].ContractType)

Sleep(1000)

}

}

for (var i = 0; i < positions.length; i++) {

if (positions[i].ContractType.indexOf('&') == -1) {

Cover(this.e, positions[i].ContractType)

Sleep(1000)

}

}

}

};

PositionManager.prototype.Profit = function(contractType) {

var accountNow = _C(this.e.GetAccount);

return _N(accountNow.Balance - this.account.Balance);

};

return PositionManager;

})();

$.NewPositionManager = function(e) {

return new PositionManager(e);

};

// Via: http://mt.sohu.com/20160429/n446860150.shtml

$.IsTrading = function(symbol) {

var now = new Date();

var day = now.getDay();

var hour = now.getHours();

var minute = now.getMinutes();

if (day === 0 || (day === 6 && (hour > 2 || hour == 2 && minute > 30))) {

return false;

}

symbol = symbol.replace('SPD ', '').replace('SP ', '');

var p, i, shortName = "";

for (i = 0; i < symbol.length; i++) {

var ch = symbol.charCodeAt(i);

if (ch >= 48 && ch <= 57) {

break;

}

shortName += symbol[i].toUpperCase();

}

var period = [

[9, 0, 10, 15],

[10, 30, 11, 30],

[13, 30, 15, 0]

];

if (shortName === "IH" || shortName === "IF" || shortName === "IC") {

period = [

[9, 30, 11, 30],

[13, 0, 15, 0]

];

} else if (shortName === "TF" || shortName === "T") {

period = [

[9, 15, 11, 30],

[13, 0, 15, 15]

];

}

if (day >= 1 && day <= 5) {

for (i = 0; i < period.length; i++) {

p = period[i];

if ((hour > p[0] || (hour == p[0] && minute >= p[1])) && (hour < p[2] || (hour == p[2] && minute < p[3]))) {

return true;

}

}

}

var nperiod = [

[

['AU', 'AG'],

[21, 0, 02, 30]

],

[

['CU', 'AL', 'ZN', 'PB', 'SN', 'NI'],

[21, 0, 01, 0]

],

[

['RU', 'RB', 'HC', 'BU'],

[21, 0, 23, 0]

],

[

['P', 'J', 'M', 'Y', 'A', 'B', 'JM', 'I'],

[21, 0, 23, 30]

],

[

['SR', 'CF', 'RM', 'MA', 'TA', 'ZC', 'FG', 'IO'],

[21, 0, 23, 30]

],

];

for (i = 0; i < nperiod.length; i++) {

for (var j = 0; j < nperiod[i][0].length; j++) {

if (nperiod[i][0][j] === shortName) {

p = nperiod[i][1];

var condA = hour > p[0] || (hour == p[0] && minute >= p[1]);

var condB = hour < p[2] || (hour == p[2] && minute < p[3]);

// in one day

if (p[2] >= p[0]) {

if ((day >= 1 && day <= 5) && condA && condB) {

return true;

}

} else {

if (((day >= 1 && day <= 5) && condA) || ((day >= 2 && day <= 6) && condB)) {

return true;

}

}

return false;

}

}

}

return false;

};

// --------交易模块完结----------

var PreRecordTime = 0;

var isFirst = true;

var IDLE = 0;

var OPENLONG = 1;

var COVER = 2;

var STATE = IDLE;

var InitAccount = null;

function MainLoop(){

var info = exchange.SetContractType("MA705");

if(!info){

return;

}

var records = exchange.GetRecords();

if(!records || records.length < 10){ // 因为长周期 为10 所以要计算10个Bar的均值, 必须要有10个K线才能计算出来。

return; // 不满足的情况,返回,重新来。

}

if(isFirst){

PreRecordTime = records[records.length - 1].Time;

InitAccount = exchange.GetAccount();

isFirst = false;

}

var fastLine = TA.MA(records, 5); // 均线指标,计算出给定 的K线数据 8个 Bar 的均值, 按顺序压入数组(随时间序列,和K线Bar时间同步形成一条线,所以叫快线) 返回这个数组给变量fastLine

var slowLine = TA.MA(records, 10); // 同上 区别是10个Bar ,所以叫慢线(周期大,均值变化的慢)。

var current_fastLine = fastLine[fastLine.length - 1]; // 这个数组的 倒数第一个索引 fastLine.length - 1 ,也就是表示的 快线的最后一个值 ,就是当前K线 对应的 快线均值。

var current_slowLine = slowLine[slowLine.length - 1]; // 同上

if(PreRecordTime !== records[records.length - 1].Time){ // K线更新了才确定当前最新的前一根Bar

$.PlotLine("fastLine", fastLine[fastLine.length - 2], PreRecordTime); // 引用了模板,可以直接使用这个模块导出函数 画线。(其实就是封装成 模块了)

$.PlotLine("slowLine", slowLine[slowLine.length - 2], PreRecordTime); // 同上 画指标线

PreRecordTime = records[records.length - 1].Time;

$.PlotLine("fastLine", current_fastLine, records[records.length - 1].Time);

$.PlotLine("slowLine", current_slowLine, records[records.length - 1].Time);

}else{

$.PlotLine("fastLine", current_fastLine, records[records.length - 1].Time); // 当前的不停在变动。

$.PlotLine("slowLine", current_slowLine, records[records.length - 1].Time);

}

$.PlotRecords(records, "MA705"); // 画K线

// 判断指标形态

if(STATE === IDLE && fastLine.length > 3 && slowLine.length > 3 && fastLine[fastLine.length - 3] < slowLine[slowLine.length - 3] && fastLine[fastLine.length - 2] > slowLine[slowLine.length - 2]){

P.OpenLong("MA705", 1);

STATE = OPENLONG;

$.PlotFlag(new Date().getTime(), '快线上传慢线', 'OPENLONG');

}

if(STATE === OPENLONG && fastLine[fastLine.length - 3] > slowLine[slowLine.length - 3] && fastLine[fastLine.length - 2] < slowLine[slowLine.length - 2]){

P.Cover("MA705");

STATE = COVER;

$.PlotFlag(new Date().getTime(), '快线下传慢线', 'COVER');

}

if(STATE === COVER){

var nowAccount = exchange.GetAccount();

LogProfit(nowAccount.Balance - InitAccount.Balance, nowAccount);

STATE = IDLE;

}

}

var cfg = $.GetCfg();

var P = null;

function main() {

var status = null;

P = $.NewPositionManager(exchange); // 构造一个 用于控制交易细节的对象。

cfg.yAxis = [{

title: {text: 'K线'}, //标题

style: {color: '#4572A7'}, //样式

opposite: false //生成右边Y轴

},

{

title:{text: "另一个Y轴"},

opposite: true //生成右边Y轴 ceshi

}

];

while(true){

status = exchange.IO("status"); // 调用API 确定连接状态

if(status === true){ // 判断状态

// LogStatus("已连接!"); // 在回测或者实际运行中显示一些实时数据、信息。

// 由于MainLoop 中用到了LogStatus 所以这个地方的要先注释掉, 以免覆盖掉信息

MainLoop(); // 连接上 交易所服务器后,执行主要工作函数。

}else{ // 如果没有连接上 即 exchange.IO("status") 函数返回 false

LogStatus("未连接状态!"); // 显示 未连接状态。

}

Sleep(1000); // 封装的睡眠函数,需要有轮询间隔, 以免访问过于频繁。CTP协议是每秒推送2次数据。

}

}

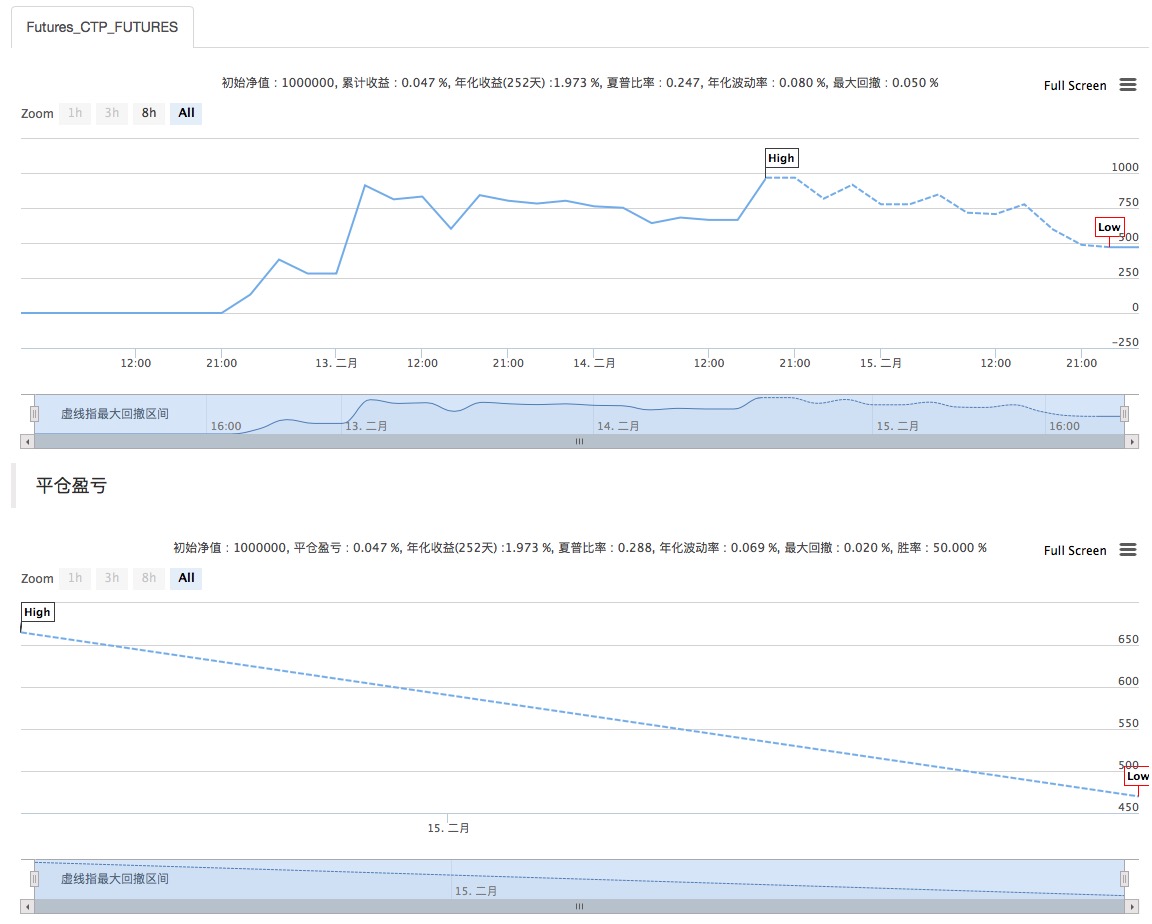

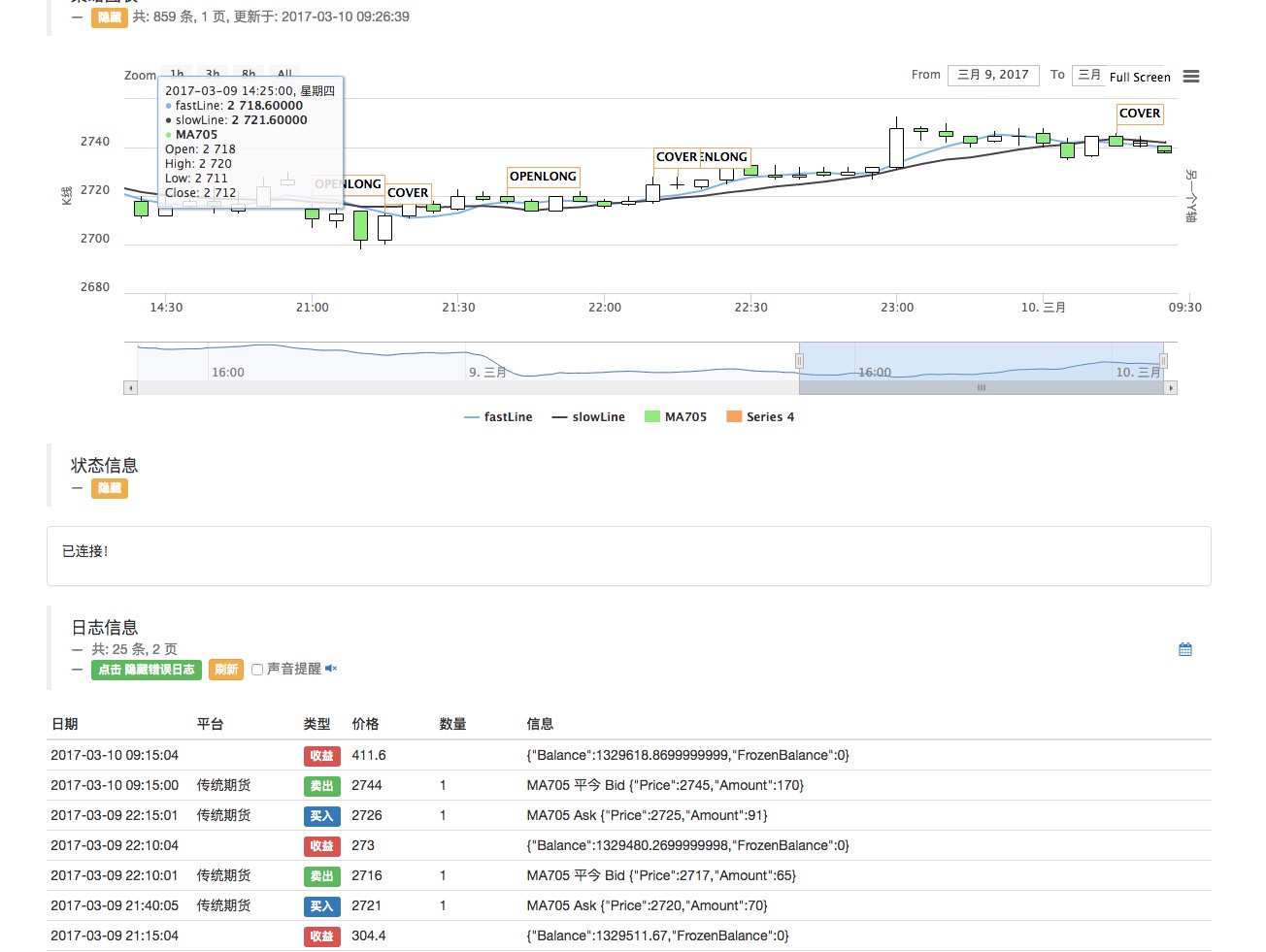

Die Sandbox wurde wie folgt gemessen:

Der Rückgang des Marktes ist sehr groß, und es ist offensichtlich, dass die Handelslogik sehr unvollkommen ist, dass die Erträge im Aufwärtstrend positiv sind, was nicht bedeutet, dass es keine Probleme gibt.

-

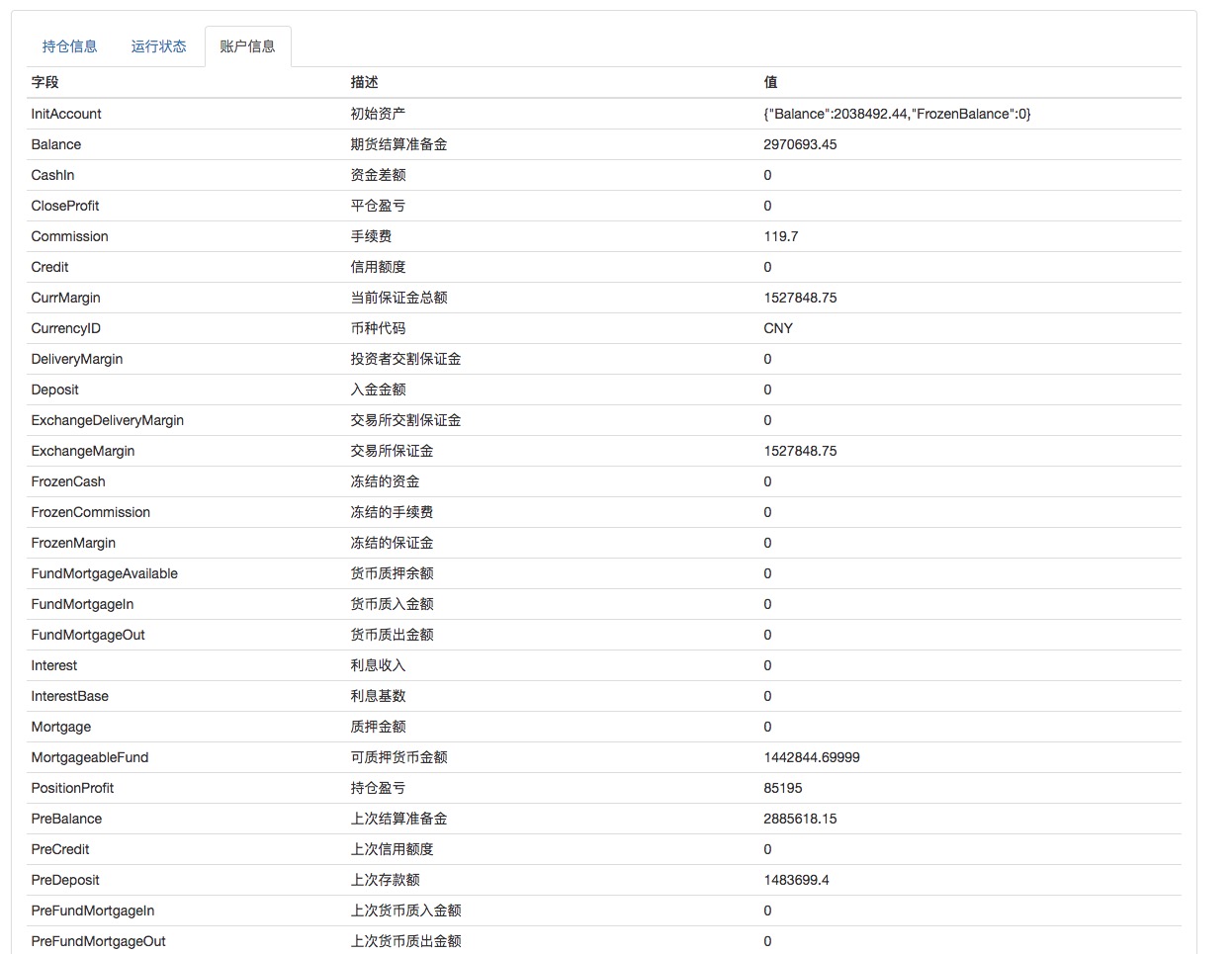

Ein Beispiel ist die Art und Weise, wie wir mit dem Simulator-Futures-Simulationskonto spielen, das wir mit Simnow-Technologie bereitstellen.

Für weitere Informationen zum Antragsformular simnow Commodity Futures können Sie sich den folgenden Beitrag ansehen:https://www.fmz.com/bbs-topic/325Die Analog-Transaktionen können direkt mit dem CTP-Protokoll programmiert werden.

Der Programm läuft eine Weile, die Strategie selbst ist demonstrativ, jeder ist nur zur Referenz, wenn es notwendig ist, können Sie auch hinzufügen Position Control, Stop Stop, Stop Loss, Burst Warning usw. (Dies hängt von der native JS-Programmiersprache ab, ist sehr frei, schreibt die Strategie Spaß).

Ich habe ein simuliertes Konto, das ich auf den Test stellen kann.

Schauen Sie sich meinen anderen Programm an, der auf einer Simulationsplatte läuft, und dieser Komplex zeigt ein bisschen:

Ich bin ein Liebhaber von JS, ich studiere JS, ich habe es gekauft, der Quellcode:https://www.fmz.com/strategy/17289

Bitte schreiben Sie mir einen E-Mail! Bitte schreiben Sie mir einen E-Mail! Bitte schreiben Sie mir einen E-Mail!

https://www.fmz.com/bbs-topic/727

Der Programmierer littleDream, ursprünglich

- Der Host Ali Linux läuft, der Host wird neu gestartet, wie findet man den ursprünglichen Host zurück?

- Wertschöpfungsinvestitionen definieren Risiko anders, als man es sich vorstellt.

- Ich möchte fragen, welche Plattformen für virtuelle Währungen unterstützt werden, und welche Währungen für den Handel.

- Null- und Negativmarkt

- Mit dem alten Weißen JavaScript spielen - ein Kauf- und Verkaufspartner erstellen (7) nützliches Tool, das man wissen muss, warum es nützlich ist!

- Spielen Sie mit Old White JavaScript - Erstellen Sie einen kleinen Partner, der einkaufen und verkaufen kann und entwickeln Sie Tools, die für Roboter verwendet werden

- Hochfrequenz-Handelsstrategien - Handel und Rückwärtswahl

- Ein Wahrscheinlichkeitsforscher sein - ein Dummkopf, der zufällig durchs Buch geht

- Positive Erwartungen an Wahrscheinlichkeiten, Verzögerungen und langfristige Transaktionen

- Spielen Sie mit dem alten Weißen JavaScript - Erstellen Sie einen kleinen Partner, der einkaufen und verkaufen kann.

- Spielen Sie JavaScript mit dem alten Weißen - erstellen Sie einen kleinen Partner, der einkaufen und verkaufen kann.

- Die Frage nach den zukünftigen Funktionen, bitte die Götter!

- Mit dem alten Weiß JavaScript spielen - ein Partner schaffen, der kauft und verkauft.

- Mit dem alten Weißen JavaScript spielen - ein Partner schaffen, der einkaufen und verkaufen kann.

- Geld und Kredite des Geldbanksystems

- Futures-Handel: Das Streben nach perfekter Sicherheit ist das Toxonsystem!

- Die Handelsstrategien der Spieler

- HttpQuery ist nicht in Python verfügbar.

- Was bedeutet es, dass die Chancengleichheit der Abgefallenen nicht mehr existiert?

- Einzelheiten: Die Größenbeschränkung für die Positionseinheit (Strandhandelsgesetze)