Multiple-Equilibrium-Preistrendfolge- und Umkehrhandelsstrategie

Strategieüberblick

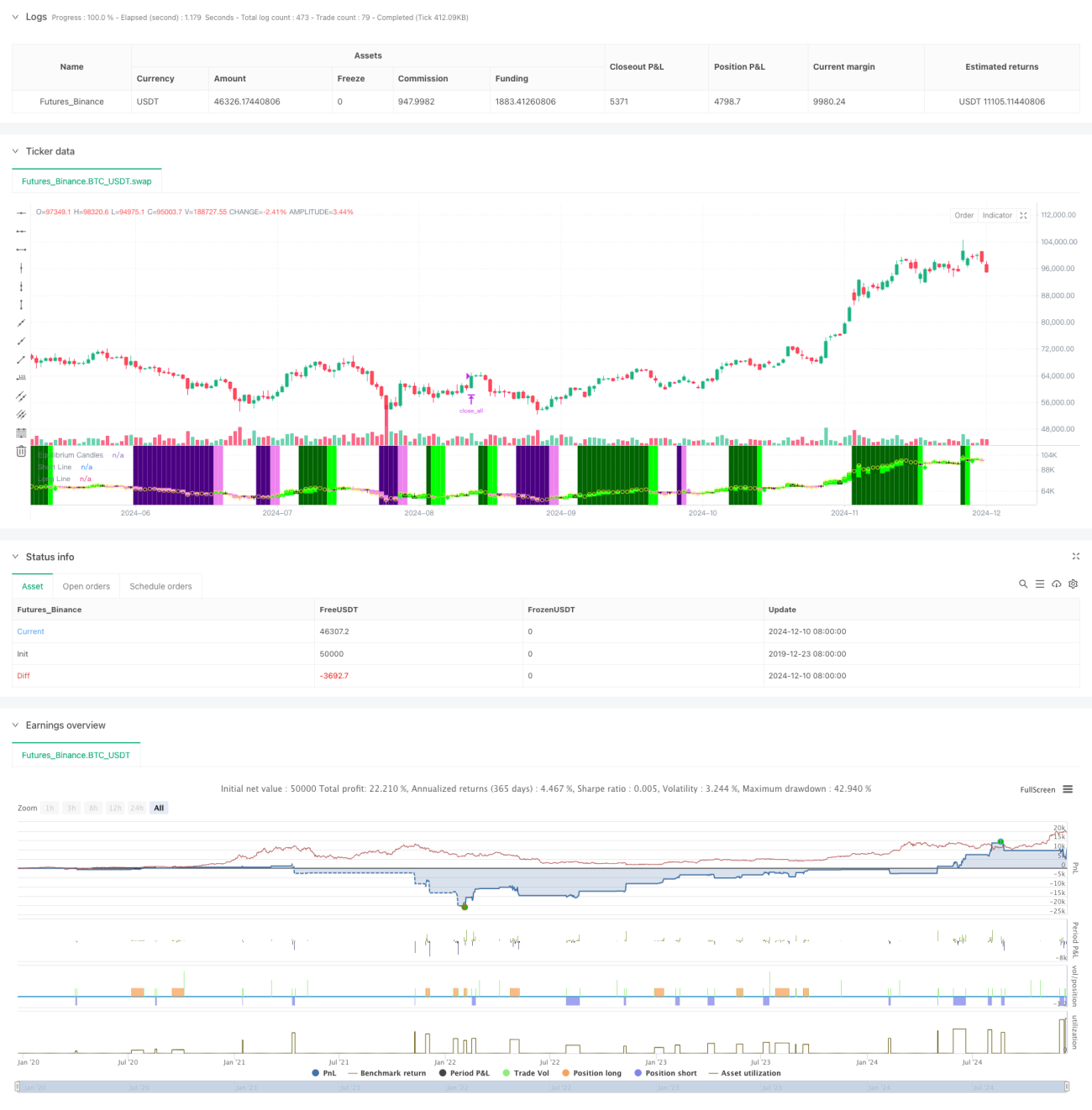

Diese Strategie ist ein Trendfolge- und Umkehrhandelssystem, das auf dem Gleichgewichtspreis basiert. Sie berechnet den Gleichgewichtspreis als Mittelwert aus dem höchsten und niedrigsten Punkt der letzten X Kerzen und bestimmt die Trendrichtung anhand der Position des Schlusskurses relativ zum Gleichgewichtspreis. Wenn der Kurs für eine festgelegte Anzahl von Kerzen kontinuierlich auf einer Seite des Gleichgewichtspreises bleibt, wird ein Trend als bestätigt angesehen. Bei der ersten Korrektur (Kurs durchbricht den Gleichgewichtspreis) wird eine Einstiegsmöglichkeit gesucht. Die Strategie kann je nach Einstellung zwischen Trendfolge- oder Umkehrmodus wählen.

Strategieprinzip

- Berechnung des Gleichgewichtspreises: Der Mittelwert aus dem Hoch- und Tiefkurs der letzten X Kerzen wird als Gleichgewichtspreis verwendet – identisch mit der Berechnungsmethode der Basislinie im Ichimoku-Kinko-Hyo.

- Trendbestimmung: Wenn der Preis für X aufeinanderfolgende Kerzen (Standard: 7) auf derselben Seite des Gleichgewichtspreises bleibt, wird ein Trend als bestätigt angesehen.

- Einstiegssignal: Das Signal wird bei der ersten Korrektur nach Trendbestätigung ausgelöst (Kurs durchbricht den Gleichgewichtspreis).

- Stop-Loss und Take-Profit: Das 60%-Quantil des ATR wird zur dynamischen Anpassung der Stop-Loss- und Take-Profit-Distanzen verwendet, was Flexibilität bei der Risikosteuerung bietet.

- Schutz vor starken Schwankungen: Wenn die Abweichung des Kurses vom Gleichgewichtspunkt ein festgelegtes ATR-Vielfaches überschreitet, wird die Position automatisch geschlossen, um größere Verluste zu verhindern.

Strategievorteile

- Hohe Anpassungsfähigkeit: Je nach Marktcharakteristik können Trendfolge- und Umkehrmodus flexibel gewechselt werden.

- Umfassende Risikokontrolle: Dynamischer ATR-Stop-Loss sowie Schutzmechanismus gegen starke Schwankungen.

- Klare Handelsregeln: Handelsignale sind eindeutig und nicht von komplexen technischen Indikatorkombinationen abhängig.

- Gute Visualisierung: Farbige Kerzen und Hintergründe bieten eine intuitive Darstellung der Marktlage.

- Automatisierungsfreundlich: Leicht an Plattformen wie MT5 anbindbar für den automatisierten Handel.

Strategierisiken

- Seitwärtsmarktrisiko: In einer range-handelnden Phase können häufige Fehlsignale auftreten.

- Slippage-Effekt: Bei starken Schwankungen kann es zu erheblichem Slippage kommen.

- Parameterempfindlichkeit: Kernparameter wie Gleichgewichtsperiode und Trendbestimmungszeitraum müssen für verschiedene Märkte sorgfältig optimiert werden.

- Marktwechselrisiko: Der Übergang von einem Trend- in einen Seitwärtsmarkt kann zu größeren Verlusten führen.

Optimierungsrichtungen

- Marktumfeld-Erkennung: Integration eines Moduls zur Beurteilung des Marktumfelds, das die Strategieparameter dynamisch an die Marktbedingungen anpasst.

- Signalfilterung: Zusätzliche Indikatoren wie Volumen oder Volatilität können zur Filterung von Fehlsignalen hinzugezogen werden.

- Positionsmanagement: Einführung komplexerer Positionsmanagementmechanismen, z. B. dynamische Anpassung basierend auf der Volatilität.

- Multi-Timeframe: Integration von Signalen mehrerer Zeitrahmen zur Steigerung der Handelsgenauigkeit.

- Handelskostenoptimierung: Optimierung der Ein- und Ausstiegszeitpunkte basierend auf den Kostencharakteristika der jeweiligen Handelsinstrumente.

Zusammenfassung

Dies ist ein gut durchdachtes Trendhandelssystem, das durch das Kernkonzept des Gleichgewichtspreises eine klare Handelslogik bietet. Die größte Stärke der Strategie liegt in ihrer Flexibilität: Sie kann sowohl für Trendfolge als auch für Umkehrhandel eingesetzt werden und verfügt über ein umfassendes Risikomanagement. Obwohl sie unter bestimmten Marktbedingungen Herausforderungen ausgesetzt sein kann, kann sie durch kontinuierliche Optimierung und flexible Anpassung in verschiedenen Marktumgebungen stabile Ergebnisse erzielen.

- 1