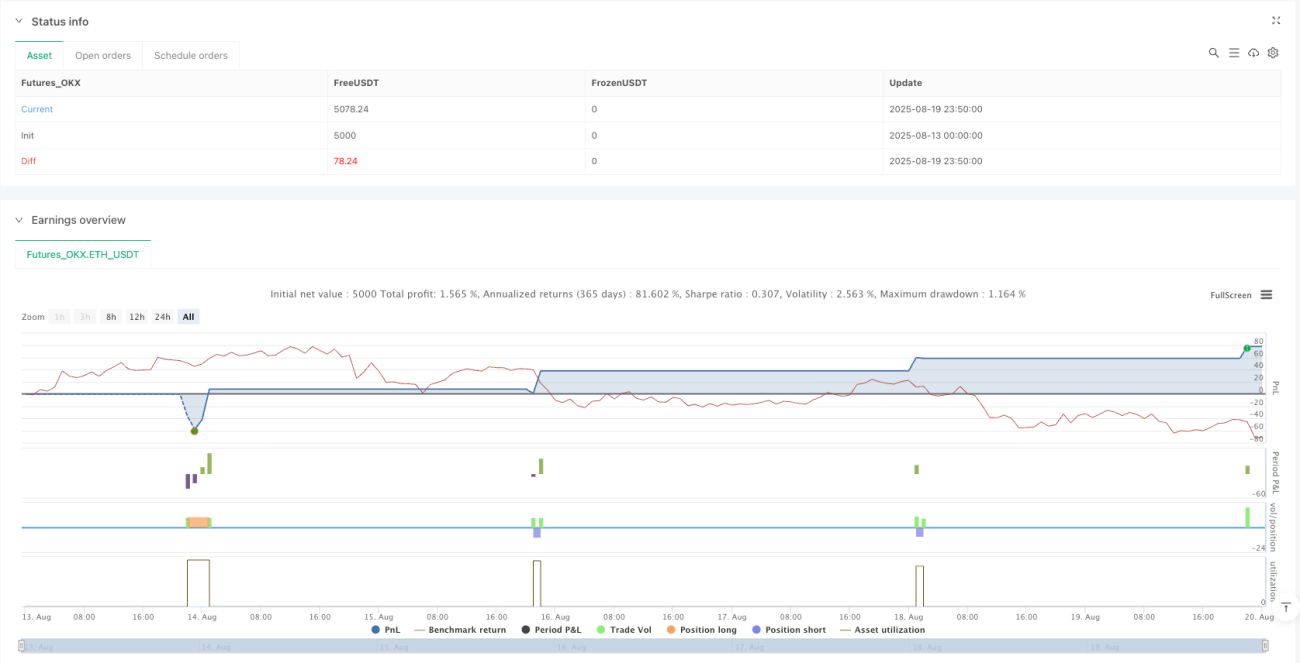

Overview

The Dynamic Time-Filtered Support-Resistance Trading System with Trailing Stop Loss is an advanced algorithmic trading strategy that combines precise entry signals, intelligent time-based filtering, and adaptive risk management. Designed for traders seeking to identify high-probability trading opportunities within specific time windows, the system employs dynamic trailing stops and partial position management techniques to optimize trading performance. The core of the strategy lies in the dynamic identification of support and resistance levels, combined with time filtering and volume confirmation to provide precise trading signals.

Strategy Principles

The fundamental principles of this strategy are built on the synergistic operation of three core elements: precise entry, optimal timing, and state management.

Entry System:

The strategy seeks reversal opportunities by dynamically identifying key price levels. It uses a configurable lookback period to calculate support and resistance zones and triggers entry signals when price interacts with these critical areas. Entry conditions include price interaction with support/resistance levels, volume confirmation, and optional trend filter confirmation. When price touches support and closes above the support buffer with above-average volume, the system generates a long signal. Similarly, when price touches resistance and closes below the resistance buffer with above-average volume, the system generates a short signal.

Time Filtering System:

The strategy implements a comprehensive time filtering system allowing traders to define optimal trading periods. This includes:

- 12-hour format trading window settings

- Multi-timezone support (UTC, EST, PST, CST)

- Day-of-week filtering (trade only weekdays, weekends, or both)

- Automatic lunch hour avoidance (typically 12:00-13:00)

- Visual time indicators (background coloring showing active/inactive trading periods)

Risk Management System:

The strategy employs a three-tier risk management approach:

- Multi-Level Take Profit System: Sets two profit targets (TP1 and TP2) with optional partial position closure at TP1

- Dynamic Trailing Stop Technology: Offers three operating modes (Conservative, Balanced, Aggressive) that automatically adjust based on current market volatility

- Intelligent Position Sizing: Allows traders to configure entry quantities and partial close quantities with clear position tracking and P&L monitoring

Strategy Advantages

Through deep analysis of the code, this strategy offers the following advantages:

-

Comprehensive Entry Signals: Combines price action, volume confirmation, and trend alignment to enhance the reliability of trading signals. The system looks for high-probability reversal points near key support and resistance levels, reducing the risk of false breakouts.

-

Flexible Time Filtering System: Allows traders to focus on optimal trading periods while avoiding low-liquidity or high-volatility market environments. This helps improve trading efficiency and reduces the likelihood of trading during unfavorable market conditions. Supports multi-timezone trading and customizable trading hour settings, making it suitable for traders worldwide.

-

Advanced Risk Management Features: Dynamic trailing stop system adjusts automatically with market volatility, helping to protect profits and let winning positions run. Multiple take-profit targets and partial closing options allow for profit locking at different price levels.

-

Comprehensive Visual Feedback: The system provides detailed chart elements and a real-time dashboard to help traders visually understand market conditions and strategy performance. Entry zone highlighting, dynamic risk/reward lines, and trailing stop visualization make the trading decision process more transparent.

-

High Customizability: From core strategy parameters to time filtering controls and risk management options, the strategy offers extensive customization capabilities to adapt to different trading styles and market conditions.

Strategy Risks

Despite its many advantages, the strategy also presents several potential risks:

-

Parameter Optimization Risk: The strategy relies on multiple parameter settings, such as lookback period, ATR multipliers, and trend filter settings. These parameters need to be carefully optimized and periodically adjusted to adapt to different market environments. Over-optimization of parameters may lead to overfitting and poor performance in future market conditions.

-

Market Condition Sensitivity: In highly volatile or low-liquidity markets, support and resistance levels may not be as reliable as expected. During extreme market conditions, prices may rapidly break through key levels, causing stop losses to be triggered.

-

Time Filtering Limitations: While time filtering can help avoid unfavorable trading periods, it may also cause the strategy to miss some high-quality trading opportunities. Markets don't always follow predetermined time patterns, especially during significant events or breaking news.

-

Trailing Stop Traps: In choppy markets, dynamic trailing stops may trigger prematurely, ending potentially profitable trades early. Different trailing stop settings (Conservative, Balanced, Aggressive) perform differently in various market environments.

-

Signal Conflicts: Mixed signals may occur when price approaches multiple support and resistance levels or when time filtering conflicts with entry signals. This may require additional judgment or more complex decision rules.

Strategy Optimization Directions

Based on the code analysis, here are potential optimization directions:

-

Adaptive Parameter Adjustment: Implement a mechanism to automatically adjust key parameters, such as lookback period and ATR multipliers, based on recent market volatility and trading performance. This can help the strategy better adapt to different market environments without manual intervention.

-

Enhanced Market Structure Analysis: Integrate more sophisticated price structure recognition methods, such as identifying higher-level support and resistance areas, recognizing trend channels, or price patterns. This can improve the quality and reliability of entry signals.

-

Optimize Time Filtering Logic: Use data analysis to identify optimal trading times for specific markets and automatically adjust trading time windows based on historical performance. Consider incorporating filtering for seasonal patterns and market-specific events like economic data releases.

-

Improved Risk Management Mechanisms: Design a smarter position sizing system that dynamically adjusts position size based on historical volatility, current market conditions, and strategy performance. Implement a tiered scaling-out strategy for profitable trades based on profit percentage.

-

Integration of Machine Learning Models: Use machine learning algorithms to predict the reliability of support and resistance levels or estimate the probability of success for entry signals under specific market conditions. This can help filter out potentially low-quality trading signals.

Summary

The Dynamic Time-Filtered Support-Resistance Trading System with Trailing Stop Loss is a comprehensive trading strategy that combines precise entry signals, intelligent time filtering, and adaptive risk management. It works by seeking high-probability reversal opportunities at key support and resistance levels while using time filtering and volume confirmation to enhance trade quality.

The strategy's main strengths lie in its comprehensive time filtering system, dynamic trailing stop technology, and highly visual user interface. These features together create a powerful and flexible trading tool suitable for various market conditions and trading styles.

However, to fully leverage the potential of this strategy, traders need to carefully optimize parameters, understand its performance characteristics in different market environments, and potentially customize it for specific markets and personal trading goals. By implementing the suggested optimization measures, the strategy's performance and robustness can be further enhanced, providing traders with a more reliable tool for market analysis and trade execution.

- 1