Balancing listing strategies with teaching strategies

Author: The Little Dream, Created: 2020-09-02 17:05:25, Updated: 2023-09-27 19:40:10

Balancing listing strategies with teaching strategies

The essence of the strategy described here is a dynamic balancing strategy, which always balances the value of the coin to the value of the coin. Although designed to be pre-listed, the strategy logic is very simple. The main purpose of writing this strategy is to show all aspects of the strategy design.

-

Strategic logical wrapping Wrapping together some data, mark variables, and strategy logic at run time ("wrapping into objects").

-

Code that handles initialization tasks Initial account information is recorded at the initial run to be used for earnings calculations and whether data is recovered at the initial run based on parameter selection.

-

The code for strategic interaction processing A simple pause, continuous interaction is designed.

-

Code for the Strategic Benefit Calculation The earnings are calculated using the coin-bit method.

-

Key data persistence mechanisms in the strategy Mechanisms for designing data recovery

-

The code that shows the policy processing information The status bar data is displayed.

The Strategy Code

var Shannon = {

// member

e : exchanges[0],

arrPlanOrders : [],

distance : BalanceDistance,

account : null,

ticker : null,

initAccount : null,

isAskPending : false,

isBidPending : false,

// function

CancelAllOrders : function (e) {

while(true) {

var orders = _C(e.GetOrders)

if(orders.length == 0) {

return

}

Sleep(500)

for(var i = 0; i < orders.length; i++) {

e.CancelOrder(orders[i].Id, orders[i])

Sleep(500)

}

}

},

Balance : function () {

if (this.arrPlanOrders.length == 0) {

this.CancelAllOrders(this.e)

var acc = _C(this.e.GetAccount)

this.account = acc

var askPendingPrice = (this.distance + acc.Balance) / acc.Stocks

var bidPendingPrice = (acc.Balance - this.distance) / acc.Stocks

var askPendingAmount = this.distance / 2 / askPendingPrice

var bidPendingAmount = this.distance / 2 / bidPendingPrice

this.arrPlanOrders.push({tradeType : "ask", price : askPendingPrice, amount : askPendingAmount})

this.arrPlanOrders.push({tradeType : "bid", price : bidPendingPrice, amount : bidPendingAmount})

} else if(this.isAskPending == false && this.isBidPending == false) {

for(var i = 0; i < this.arrPlanOrders.length; i++) {

var tradeFun = this.arrPlanOrders[i].tradeType == "ask" ? this.e.Sell : this.e.Buy

var id = tradeFun(this.arrPlanOrders[i].price, this.arrPlanOrders[i].amount)

if(id) {

this.isAskPending = this.arrPlanOrders[i].tradeType == "ask" ? true : this.isAskPending

this.isBidPending = this.arrPlanOrders[i].tradeType == "bid" ? true : this.isBidPending

} else {

Log("挂单失败,清理!")

this.CancelAllOrders(this.e)

return

}

}

}

if(this.isBidPending || this.isAskPending) {

var orders = _C(this.e.GetOrders)

Sleep(1000)

var ticker = _C(this.e.GetTicker)

this.ticker = ticker

if(this.isAskPending) {

var isFoundAsk = false

for (var i = 0; i < orders.length; i++) {

if(orders[i].Type == ORDER_TYPE_SELL) {

isFoundAsk = true

}

}

if(!isFoundAsk) {

Log("卖单成交,撤销订单,重置")

this.CancelAllOrders(this.e)

this.arrPlanOrders = []

this.isAskPending = false

this.isBidPending = false

LogProfit(this.CalcProfit(ticker))

return

}

}

if(this.isBidPending) {

var isFoundBid = false

for(var i = 0; i < orders.length; i++) {

if(orders[i].Type == ORDER_TYPE_BUY) {

isFoundBid = true

}

}

if(!isFoundBid) {

Log("买单成交,撤销订单,重置")

this.CancelAllOrders(this.e)

this.arrPlanOrders = []

this.isAskPending = false

this.isBidPending = false

LogProfit(this.CalcProfit(ticker))

return

}

}

}

},

ShowTab : function() {

var tblPlanOrders = {

type : "table",

title : "计划挂单",

cols : ["方向", "价格", "数量"],

rows : []

}

for(var i = 0; i < this.arrPlanOrders.length; i++) {

tblPlanOrders.rows.push([this.arrPlanOrders[i].tradeType, this.arrPlanOrders[i].price, this.arrPlanOrders[i].amount])

}

var tblAcc = {

type : "table",

title : "账户信息",

cols : ["type", "Stocks", "FrozenStocks", "Balance", "FrozenBalance"],

rows : []

}

tblAcc.rows.push(["初始", this.initAccount.Stocks, this.initAccount.FrozenStocks, this.initAccount.Balance, this.initAccount.FrozenBalance])

tblAcc.rows.push(["当前", this.account.Stocks, this.account.FrozenStocks, this.account.Balance, this.account.FrozenBalance])

return "时间:" + _D() + "\n `" + JSON.stringify([tblPlanOrders, tblAcc]) + "`" + "\n" + "ticker:" + JSON.stringify(this.ticker)

},

CalcProfit : function(ticker) {

var acc = _C(this.e.GetAccount)

this.account = acc

return (this.account.Balance - this.initAccount.Balance) + (this.account.Stocks - this.initAccount.Stocks) * ticker.Last

},

Init : function() {

this.initAccount = _C(this.e.GetAccount)

if(IsReset) {

var acc = _G("account")

if(acc) {

this.initAccount = acc

} else {

Log("恢复初始账户信息失败!以初始状态运行!")

_G("account", this.initAccount)

}

} else {

_G("account", this.initAccount)

LogReset(1)

LogProfitReset()

}

},

Exit : function() {

Log("停止前,取消所有挂单...")

this.CancelAllOrders(this.e)

}

}

function main() {

// 初始化

Shannon.Init()

// 主循环

while(true) {

Shannon.Balance()

LogStatus(Shannon.ShowTab())

// 交互

var cmd = GetCommand()

if(cmd) {

if(cmd == "stop") {

while(true) {

LogStatus("暂停", Shannon.ShowTab())

cmd = GetCommand()

if(cmd) {

if(cmd == "continue") {

break

}

}

Sleep(1000)

}

}

}

Sleep(5000)

}

}

function onexit() {

Shannon.Exit()

}

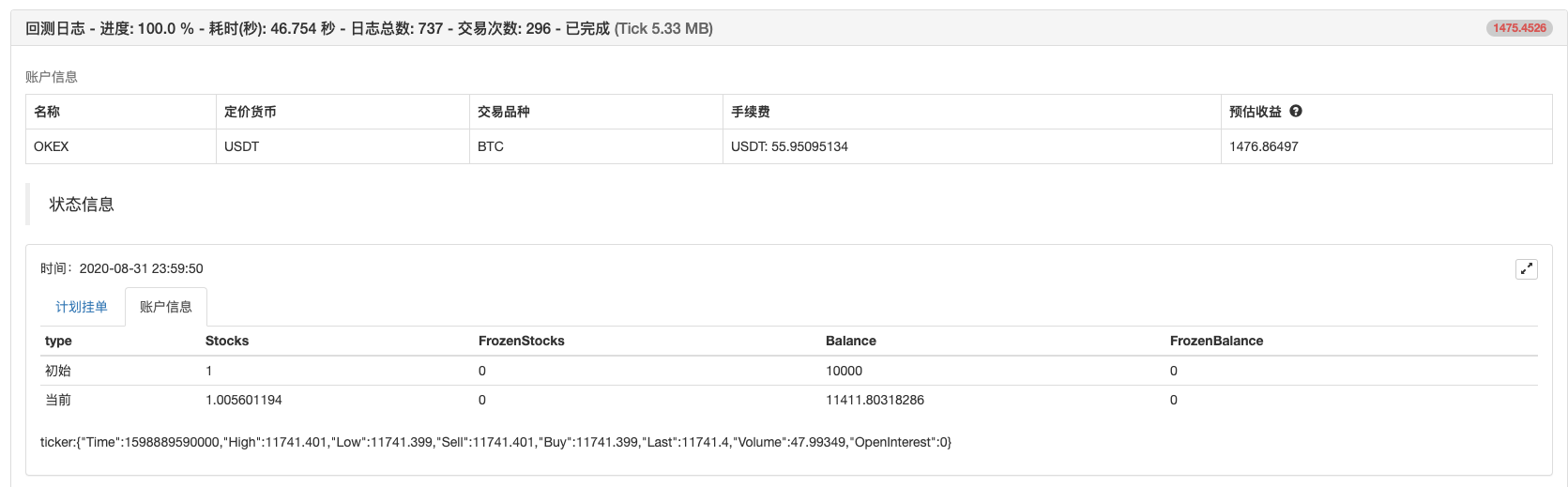

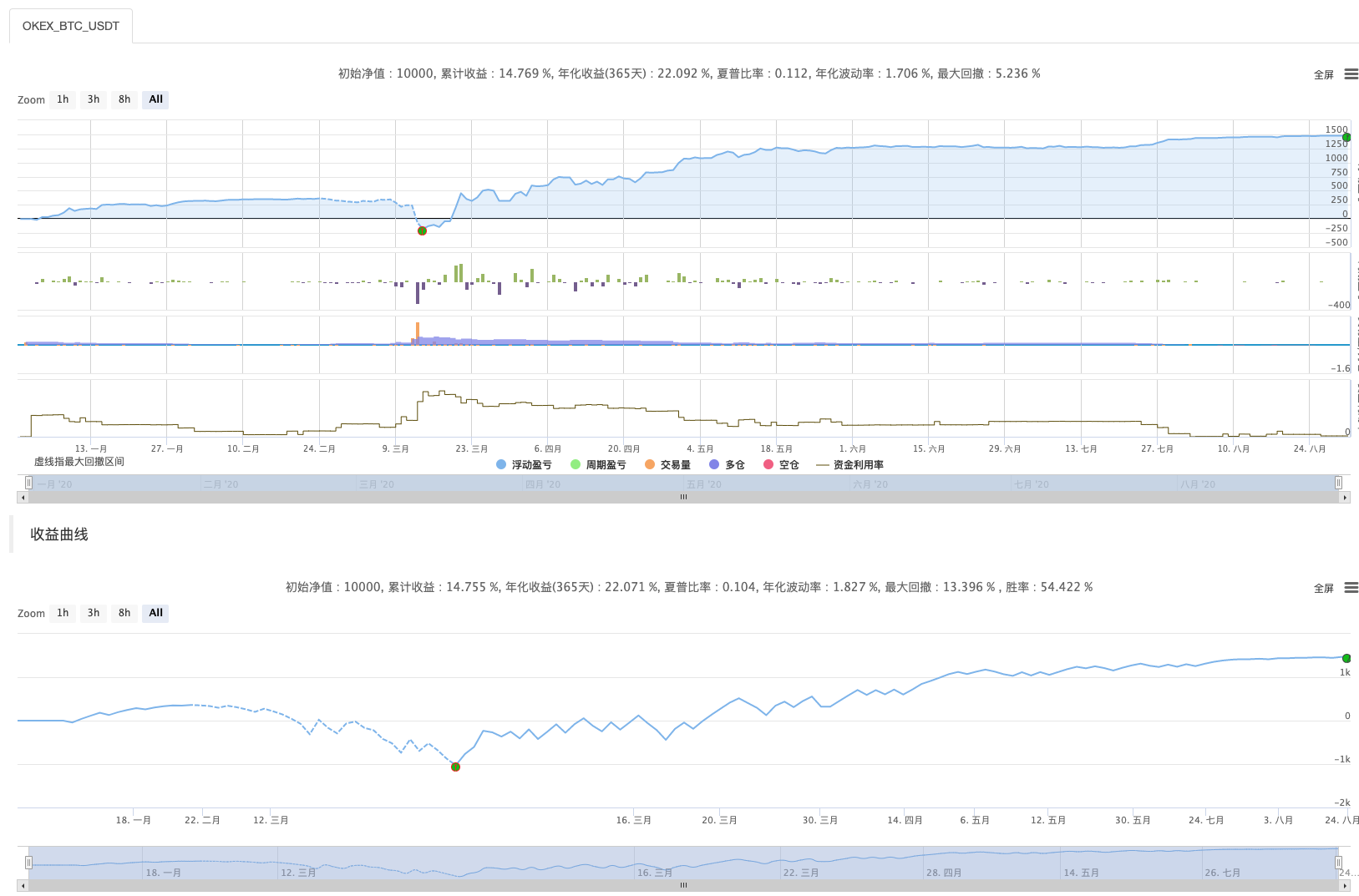

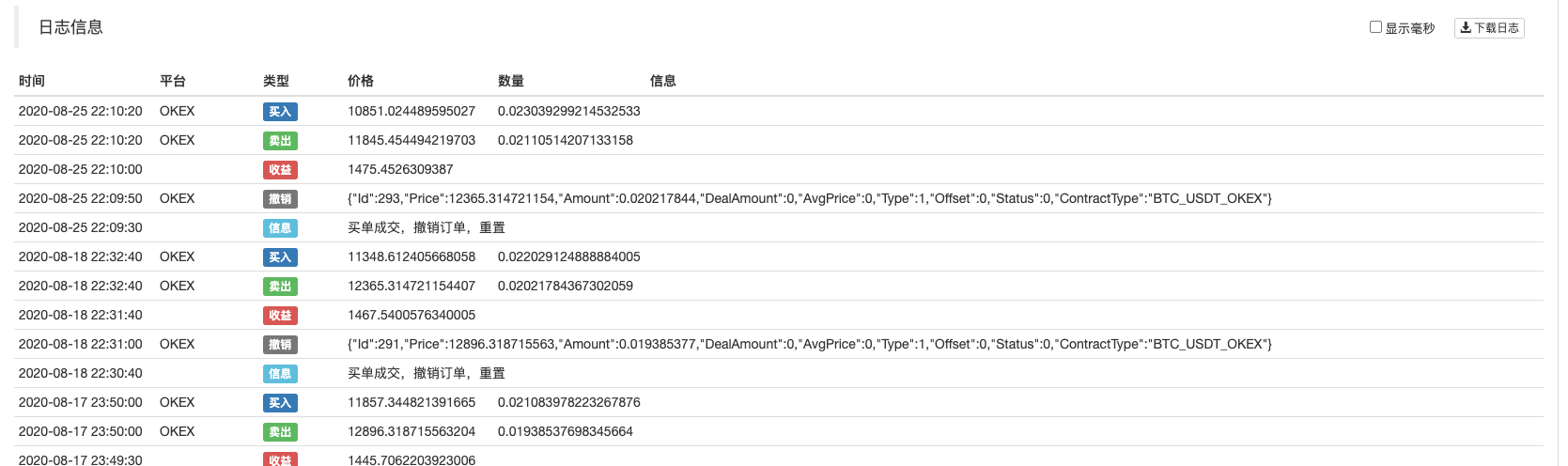

The retest is running

Optimized expansion

- The virtual listing mechanism can be added, and some trades all the listing limits, so it is possible that the order will not actually be hung, and you need to wait for the price to get closer to the real listing.

- Joining the futures market

- Expanded to multi-variety, multi-exchange version

The tactics are only for teaching purposes and should be used sparingly. The policy address:https://www.fmz.com/strategy/225746

- Quantifying Fundamental Analysis in the Cryptocurrency Market: Let Data Speak for Itself!

- Quantified research on the basics of coin circles - stop believing in all kinds of crazy professors, data is objective!

- The inventor of the Quantitative Data Exploration Module, an essential tool in the field of quantitative trading.

- Mastering Everything - Introduction to FMZ New Version of Trading Terminal (with TRB Arbitrage Source Code)

- Get all the details about the new FMZ trading terminal (with the TRB suite source code)

- FMZ Quant: An Analysis of Common Requirements Design Examples in the Cryptocurrency Market (II)

- How to Exploit Brainless Selling Bots with a High-Frequency Strategy in 80 Lines of Code

- FMZ quantification: common demands on the cryptocurrency market design example analysis (II)

- How to exploit brainless robots for sale with high-frequency strategies of 80 lines of code

- FMZ Quant: An Analysis of Common Requirements Design Examples in the Cryptocurrency Market (I)

- FMZ quantification: common demands of the cryptocurrency market design instance analysis (1)