Jugar JavaScript con el viejo blanco - crear un compañero que haga compras y ventas (4) enseñarle un poco de conocimiento simple (aplicaciones de línea recta)

El autor:Un sueño pequeño., Creado: 2017-03-08 11:52:02, Actualizado: 2017-10-11 10:37:23Jugar con el viejo blanco y el viejo ladrón de JavaScript para crear un compañero de compras y ventas.

Enseñarle un conocimiento sencillo (aplicación lineal)

En el capítulo anterior, practicamos un montón de código interesante en el sistema de cajas de arena, y hoy necesitamos que nuestro programa salga de la caja de arena y vea el mundo exterior, por supuesto, primero tenemos que enseñarle algo.

-

La lógica de compra y venta

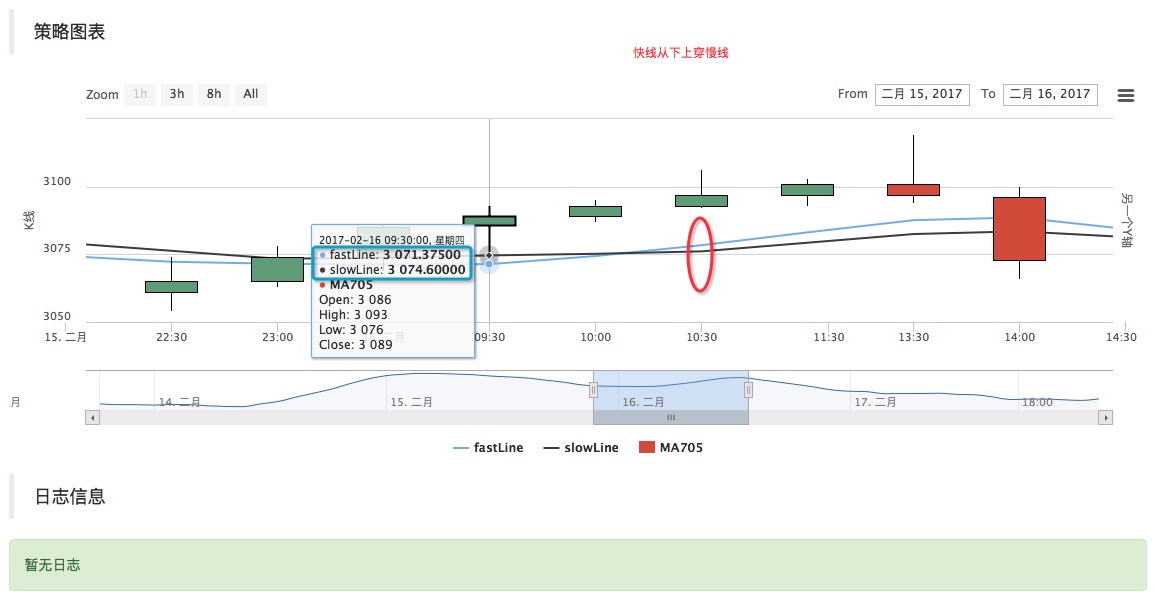

Esta lógica de compra y venta es probablemente la estrategia más simple y básica en el mundo de la negociación programada y de la negociación cuantitativa. Es decir: un objeto de referencia, como el contrato MA705 (contrato de metanol), el ciclo tiene una media de 10 Bar (columna de línea K) y el ciclo tiene una media de 8 Bar, la diferencia de contraste. Los siguientes 10 ciclos (ciclo largo) son la línea lenta, y los ocho ciclos (ciclo relativamente corto) son la línea rápida.

La dirección de la plantilla de gráficos es:https://www.fmz.com/strategy/27293

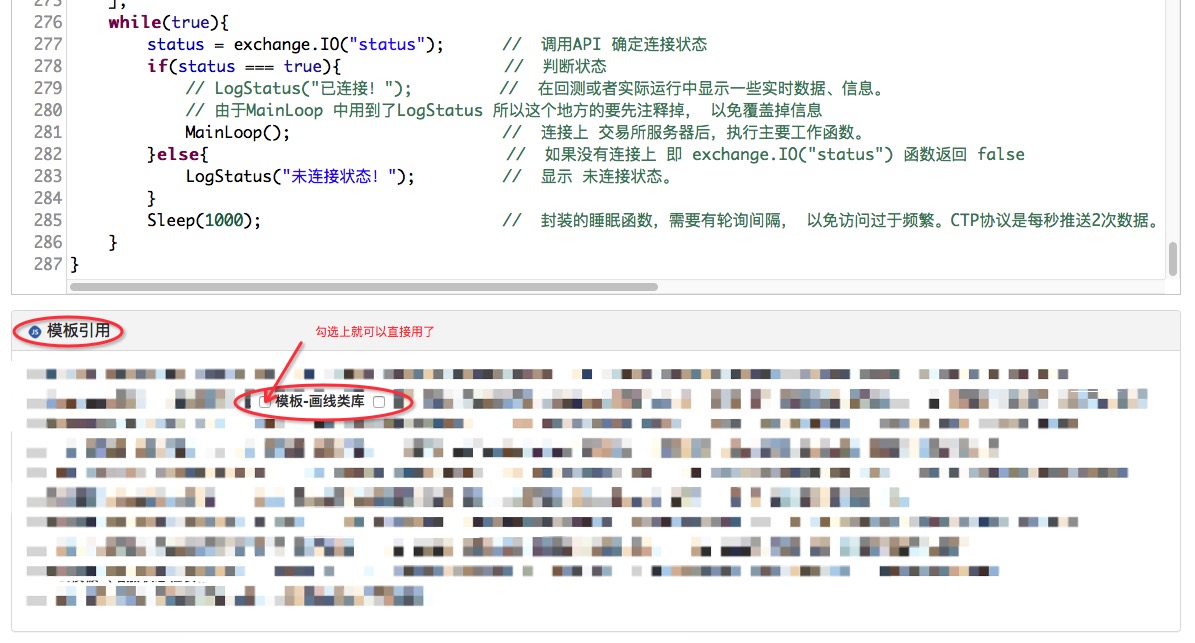

La copia aparece en la barra de referencia de la plantilla de etiquetas, se usa directamente, recuerde seleccionar.

El código es muy simple:

var PreRecordTime = 0; var isFirst = true; function MainLoop(){ var info = exchange.SetContractType("MA705"); if(!info){ return; } var records = exchange.GetRecords(); if(!records || records.length < 10){ // 因为长周期 为10 所以要计算10个Bar的均值, 必须要有10个K线才能计算出来。 return; // 不满足的情况,返回,重新来。 } if(isFirst){ PreRecordTime = records[records.length - 1].Time; isFirst = false; } var fastLine = TA.MA(records, 8); // 均线指标,计算出给定 的K线数据 8个 Bar 的均值, 按顺序压入数组(随时间序列,和K线Bar时间同步形成一条线,所以叫快线) 返回这个数组给变量fastLine var slowLine = TA.MA(records, 10); // 同上 区别是10个Bar ,所以叫慢线(周期大,均值变化的慢)。 var current_fastLine = fastLine[fastLine.length - 1]; // 这个数组的 倒数第一个索引 fastLine.length - 1 ,也就是表示的 快线的最后一个值 ,就是当前K线 对应的 快线均值。 var current_slowLine = slowLine[slowLine.length - 1]; // 同上 if(PreRecordTime !== records[records.length - 1].Time){ // K线更新了才确定当前最新的前一根Bar $.PlotLine("fastLine", fastLine[fastLine.length - 2], PreRecordTime); // 引用了模板,可以直接使用这个模块导出函数 画线。(其实就是封装成 模块了) $.PlotLine("slowLine", slowLine[slowLine.length - 2], PreRecordTime); // 同上 画指标线 PreRecordTime = records[records.length - 1].Time; $.PlotLine("fastLine", current_fastLine, records[records.length - 1].Time); $.PlotLine("slowLine", current_slowLine, records[records.length - 1].Time); }else{ $.PlotLine("fastLine", current_fastLine, records[records.length - 1].Time); // 当前的不停在变动。 $.PlotLine("slowLine", current_slowLine, records[records.length - 1].Time); } $.PlotRecords(records, "MA705"); // 画K线 } var cfg = $.GetCfg(); function main() { var status = null; cfg.yAxis = [{ title: {text: 'K线'}, //标题 style: {color: '#4572A7'}, //样式 opposite: false //生成右边Y轴 }, { title:{text: "另一个Y轴"}, opposite: true //生成右边Y轴 ceshi } ]; while(true){ status = exchange.IO("status"); // 调用API 确定连接状态 if(status === true){ // 判断状态 // LogStatus("已连接!"); // 在回测或者实际运行中显示一些实时数据、信息。 // 由于MainLoop 中用到了LogStatus 所以这个地方的要先注释掉, 以免覆盖掉信息 MainLoop(); // 连接上 交易所服务器后,执行主要工作函数。 }else{ // 如果没有连接上 即 exchange.IO("status") 函数返回 false LogStatus("未连接状态!"); // 显示 未连接状态。 } Sleep(1000); // 封装的睡眠函数,需要有轮询间隔, 以免访问过于频繁。CTP协议是每秒推送2次数据。 } }En la actualidad, la mayoría de los usuarios de Twitter están usando el sistema de cajas de arena para obtener información sobre el tema.

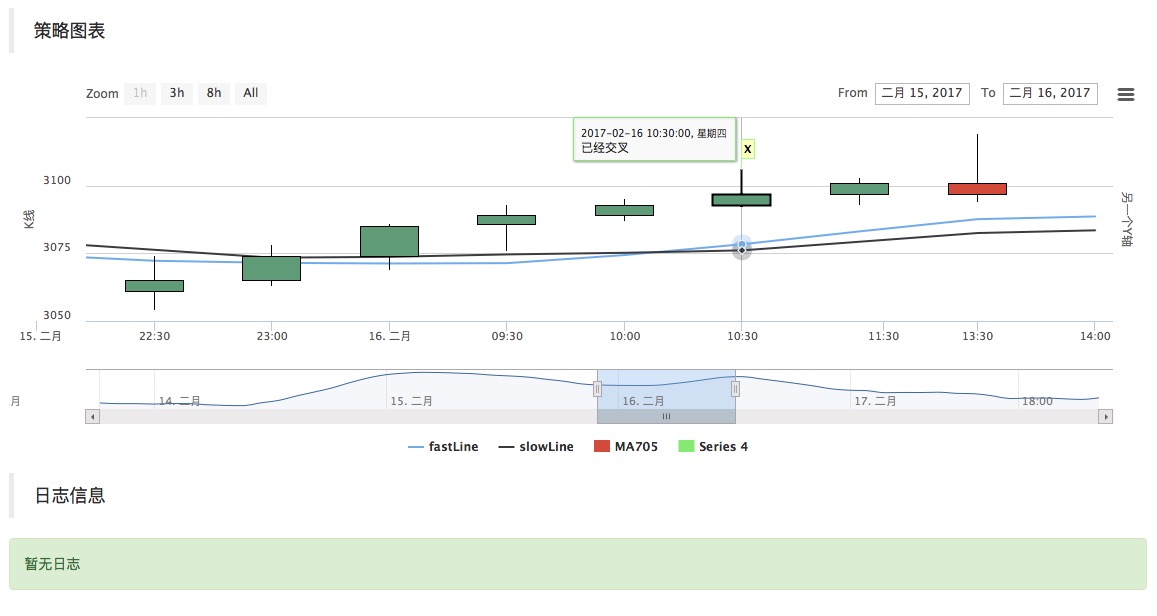

Se puede ver que en la subida local se produce una línea rápida que atraviesa una línea lenta desde abajo, ¿cómo se describe esta forma en el código?

// 判断指标形态 if(fastLine.length > 3 && slowLine.length > 3 && fastLine[fastLine.length - 3] < slowLine[slowLine.length - 3] && fastLine[fastLine.length - 2] > slowLine[slowLine.length - 2]){ $.PlotFlag(records[records.length - 2].Time, '已经交叉', 'X'); // 在图表上打个标记 }

La línea rápida pasa por la línea lenta desde arriba hacia abajo y también es simétrica. En este sentido, añadimos un par de código al programa.

-

Los maestros aprenden a operar de manera uniforme

Aquí hay otro módulo escrito en JavaScript, pero no voy a citarlo antes, que se incrusta directamente en nuestro programa. El contrato MA705 (metanol) sigue siendo utilizado como símbolo comercial.

// --------交易模块-------------

var Interval = 500;

var SlideTick = 1;

var RiskControl = false;

var __orderCount = 0

var __orderDay = 0

function CanTrade(tradeAmount) {

if (!RiskControl) {

return true

}

if (typeof(tradeAmount) == 'number' && tradeAmount > MaxTradeAmount) {

Log("风控模块限制, 超过最大下单量", MaxTradeAmount, "#ff0000 @");

throw "中断执行"

return false;

}

var nowDay = new Date().getDate();

if (nowDay != __orderDay) {

__orderDay = nowDay;

__orderCount = 0;

}

__orderCount++;

if (__orderCount > MaxTrade) {

Log("风控模块限制, 不可交易, 超过最大下单次数", MaxTrade, "#ff0000 @");

throw "中断执行"

return false;

}

return true;

}

function init() {

if (typeof(SlideTick) === 'undefined') {

SlideTick = 1;

} else {

SlideTick = parseInt(SlideTick);

}

Log("商品交易类库加载成功");

}

function GetPosition(e, contractType, direction, positions) {

var allCost = 0;

var allAmount = 0;

var allProfit = 0;

var allFrozen = 0;

var posMargin = 0;

if (typeof(positions) === 'undefined' || !positions) {

positions = _C(e.GetPosition);

}

for (var i = 0; i < positions.length; i++) {

if (positions[i].ContractType == contractType &&

(((positions[i].Type == PD_LONG || positions[i].Type == PD_LONG_YD) && direction == PD_LONG) || ((positions[i].Type == PD_SHORT || positions[i].Type == PD_SHORT_YD) && direction == PD_SHORT))

) {

posMargin = positions[i].MarginLevel;

allCost += (positions[i].Price * positions[i].Amount);

allAmount += positions[i].Amount;

allProfit += positions[i].Profit;

allFrozen += positions[i].FrozenAmount;

}

}

if (allAmount === 0) {

return null;

}

return {

MarginLevel: posMargin,

FrozenAmount: allFrozen,

Price: _N(allCost / allAmount),

Amount: allAmount,

Profit: allProfit,

Type: direction,

ContractType: contractType

};

}

function Open(e, contractType, direction, opAmount) {

var initPosition = GetPosition(e, contractType, direction);

var isFirst = true;

var initAmount = initPosition ? initPosition.Amount : 0;

var positionNow = initPosition;

while (true) {

var needOpen = opAmount;

if (isFirst) {

isFirst = false;

} else {

positionNow = GetPosition(e, contractType, direction);

if (positionNow) {

needOpen = opAmount - (positionNow.Amount - initAmount);

}

}

var insDetail = _C(e.SetContractType, contractType);

//Log("初始持仓", initAmount, "当前持仓", positionNow, "需要加仓", needOpen);

if (needOpen < insDetail.MinLimitOrderVolume) {

break;

}

if (!CanTrade(opAmount)) {

break;

}

var depth = _C(e.GetDepth);

var amount = Math.min(insDetail.MaxLimitOrderVolume, needOpen);

e.SetDirection(direction == PD_LONG ? "buy" : "sell");

var orderId;

if (direction == PD_LONG) {

orderId = e.Buy(depth.Asks[0].Price + (insDetail.PriceTick * SlideTick), Math.min(amount, depth.Asks[0].Amount), contractType, 'Ask', depth.Asks[0]);

} else {

orderId = e.Sell(depth.Bids[0].Price - (insDetail.PriceTick * SlideTick), Math.min(amount, depth.Bids[0].Amount), contractType, 'Bid', depth.Bids[0]);

}

// CancelPendingOrders

while (true) {

Sleep(Interval);

var orders = _C(e.GetOrders);

if (orders.length === 0) {

break;

}

for (var j = 0; j < orders.length; j++) {

e.CancelOrder(orders[j].Id);

if (j < (orders.length - 1)) {

Sleep(Interval);

}

}

}

}

var ret = {

price: 0,

amount: 0,

position: positionNow

};

if (!positionNow) {

return ret;

}

if (!initPosition) {

ret.price = positionNow.Price;

ret.amount = positionNow.Amount;

} else {

ret.amount = positionNow.Amount - initPosition.Amount;

ret.price = _N(((positionNow.Price * positionNow.Amount) - (initPosition.Price * initPosition.Amount)) / ret.amount);

}

return ret;

}

function Cover(e, contractType) {

var insDetail = _C(e.SetContractType, contractType);

while (true) {

var n = 0;

var opAmount = 0;

var positions = _C(e.GetPosition);

for (var i = 0; i < positions.length; i++) {

if (positions[i].ContractType != contractType) {

continue;

}

var amount = Math.min(insDetail.MaxLimitOrderVolume, positions[i].Amount);

var depth;

if (positions[i].Type == PD_LONG || positions[i].Type == PD_LONG_YD) {

depth = _C(e.GetDepth);

opAmount = Math.min(amount, depth.Bids[0].Amount);

if (!CanTrade(opAmount)) {

return;

}

e.SetDirection(positions[i].Type == PD_LONG ? "closebuy_today" : "closebuy");

e.Sell(depth.Bids[0].Price - (insDetail.PriceTick * SlideTick), opAmount, contractType, positions[i].Type == PD_LONG ? "平今" : "平昨", 'Bid', depth.Bids[0]);

n++;

} else if (positions[i].Type == PD_SHORT || positions[i].Type == PD_SHORT_YD) {

depth = _C(e.GetDepth);

opAmount = Math.min(amount, depth.Asks[0].Amount);

if (!CanTrade(opAmount)) {

return;

}

e.SetDirection(positions[i].Type == PD_SHORT ? "closesell_today" : "closesell");

e.Buy(depth.Asks[0].Price + (insDetail.PriceTick * SlideTick), opAmount, contractType, positions[i].Type == PD_SHORT ? "平今" : "平昨", 'Ask', depth.Asks[0]);

n++;

}

}

if (n === 0) {

break;

}

while (true) {

Sleep(Interval);

var orders = _C(e.GetOrders);

if (orders.length === 0) {

break;

}

for (var j = 0; j < orders.length; j++) {

e.CancelOrder(orders[j].Id);

if (j < (orders.length - 1)) {

Sleep(Interval);

}

}

}

}

}

var PositionManager = (function() {

function PositionManager(e) {

if (typeof(e) === 'undefined') {

e = exchange;

}

if (e.GetName() !== 'Futures_CTP') {

throw 'Only support CTP';

}

this.e = e;

this.account = null;

}

// Get Cache

PositionManager.prototype.Account = function() {

if (!this.account) {

this.account = _C(this.e.GetAccount);

}

return this.account;

};

PositionManager.prototype.GetAccount = function(getTable) {

this.account = _C(this.e.GetAccount);

if (typeof(getTable) !== 'undefined' && getTable) {

return AccountToTable(this.e.GetRawJSON())

}

return this.account;

};

PositionManager.prototype.GetPosition = function(contractType, direction, positions) {

return GetPosition(this.e, contractType, direction, positions);

};

PositionManager.prototype.OpenLong = function(contractType, shares) {

if (!this.account) {

this.account = _C(this.e.GetAccount);

}

return Open(this.e, contractType, PD_LONG, shares);

};

PositionManager.prototype.OpenShort = function(contractType, shares) {

if (!this.account) {

this.account = _C(this.e.GetAccount);

}

return Open(this.e, contractType, PD_SHORT, shares);

};

PositionManager.prototype.Cover = function(contractType) {

if (!this.account) {

this.account = _C(this.e.GetAccount);

}

return Cover(this.e, contractType);

};

PositionManager.prototype.CoverAll = function() {

if (!this.account) {

this.account = _C(this.e.GetAccount);

}

while (true) {

var positions = _C(this.e.GetPosition)

if (positions.length == 0) {

break

}

for (var i = 0; i < positions.length; i++) {

// Cover Hedge Position First

if (positions[i].ContractType.indexOf('&') != -1) {

Cover(this.e, positions[i].ContractType)

Sleep(1000)

}

}

for (var i = 0; i < positions.length; i++) {

if (positions[i].ContractType.indexOf('&') == -1) {

Cover(this.e, positions[i].ContractType)

Sleep(1000)

}

}

}

};

PositionManager.prototype.Profit = function(contractType) {

var accountNow = _C(this.e.GetAccount);

return _N(accountNow.Balance - this.account.Balance);

};

return PositionManager;

})();

$.NewPositionManager = function(e) {

return new PositionManager(e);

};

// Via: http://mt.sohu.com/20160429/n446860150.shtml

$.IsTrading = function(symbol) {

var now = new Date();

var day = now.getDay();

var hour = now.getHours();

var minute = now.getMinutes();

if (day === 0 || (day === 6 && (hour > 2 || hour == 2 && minute > 30))) {

return false;

}

symbol = symbol.replace('SPD ', '').replace('SP ', '');

var p, i, shortName = "";

for (i = 0; i < symbol.length; i++) {

var ch = symbol.charCodeAt(i);

if (ch >= 48 && ch <= 57) {

break;

}

shortName += symbol[i].toUpperCase();

}

var period = [

[9, 0, 10, 15],

[10, 30, 11, 30],

[13, 30, 15, 0]

];

if (shortName === "IH" || shortName === "IF" || shortName === "IC") {

period = [

[9, 30, 11, 30],

[13, 0, 15, 0]

];

} else if (shortName === "TF" || shortName === "T") {

period = [

[9, 15, 11, 30],

[13, 0, 15, 15]

];

}

if (day >= 1 && day <= 5) {

for (i = 0; i < period.length; i++) {

p = period[i];

if ((hour > p[0] || (hour == p[0] && minute >= p[1])) && (hour < p[2] || (hour == p[2] && minute < p[3]))) {

return true;

}

}

}

var nperiod = [

[

['AU', 'AG'],

[21, 0, 02, 30]

],

[

['CU', 'AL', 'ZN', 'PB', 'SN', 'NI'],

[21, 0, 01, 0]

],

[

['RU', 'RB', 'HC', 'BU'],

[21, 0, 23, 0]

],

[

['P', 'J', 'M', 'Y', 'A', 'B', 'JM', 'I'],

[21, 0, 23, 30]

],

[

['SR', 'CF', 'RM', 'MA', 'TA', 'ZC', 'FG', 'IO'],

[21, 0, 23, 30]

],

];

for (i = 0; i < nperiod.length; i++) {

for (var j = 0; j < nperiod[i][0].length; j++) {

if (nperiod[i][0][j] === shortName) {

p = nperiod[i][1];

var condA = hour > p[0] || (hour == p[0] && minute >= p[1]);

var condB = hour < p[2] || (hour == p[2] && minute < p[3]);

// in one day

if (p[2] >= p[0]) {

if ((day >= 1 && day <= 5) && condA && condB) {

return true;

}

} else {

if (((day >= 1 && day <= 5) && condA) || ((day >= 2 && day <= 6) && condB)) {

return true;

}

}

return false;

}

}

}

return false;

};

// --------交易模块完结----------

var PreRecordTime = 0;

var isFirst = true;

var IDLE = 0;

var OPENLONG = 1;

var COVER = 2;

var STATE = IDLE;

var InitAccount = null;

function MainLoop(){

var info = exchange.SetContractType("MA705");

if(!info){

return;

}

var records = exchange.GetRecords();

if(!records || records.length < 10){ // 因为长周期 为10 所以要计算10个Bar的均值, 必须要有10个K线才能计算出来。

return; // 不满足的情况,返回,重新来。

}

if(isFirst){

PreRecordTime = records[records.length - 1].Time;

InitAccount = exchange.GetAccount();

isFirst = false;

}

var fastLine = TA.MA(records, 5); // 均线指标,计算出给定 的K线数据 8个 Bar 的均值, 按顺序压入数组(随时间序列,和K线Bar时间同步形成一条线,所以叫快线) 返回这个数组给变量fastLine

var slowLine = TA.MA(records, 10); // 同上 区别是10个Bar ,所以叫慢线(周期大,均值变化的慢)。

var current_fastLine = fastLine[fastLine.length - 1]; // 这个数组的 倒数第一个索引 fastLine.length - 1 ,也就是表示的 快线的最后一个值 ,就是当前K线 对应的 快线均值。

var current_slowLine = slowLine[slowLine.length - 1]; // 同上

if(PreRecordTime !== records[records.length - 1].Time){ // K线更新了才确定当前最新的前一根Bar

$.PlotLine("fastLine", fastLine[fastLine.length - 2], PreRecordTime); // 引用了模板,可以直接使用这个模块导出函数 画线。(其实就是封装成 模块了)

$.PlotLine("slowLine", slowLine[slowLine.length - 2], PreRecordTime); // 同上 画指标线

PreRecordTime = records[records.length - 1].Time;

$.PlotLine("fastLine", current_fastLine, records[records.length - 1].Time);

$.PlotLine("slowLine", current_slowLine, records[records.length - 1].Time);

}else{

$.PlotLine("fastLine", current_fastLine, records[records.length - 1].Time); // 当前的不停在变动。

$.PlotLine("slowLine", current_slowLine, records[records.length - 1].Time);

}

$.PlotRecords(records, "MA705"); // 画K线

// 判断指标形态

if(STATE === IDLE && fastLine.length > 3 && slowLine.length > 3 && fastLine[fastLine.length - 3] < slowLine[slowLine.length - 3] && fastLine[fastLine.length - 2] > slowLine[slowLine.length - 2]){

P.OpenLong("MA705", 1);

STATE = OPENLONG;

$.PlotFlag(new Date().getTime(), '快线上传慢线', 'OPENLONG');

}

if(STATE === OPENLONG && fastLine[fastLine.length - 3] > slowLine[slowLine.length - 3] && fastLine[fastLine.length - 2] < slowLine[slowLine.length - 2]){

P.Cover("MA705");

STATE = COVER;

$.PlotFlag(new Date().getTime(), '快线下传慢线', 'COVER');

}

if(STATE === COVER){

var nowAccount = exchange.GetAccount();

LogProfit(nowAccount.Balance - InitAccount.Balance, nowAccount);

STATE = IDLE;

}

}

var cfg = $.GetCfg();

var P = null;

function main() {

var status = null;

P = $.NewPositionManager(exchange); // 构造一个 用于控制交易细节的对象。

cfg.yAxis = [{

title: {text: 'K线'}, //标题

style: {color: '#4572A7'}, //样式

opposite: false //生成右边Y轴

},

{

title:{text: "另一个Y轴"},

opposite: true //生成右边Y轴 ceshi

}

];

while(true){

status = exchange.IO("status"); // 调用API 确定连接状态

if(status === true){ // 判断状态

// LogStatus("已连接!"); // 在回测或者实际运行中显示一些实时数据、信息。

// 由于MainLoop 中用到了LogStatus 所以这个地方的要先注释掉, 以免覆盖掉信息

MainLoop(); // 连接上 交易所服务器后,执行主要工作函数。

}else{ // 如果没有连接上 即 exchange.IO("status") 函数返回 false

LogStatus("未连接状态!"); // 显示 未连接状态。

}

Sleep(1000); // 封装的睡眠函数,需要有轮询间隔, 以免访问过于频繁。CTP协议是每秒推送2次数据。

}

}

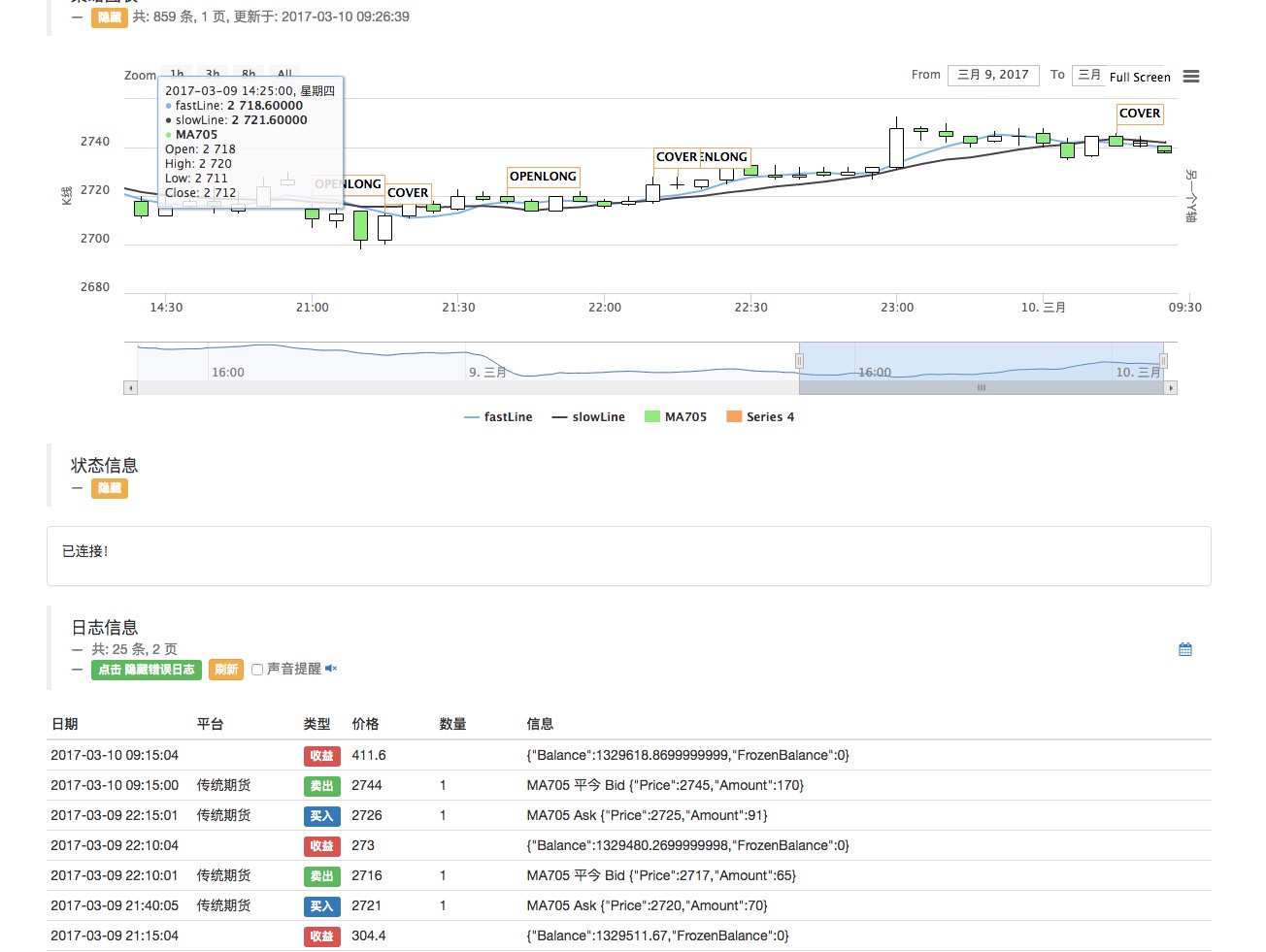

La caja de arena se refleja en la siguiente imagen:

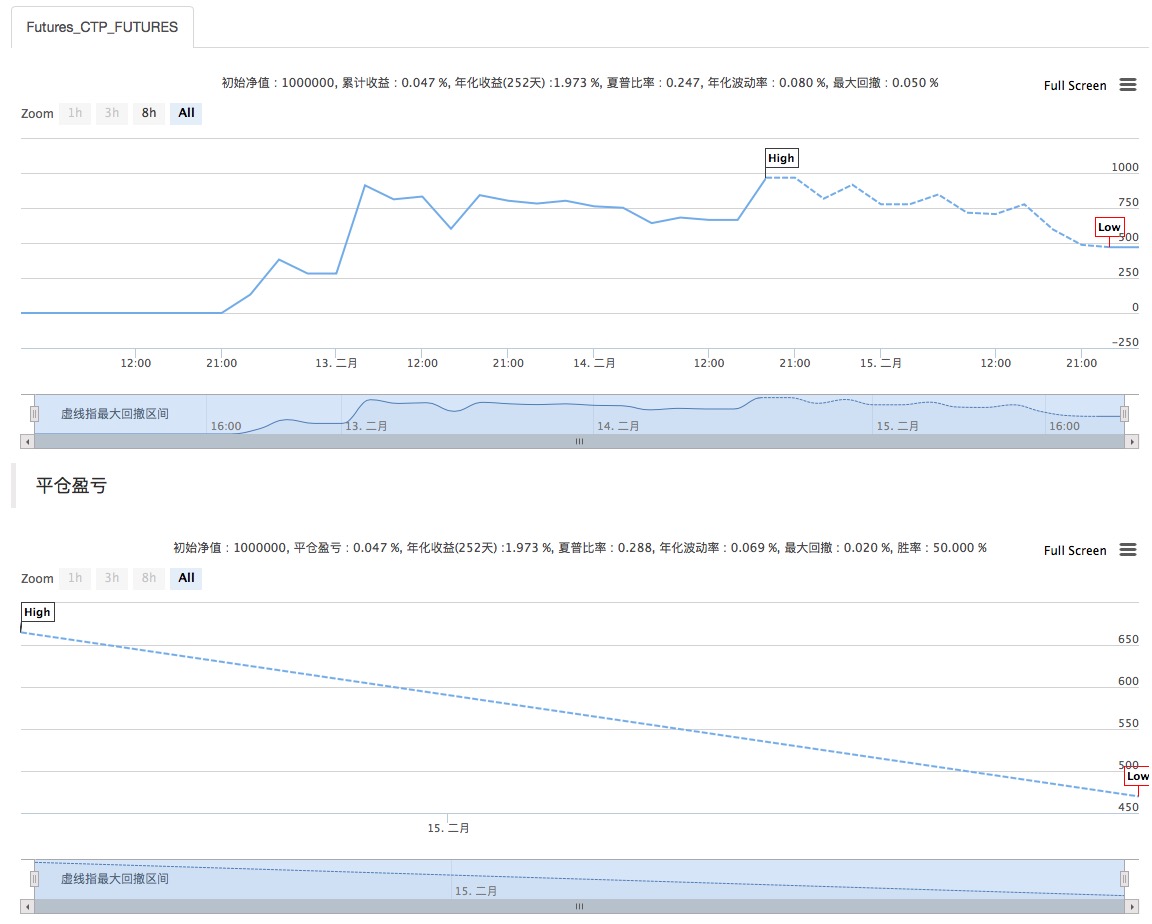

En la revisión, el mercado conmocionado retrocedió mucho, se puede ver que la lógica de negociación es imperfecta, es una ganancia positiva en la tendencia al alza, no significa que no haya problemas ((el mercado conmocionado puede ser sacudido =_=)).

-

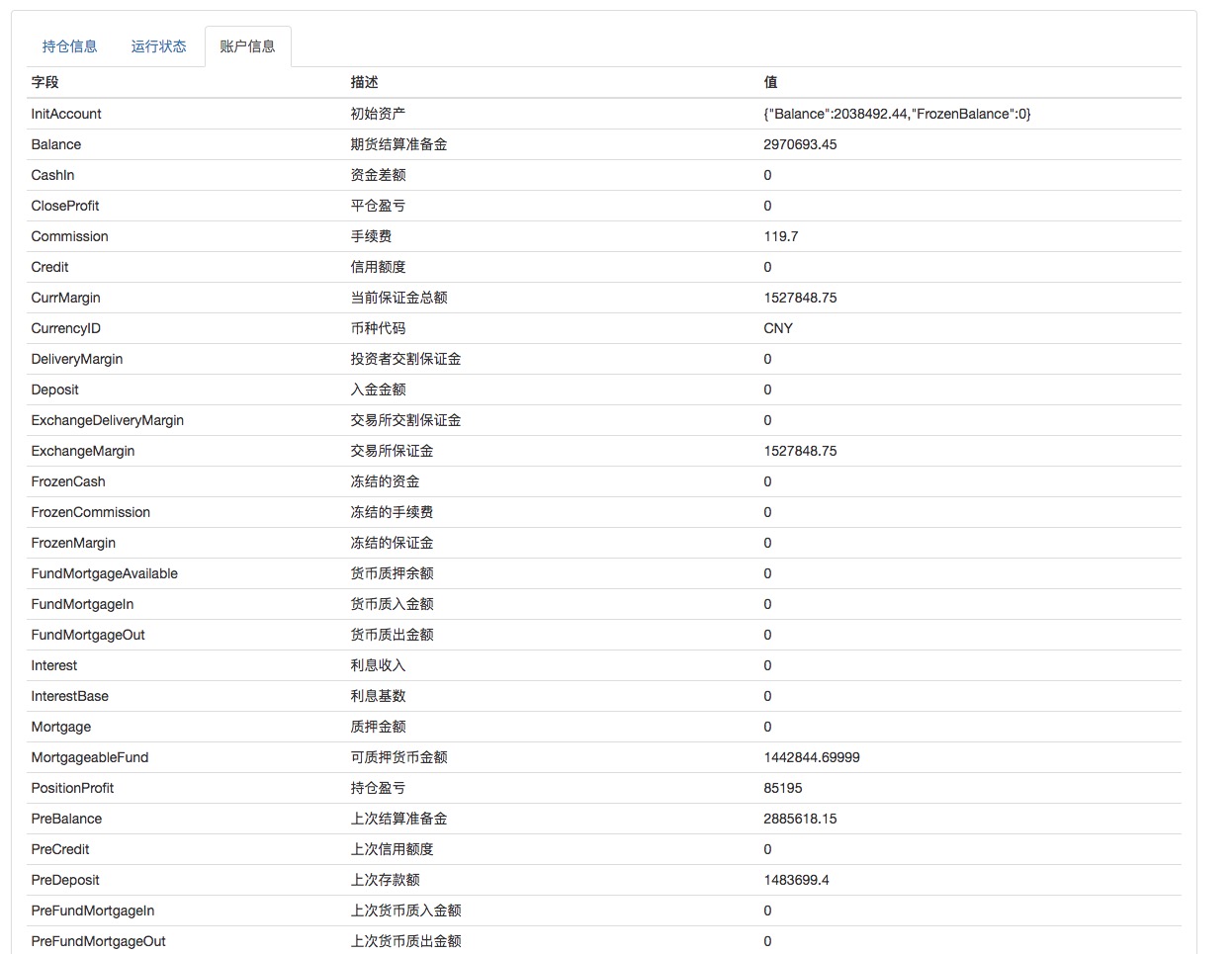

Si quieres salir de la caja de arena y ver el mundo exterior, puedes jugar con una cuenta de simulación de futuros simulada con tecnología Simnow.

Para más información sobre cómo solicitar una simnow Commodity Futures Simulator Account puedes consultar este post:https://www.fmz.com/bbs-topic/325Se puede programar transacciones analógicas directamente con el protocolo CTP.

El programa se ejecuta durante un tiempo, la política en sí es de carácter de demostración, todos sólo para la referencia, si se necesita para mejorar también se puede añadir el control de posición, stop stop stop stop, alerta de explosión de posición, etc. (dependiendo del juego de lenguaje de programación nativo JS, la libertad es muy alta, escribir la política es muy divertido).

En el caso de las cuentas falsas, puedes ponerlas en esta prueba.

Mira mi otro programa que se ejecuta en un disco de simulación, este punto complejo muestra un poco:

El código fuente es: "JS" y "JS".https://www.fmz.com/strategy/17289

Antes de escribir esto, bienvenido a los lectores a dejarme un comentario! para sugerencias y comentarios, si se siente divertido puede compartir con más amigos que aman los programas que aman las transacciones

https://www.fmz.com/bbs-topic/727

Programador littleDream, originalmente

- ¿Cómo puedo recuperar el host original? ¿Cómo puedo recuperar el host original si el host se reinició?

- ¿La inversión en valor tiene una definición de riesgo diferente a la que usted piensa?

- Me gustaría preguntar qué plataformas pueden soportar plataformas virtuales y qué tipo de transacciones.

- Mercado cero y negativo

- Jugar JavaScript con los viejos -- Crear un compañero de compras y ventas [7] herramientas útiles para saber por qué es útil!

- Jugar JavaScript con el viejo blanco - crear un compañero que haga compras y ventas - desarrollar el código de herramientas para el robot

- Negociación de estrategias de alta frecuencia: hacer el mercado y la opción inversa

- Ser un probabilista: el tonto que se pasea al azar leyendo libros.

- Probabilidades, probabilidades y expectativas positivas de las transacciones a largo plazo

- Jugar JavaScript con el viejo blanco - crear un compañero que haga compras y ventas (5)

- Jugar JavaScript con el viejo blanco - crear un compañero de compras y ventas - un tipo alegre y joven que le gusta lo nuevo que hay alrededor.

- ¡Pregúntenle a los dioses si tiene dudas acerca de las funciones futuras!

- Jugar JavaScript con el viejo blanco - crear un compañero de compras y ventas (2) nacido en una caja de arena

- Jugar JavaScript con el viejo blanco - Crear un compañero que haga compras y ventas

- El dinero y el crédito del sistema bancario monetario

- ¡Las negociaciones de futuros: la búsqueda de la certeza perfecta es el veneno del sistema de negociación!

- Las estrategias de negociación de los jugadores

- HttpQuery no funciona en Python

- ¿Qué significa esto? ¿Qué significa esto?

- Detalles: Las reglas sobre el tamaño de las unidades de posición de las tortugas (Reglas de comercio de tortugas)