Enseñarle a diseñar una biblioteca de clases de plantillas para obtener datos de línea K de longitud especificada

El autor:- ¿ Por qué?, Creado: 2023-06-29 17:27:59, Actualizado: 2023-09-18 19:33:33

Enseñarle a diseñar una biblioteca de clases de plantillas para obtener datos de línea K de longitud especificada

Cuando se diseñan estrategias de tendencia, a menudo es necesario disponer de un número suficiente de barras de la línea K para el cálculo de los indicadores.exchange.GetRecords()En el diseño inicial de las API de intercambio de criptomonedas, no había soporte para la paginación en la interfaz de línea K, y la interfaz de línea K de la bolsa solo proporcionó una cantidad limitada de datos.

La interfaz de línea K de la API de contratos de Binance

Interfaz de línea K de Binance

Datos de la línea K

La hora de apertura de cada línea K en elGET /dapi/v1/klinesel punto final puede considerarse como un identificador único.

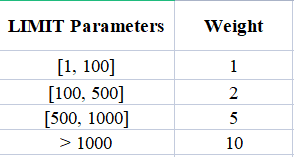

El peso de la solicitud depende del valor del parámetro

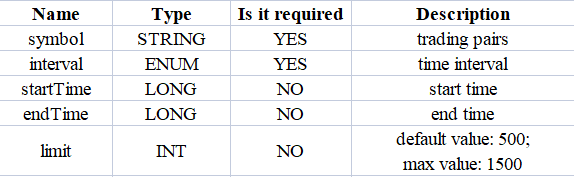

Parámetros:

En primer lugar, necesitamos consultar la documentación de la API del exchange

Dado que nuestro requisito de diseño es consultar un número específico de datos de línea K, por ejemplo, consultar la línea K de 1 hora, 5000 bares de datos de línea K de 1 hora desde el momento actual hacia el pasado, es evidente que hacer una sola llamada de API al intercambio no recuperará los datos deseados.

Para lograr esto, podemos implementar la paginación y dividir la consulta en segmentos desde el momento actual hacia un momento histórico específico. Dado que conocemos el período de datos de la línea K deseado, podemos calcular fácilmente el tiempo de inicio y final para cada segmento. Luego podemos consultar cada segmento en secuencia hacia el momento histórico hasta que recuperemos suficientes barras.

Diseño Versión JavaScript de la plantilla de datos históricos de línea K de la consulta paginada

Función de interfaz para plantillas de diseño:$.GetRecordsByLength(e, period, length).

/**

* desc: $.GetRecordsByLength is the interface function of this template library, this function is used to get the K-line data of the specified K-line length

* @param {Object} e - exchange object

* @param {Int} period - K-line period, in seconds

* @param {Int} length - Specify the length of the acquired K-line data, which is related to the exchange interface limits

* @returns {Array<Object>} - K-line data

*/

Diseñar la función$.GetRecordsByLength, que se utiliza típicamente en la etapa inicial de la ejecución de la estrategia para calcular indicadores basados en un largo período de datos de línea K. Una vez que esta función se ejecuta y se obtienen datos suficientes, solo se necesitan actualizar nuevos datos de línea K. No es necesario llamar a esta función nuevamente para recuperar datos de línea K excesivamente largos, ya que daría lugar a llamadas innecesarias de API.

Por lo tanto, también es necesario diseñar una interfaz para las actualizaciones de datos posteriores:$.UpdataRecords(e, records, period).

/**

* desc: $.UpdataRecords is the interface function of this template library, this function is used to update the K-line data.

* @param {Object} e - exchange object

* @param {Array<Object>} records - K-line data sources that need to be updated

* @param {Int} period - K-line period, needs to be the same as the K-line data period passed in the records parameter

* @returns {Bool} - Whether the update was successful

*/

El siguiente paso es implementar estas funciones de interfaz.

/**

* desc: $.GetRecordsByLength is the interface function of this template library, this function is used to get the K-line data of the specified K-line length

* @param {Object} e - exchange object

* @param {Int} period - K-line period, in seconds

* @param {Int} length - Specify the length of the acquired K-line data, which is related to the exchange interface limits

* @returns {Array<Object>} - K-line data

*/

$.GetRecordsByLength = function(e, period, length) {

if (!Number.isInteger(period) || !Number.isInteger(length)) {

throw "params error!"

}

var exchangeName = e.GetName()

if (exchangeName == "Futures_Binance") {

return getRecordsForFuturesBinance(e, period, length)

} else {

throw "not support!"

}

}

/**

* desc: getRecordsForFuturesBinance, the specific implementation of the function to get K-line data for Binance Futures Exchange

* @param {Object} e - exchange object

* @param {Int} period - K-line period, in seconds

* @param {Int} length - Specify the length of the acquired K-line data, which is related to the exchange interface limits

* @returns {Array<Object>} - K-line data

*/

function getRecordsForFuturesBinance(e, period, length) {

var contractType = e.GetContractType()

var currency = e.GetCurrency()

var strPeriod = String(period)

var symbols = currency.split("_")

var baseCurrency = ""

var quoteCurrency = ""

if (symbols.length == 2) {

baseCurrency = symbols[0]

quoteCurrency = symbols[1]

} else {

throw "currency error!"

}

var realCt = e.SetContractType(contractType)["instrument"]

if (!realCt) {

throw "realCt error"

}

// m -> minute; h -> hour; d -> day; w -> week; M -> month

var periodMap = {}

periodMap[(60).toString()] = "1m"

periodMap[(60 * 3).toString()] = "3m"

periodMap[(60 * 5).toString()] = "5m"

periodMap[(60 * 15).toString()] = "15m"

periodMap[(60 * 30).toString()] = "30m"

periodMap[(60 * 60).toString()] = "1h"

periodMap[(60 * 60 * 2).toString()] = "2h"

periodMap[(60 * 60 * 4).toString()] = "4h"

periodMap[(60 * 60 * 6).toString()] = "6h"

periodMap[(60 * 60 * 8).toString()] = "8h"

periodMap[(60 * 60 * 12).toString()] = "12h"

periodMap[(60 * 60 * 24).toString()] = "1d"

periodMap[(60 * 60 * 24 * 3).toString()] = "3d"

periodMap[(60 * 60 * 24 * 7).toString()] = "1w"

periodMap[(60 * 60 * 24 * 30).toString()] = "1M"

var records = []

var url = ""

if (quoteCurrency == "USDT") {

// GET https://fapi.binance.com /fapi/v1/klines symbol , interval , startTime , endTime , limit

// limit maximum value:1500

url = "https://fapi.binance.com/fapi/v1/klines"

} else if (quoteCurrency == "USD") {

// GET https://dapi.binance.com /dapi/v1/klines symbol , interval , startTime , endTime , limit

// The difference between startTime and endTime can be up to 200 days.

// limit maximum value:1500

url = "https://dapi.binance.com/dapi/v1/klines"

} else {

throw "not support!"

}

var maxLimit = 1500

var interval = periodMap[strPeriod]

if (typeof(interval) !== "string") {

throw "period error!"

}

var symbol = realCt

var currentTS = new Date().getTime()

while (true) {

// Calculate limit

var limit = Math.min(maxLimit, length - records.length)

var barPeriodMillis = period * 1000

var rangeMillis = barPeriodMillis * limit

var twoHundredDaysMillis = 200 * 60 * 60 * 24 * 1000

if (rangeMillis > twoHundredDaysMillis) {

limit = Math.floor(twoHundredDaysMillis / barPeriodMillis)

rangeMillis = barPeriodMillis * limit

}

var query = `symbol=${symbol}&interval=${interval}&endTime=${currentTS}&limit=${limit}`

var retHttpQuery = HttpQuery(url + "?" + query)

var ret = null

try {

ret = JSON.parse(retHttpQuery)

} catch(e) {

Log(e)

}

if (!ret || !Array.isArray(ret)) {

return null

}

// When the data cannot be searched because it is beyond the searchable range of the exchange

if (ret.length == 0 || currentTS <= 0) {

break

}

for (var i = ret.length - 1; i >= 0; i--) {

var ele = ret[i]

var bar = {

Time : parseInt(ele[0]),

Open : parseFloat(ele[1]),

High : parseFloat(ele[2]),

Low : parseFloat(ele[3]),

Close : parseFloat(ele[4]),

Volume : parseFloat(ele[5])

}

records.unshift(bar)

}

if (records.length >= length) {

break

}

currentTS -= rangeMillis

Sleep(1000)

}

return records

}

/**

* desc: $.UpdataRecords is the interface function of this template library, this function is used to update the K-line data.

* @param {Object} e - exchange object

* @param {Array<Object>} records - K-line data sources that need to be updated

* @param {Int} period - K-line period, needs to be the same as the K-line data period passed in the records parameter

* @returns {Bool} - Whether the update was successful

*/

$.UpdataRecords = function(e, records, period) {

var r = e.GetRecords(period)

if (!r) {

return false

}

for (var i = 0; i < r.length; i++) {

if (r[i].Time > records[records.length - 1].Time) {

// Add a new Bar

records.push(r[i])

// Update the previous Bar

if (records.length - 2 >= 0 && i - 1 >= 0 && records[records.length - 2].Time == r[i - 1].Time) {

records[records.length - 2] = r[i - 1]

}

} else if (r[i].Time == records[records.length - 1].Time) {

// Update Bar

records[records.length - 1] = r[i]

}

}

return true

}

En la plantilla, sólo hemos implementado soporte para el contrato de futuros Binance interfaz K-line, es decir, elgetRecordsForFuturesBinanceTambién se puede extender para soportar interfaces K-line de otros intercambios de criptomonedas.

Sesión de prueba

Como puede ver, el código para implementar estas funcionalidades en la plantilla no es extenso, con un total de menos de 200 líneas. Después de escribir el código de la plantilla, la prueba es crucial y no debe pasarse por alto. Además, para la recuperación de datos como esta, es importante realizar pruebas exhaustivas.

Para probarlo, debe copiar tanto la

La

function main() {

LogReset(1)

var testPeriod = PERIOD_M5

Log("Current exchanges tested:", exchange.GetName())

// If futures, you need to set up a contract

exchange.SetContractType("swap")

// Get K-line data of specified length using $.GetRecordsByLength

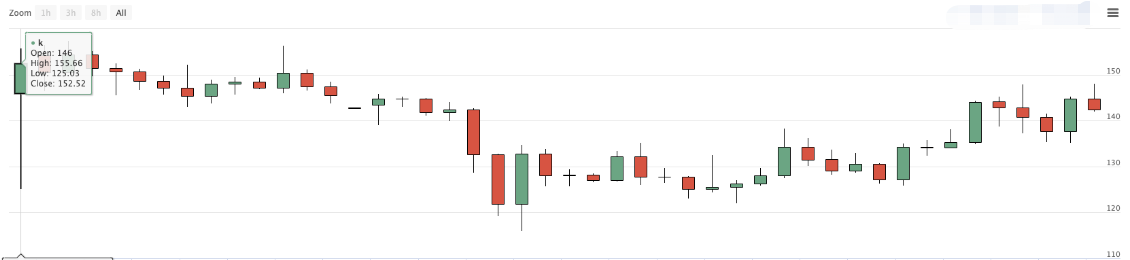

var r = $.GetRecordsByLength(exchange, testPeriod, 8000)

Log(r)

// Use the Plot test for easy observation

$.PlotRecords(r, "k")

// Test data

var diffTime = r[1].Time - r[0].Time

Log("diffTime:", diffTime, " ms")

for (var i = 0; i < r.length; i++) {

for (var j = 0; j < r.length; j++) {

// Check the repeat bar

if (i != j && r[i].Time == r[j].Time) {

Log(r[i].Time, i, r[j].Time, j)

throw "With duplicate Bar"

}

}

// Check Bar continuity

if (i < r.length - 1) {

if (r[i + 1].Time - r[i].Time != diffTime) {

Log("i:", i, ", diff:", r[i + 1].Time - r[i].Time, ", r[i].Time:", r[i].Time, ", r[i + 1].Time:", r[i + 1].Time)

throw "Bar discontinuity"

}

}

}

Log("Test passed")

Log("The length of the data returned by the $.GetRecordsByLength function:", r.length)

// Update data

while (true) {

$.UpdataRecords(exchange, r, testPeriod)

LogStatus(_D(), "r.length:", r.length)

$.PlotRecords(r, "k")

Sleep(5000)

}

}

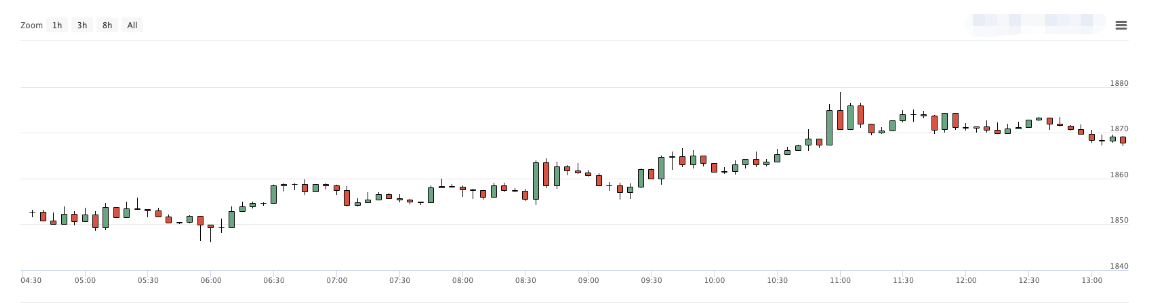

Aquí, usamos la líneavar testPeriod = PERIOD_M5Entonces podemos realizar una prueba de gráficos en los datos de línea K largos devueltos por elvar r = $.GetRecordsByLength(exchange, testPeriod, 8000) interface.

// Use the plot test for easy observation

$.PlotRecords(r, "k")

El siguiente ensayo para los datos de la línea K larga es:

// Test data

var diffTime = r[1].Time - r[0].Time

Log("diffTime:", diffTime, " ms")

for (var i = 0; i < r.length; i++) {

for (var j = 0; j < r.length; j++) {

// Check the repeat Bar

if (i != j && r[i].Time == r[j].Time) {

Log(r[i].Time, i, r[j].Time, j)

throw "With duplicate Bar"

}

}

// Check Bar continuity

if (i < r.length - 1) {

if (r[i + 1].Time - r[i].Time != diffTime) {

Log("i:", i, ", diff:", r[i + 1].Time - r[i].Time, ", r[i].Time:", r[i].Time, ", r[i + 1].Time:", r[i + 1].Time)

throw "Bar discontinuity"

}

}

}

Log("Test passed")

- Compruebe si hay barras duplicadas en los datos de la línea K.

- Compruebe la coherencia de los datos de la línea K (si la diferencia de marca horaria entre las barras adyacentes es igual).

Después de pasar estos controles, comprobar si la interfaz utilizada para actualizar los datos de la línea K,$.UpdateRecords(exchange, r, testPeriod), funciona correctamente.

// Update data

while (true) {

$.UpdataRecords(exchange, r, testPeriod)

LogStatus(_D(), "r.length:", r.length)

$.PlotRecords(r, "k")

Sleep(5000)

}

Este código emitirá continuamente datos de línea K en el gráfico de estrategia durante el comercio en vivo, lo que nos permite verificar si las actualizaciones y adiciones de datos de línea K funcionan correctamente.

Utilizando los datos diarios de la línea K, lo configuramos para recuperar 8000 barras (sabiendo que no hay datos de mercado disponibles para 8000 días atrás).

Visto que sólo hay 1309 líneas K diarias, comparar los datos en los gráficos de cambio:

Se puede ver que los datos también coinciden.

Enlace a la sección

Dirección del modelo:

La plantilla y el código de estrategia anteriores son solo para uso de enseñanza y aprendizaje, por favor optimice y modifique de acuerdo con las necesidades específicas del comercio en vivo.

- Cuantificar el análisis fundamental en el mercado de criptomonedas: ¡Deja que los datos hablen por sí mismos!

- La investigación cuantitativa básica del círculo monetario - ¡No confíes más en los profesores de idiomas, los datos hablan objetivamente!

- Una herramienta esencial en el campo de la transacción cuantitativa - inventor de módulos de exploración de datos cuantitativos

- Dominarlo todo - Introducción a FMZ Nueva versión de la terminal de negociación (con el código fuente de TRB Arbitrage)

- Conozca todo acerca de la nueva versión del terminal de operaciones de FMZ (con código de código de TRB)

- FMZ Quant: Análisis de ejemplos de diseño de requisitos comunes en el mercado de criptomonedas (II)

- Cómo explotar robots de venta sin cerebro con una estrategia de alta frecuencia en 80 líneas de código

- Cuantificación FMZ: Desarrollo de casos de diseño de necesidades comunes en el mercado de criptomonedas (II)

- Cómo utilizar una estrategia de alta frecuencia de 80 líneas de código para explotar y vender robots sin cerebro

- FMZ Quant: Análisis de ejemplos de diseño de requisitos comunes en el mercado de criptomonedas (I)

- Cuantificación FMZ: Desarrollo de casos de diseño de necesidades comunes en el mercado de criptomonedas (1)