Ejemplo de diseño de la estrategia dYdX

El autor:- ¿ Por qué?, Creado: 2022-11-07 10:59:29, Actualizado: 2023-09-15 21:03:43

En respuesta a la demanda de muchos usuarios, la plataforma FMZ ha accedido recientemente a dYdX, un intercambio descentralizado. Alguien que tenga estrategias puede disfrutar del proceso de adquisición de moneda digital dYdX. Solo quería escribir una estrategia de negociación estocástica hace mucho tiempo, no importa si obtiene ganancias. Así que a continuación nos reunimos para diseñar una estrategia de intercambio estocástica, sin importar si la estrategia funciona bien o no, solo aprendemos el diseño de la estrategia.

Diseño de la estrategia de negociación estocástica

Vamos a tener una lluvia de ideas! Se planea diseñar una estrategia de colocar órdenes al azar con indicadores y precios aleatorios. Poner órdenes no es más que ir largo o ir corto, sólo apostando a la probabilidad. Luego usaremos el número aleatorio 1 ~ 100 para determinar si ir largo o ir corto.

Condición para hacer el largo: número aleatorio 1~50. Condición para el cortocircuito: número aleatorio 51~100.

Por lo tanto, tanto ir largo como ir corto son 50 números. A continuación, pensemos en cómo cerrar la posición, ya que es una apuesta, entonces debe haber un criterio para ganar o perder. Establecemos un criterio para stop de ganancia y pérdida fijos en la transacción. Stop de ganancia para ganar, stop de pérdida para perder. En cuanto a la cantidad de stop de ganancia y pérdida, en realidad es el impacto de la relación de ganancia y pérdida, oh sí!

El comercio no es libre de costos, hay suficiente deslizamiento, comisiones, etc. para tirar nuestra tasa de ganancia de comercio estocástico hacia el lado de menos del 50%. Así que, ¿cómo diseñar continuamente? ¿Qué tal diseñar un multiplicador para aumentar la posición? ya que es una apuesta, entonces la probabilidad de perder por 8 ~ 10 veces en una fila de operaciones aleatorias debe ser baja. Así que la primera transacción fue diseñada para colocar una pequeña cantidad de órdenes, lo más pequeño posible. Luego, si pierdo, voy a aumentar la cantidad de órdenes y seguir colocando órdenes al azar.

Está bien, la estrategia está diseñada de manera simple.

Código fuente diseñado:

var openPrice = 0

var ratio = 1

var totalEq = null

var nowEq = null

function cancelAll() {

while (1) {

var orders = _C(exchange.GetOrders)

if (orders.length == 0) {

break

}

for (var i = 0 ; i < orders.length ; i++) {

exchange.CancelOrder(orders[i].Id, orders[i])

Sleep(500)

}

Sleep(500)

}

}

function main() {

if (isReset) {

_G(null)

LogReset(1)

LogProfitReset()

LogVacuum()

Log("reset all data", "#FF0000")

}

exchange.SetContractType(ct)

var initPos = _C(exchange.GetPosition)

if (initPos.length != 0) {

throw "Strategy starts with a position!"

}

exchange.SetPrecision(pricePrecision, amountPrecision)

Log("set the pricePrecision", pricePrecision, amountPrecision)

if (!IsVirtual()) {

var recoverTotalEq = _G("totalEq")

if (!recoverTotalEq) {

var currTotalEq = _C(exchange.GetAccount).Balance // equity

if (currTotalEq) {

totalEq = currTotalEq

_G("totalEq", currTotalEq)

} else {

throw "failed to obtain initial interest"

}

} else {

totalEq = recoverTotalEq

}

} else {

totalEq = _C(exchange.GetAccount).Balance

}

while (1) {

if (openPrice == 0) {

// Update account information and calculate profits

var nowAcc = _C(exchange.GetAccount)

nowEq = IsVirtual() ? nowAcc.Balance : nowAcc.Balance // equity

LogProfit(nowEq - totalEq, nowAcc)

var direction = Math.floor((Math.random()*100)+1) // 1~50 , 51~100

var depth = _C(exchange.GetDepth)

if (depth.Asks.length <= 2 || depth.Bids.length <= 2) {

Sleep(1000)

continue

}

if (direction > 50) {

// long

openPrice = depth.Bids[1].Price

exchange.SetDirection("buy")

exchange.Buy(Math.abs(openPrice) + slidePrice, amount * ratio)

} else {

// short

openPrice = -depth.Asks[1].Price

exchange.SetDirection("sell")

exchange.Sell(Math.abs(openPrice) - slidePrice, amount * ratio)

}

Log("place", direction > 50 ? "buying order" : "selling order", ", price:", Math.abs(openPrice))

continue

}

var orders = _C(exchange.GetOrders)

if (orders.length == 0) {

var pos = _C(exchange.GetPosition)

if (pos.length == 0) {

openPrice = 0

continue

}

// Test for closing the position

while (1) {

var depth = _C(exchange.GetDepth)

if (depth.Asks.length <= 2 || depth.Bids.length <= 2) {

Sleep(1000)

continue

}

var stopLossPrice = openPrice > 0 ? Math.abs(openPrice) - stopLoss : Math.abs(openPrice) + stopLoss

var stopProfitPrice = openPrice > 0 ? Math.abs(openPrice) + stopProfit : Math.abs(openPrice) - stopProfit

var winOrLoss = 0 // 1 win , -1 loss

// drawing the line

$.PlotLine("bid", depth.Bids[0].Price)

$.PlotLine("ask", depth.Asks[0].Price)

// stop loss

if (openPrice > 0 && depth.Bids[0].Price < stopLossPrice) {

exchange.SetDirection("closebuy")

exchange.Sell(depth.Bids[0].Price - slidePrice, pos[0].Amount)

winOrLoss = -1

} else if (openPrice < 0 && depth.Asks[0].Price > stopLossPrice) {

exchange.SetDirection("closesell")

exchange.Buy(depth.Asks[0].Price + slidePrice, pos[0].Amount)

winOrLoss = -1

}

// stop profit

if (openPrice > 0 && depth.Bids[0].Price > stopProfitPrice) {

exchange.SetDirection("closebuy")

exchange.Sell(depth.Bids[0].Price - slidePrice, pos[0].Amount)

winOrLoss = 1

} else if (openPrice < 0 && depth.Asks[0].Price < stopProfitPrice) {

exchange.SetDirection("closesell")

exchange.Buy(depth.Asks[0].Price + slidePrice, pos[0].Amount)

winOrLoss = 1

}

// Test the pending orders

Sleep(2000)

var orders = _C(exchange.GetOrders)

if (orders.length == 0) {

pos = _C(exchange.GetPosition)

if (pos.length == 0) {

if (winOrLoss == -1) {

ratio++

} else if (winOrLoss == 1) {

ratio = 1

}

break

}

} else {

// cancel pending orders

cancelAll()

Sleep(2000)

pos = _C(exchange.GetPosition)

// update the position after cancellation, and check it again

if (pos.length == 0) {

if (winOrLoss == -1) {

ratio++

} else if (winOrLoss == 1) {

ratio = 1

}

break

}

}

var tbl = {

"type" : "table",

"title" : "info",

"cols" : ["totalEq", "nowEq", "openPrice", "bid1Price", "ask1Price", "ratio", "pos.length"],

"rows" : [],

}

tbl.rows.push([totalEq, nowEq, Math.abs(openPrice), depth.Bids[0].Price, depth.Asks[0].Price, ratio, pos.length])

tbl.rows.push(["pos", "type", "amount", "price", "--", "--", "--"])

for (var j = 0 ; j < pos.length ; j++) {

tbl.rows.push([j, pos[j].Type, pos[j].Amount, pos[j].Price, "--", "--", "--"])

}

LogStatus(_D(), "\n", "`" + JSON.stringify(tbl) + "`")

}

} else {

// cancel the pending orders

// reset openPrice

cancelAll()

openPrice = 0

}

Sleep(1000)

}

}

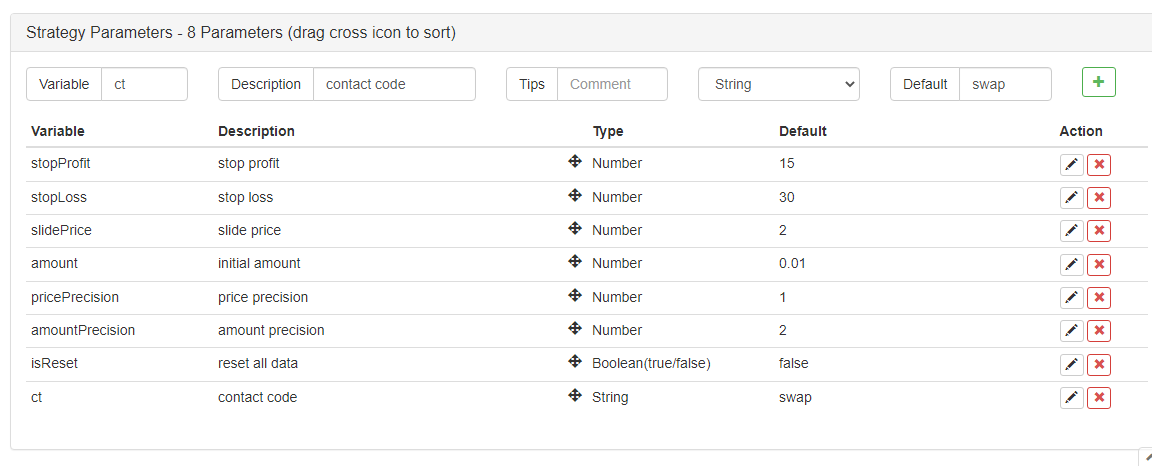

Parámetros de la estrategia:

La estrategia necesita un nombre, vamos a llamarlo

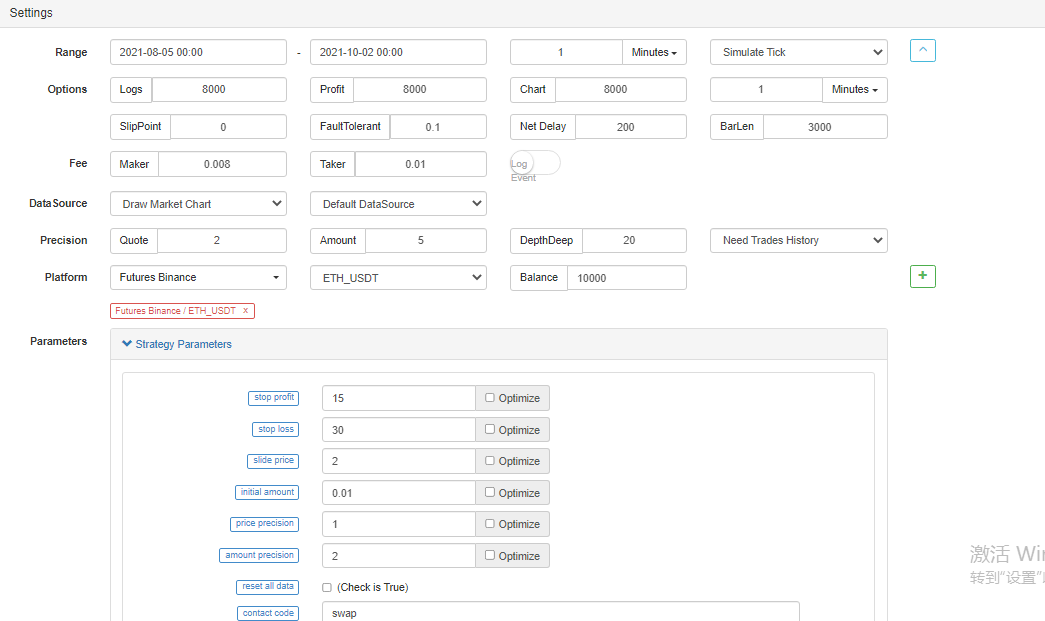

Prueba de retroceso

Las pruebas de retroceso son sólo para referencia, >_

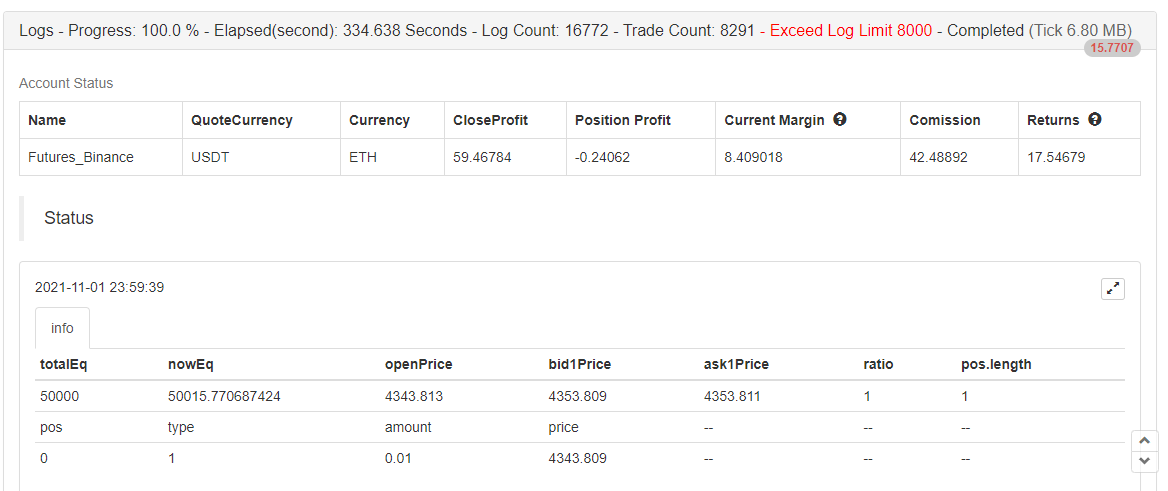

La prueba de retroceso ha terminado, no hay ningún error.

Esta estrategia se utiliza para el aprendizaje y la referencia sólo, no lo use en el bot real!

- Cuantificar el análisis fundamental en el mercado de criptomonedas: ¡Deja que los datos hablen por sí mismos!

- La investigación cuantitativa básica del círculo monetario - ¡No confíes más en los profesores de idiomas, los datos hablan objetivamente!

- Una herramienta esencial en el campo de la transacción cuantitativa - inventor de módulos de exploración de datos cuantitativos

- Dominarlo todo - Introducción a FMZ Nueva versión de la terminal de negociación (con el código fuente de TRB Arbitrage)

- Conozca todo acerca de la nueva versión del terminal de operaciones de FMZ (con código de código de TRB)

- FMZ Quant: Análisis de ejemplos de diseño de requisitos comunes en el mercado de criptomonedas (II)

- Cómo explotar robots de venta sin cerebro con una estrategia de alta frecuencia en 80 líneas de código

- Cuantificación FMZ: Desarrollo de casos de diseño de necesidades comunes en el mercado de criptomonedas (II)

- Cómo utilizar una estrategia de alta frecuencia de 80 líneas de código para explotar y vender robots sin cerebro

- FMZ Quant: Análisis de ejemplos de diseño de requisitos comunes en el mercado de criptomonedas (I)

- Cuantificación FMZ: Desarrollo de casos de diseño de necesidades comunes en el mercado de criptomonedas (1)