Estrategia de trading de AlphaTradingBot

Resumen

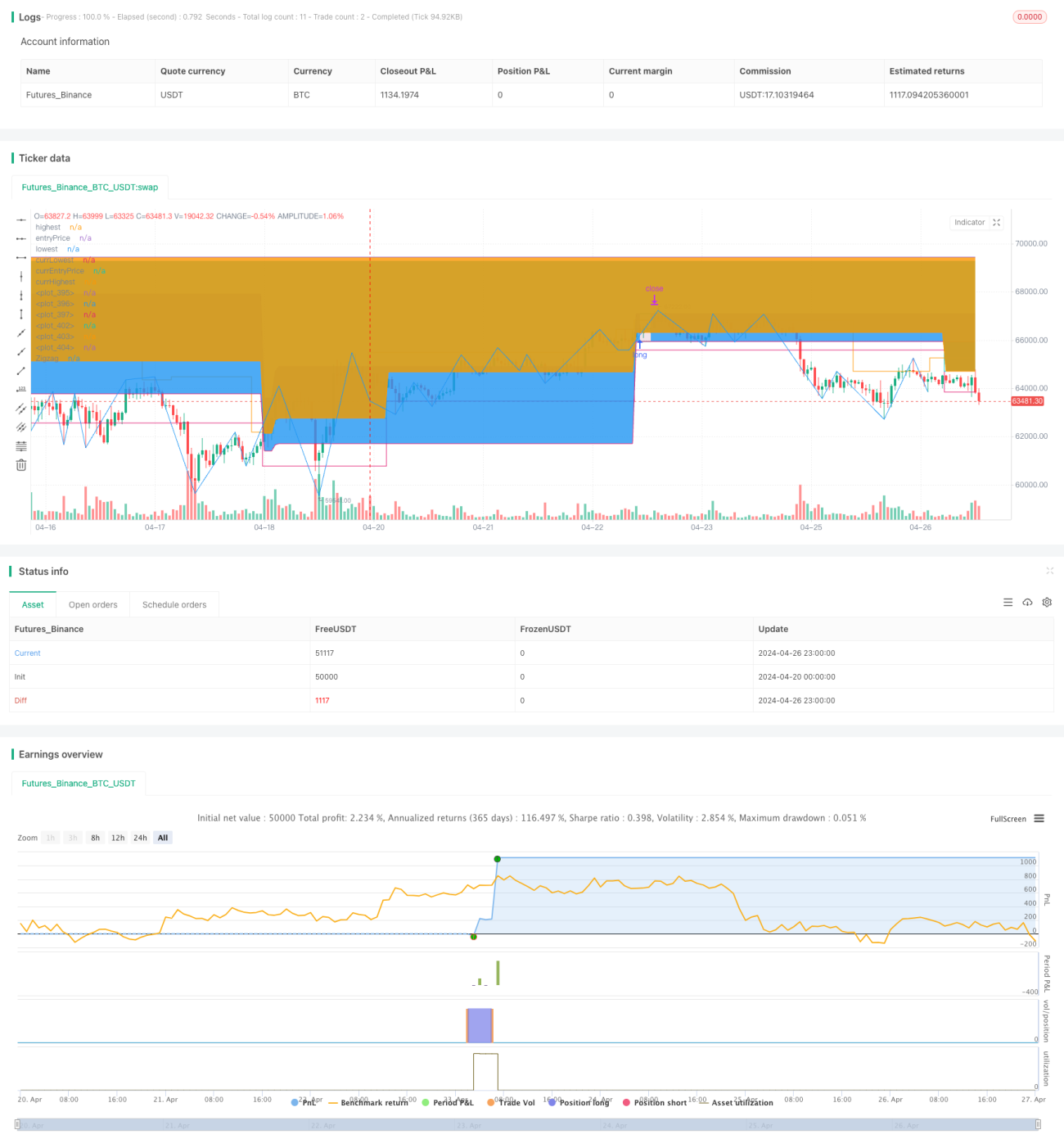

AlphaTradingBot es una estrategia de trading intradía basada en el indicador Zigzag y la secuencia de Fibonacci. Esta estrategia identifica la tendencia detectando los máximos (HH) y mínimos (LL) del mercado, y combina retrocesos y extensiones de Fibonacci para establecer puntos de entrada, take profit y stop loss. La estrategia solo opera dentro de un rango de fechas establecido, pudiendo tomar posiciones largas y cortas por separado, con cierta capacidad para capturar tendencias y controlar la relación riesgo-beneficio.

Principio de la Estrategia

- Utiliza el indicador Zigzag para identificar máximos (HH), mínimos (LL), mínimos más altos (HL) y máximos más bajos (LH) del mercado.

- Cuando aparece un HH, se considera el inicio de una tendencia alcista y se comienza a buscar oportunidades de compra; cuando aparece un LL, se considera el inicio de una tendencia bajista y se buscan oportunidades de venta.

- En una tendencia alcista, si aparece un HL, se toma el rango formado por el HL y el LL anterior como la zona de retroceso de Fibonacci para posiciones largas. Si el precio supera el máximo anterior, se abre una posición larga en la zona de retroceso entre el 23.6% y el 38.2% (configurable), con el stop loss en el retroceso del 61.8% y el take profit calculado según el valor RR (configurable).

- En una tendencia bajista, si aparece un LH, se toma el rango formado por el LH y el HH anterior como la zona de retroceso de Fibonacci para posiciones cortas. Si el precio supera el mínimo anterior, se abre una posición corta en la zona de retroceso entre el 61.8% y el 76.4% (configurable), con el stop loss en el retroceso del 38.2% y el take profit calculado según el valor RR (configurable).

- Gestión de órdenes: solo se abre una orden por señal, hasta que esta se cierre. Si una pérdida individual alcanza el X% (configurable) del capital total de la cuenta, la estrategia deja de operar.

Análisis de Ventajas

- Fuerte capacidad de seguimiento de tendencias. Al identificar eficazmente la tendencia mediante Zigzag, se puede intervenir al inicio de la misma.

- Lógica de retroceso clara. Utilizar los retrocesos de Fibonacci para establecer zonas de entrada permite intervenir durante los retrocesos de la tendencia, con una tasa de aciertos relativamente alta.

- Riesgo controlable. Se controla el riesgo de cada operación estableciendo un porcentaje máximo de pérdida por operación, y un estricto sistema de stop loss garantiza un riesgo total manejable.

- Relación riesgo-beneficio optimizable. Se puede ajustar el valor RR para optimizar la relación riesgo-beneficio de la estrategia según las características del mercado y las preferencias personales.

Análisis de Riesgos

- Trading frecuente. Debido a la alta sensibilidad del Zigzag, puede generar señales con frecuencia, provocando un exceso de operaciones.

- Captura imprecisa de tendencias. La tendencia determinada por Zigzag aún puede presentar desviaciones, lo que lleva a momentos de entrada no ideales.

- Rendimiento deficiente en mercados laterales. En mercados volátiles sin tendencia clara, la estrategia puede generar muchas operaciones perdedoras.

- Período de operación limitado. La estrategia solo opera dentro de un rango de fechas específico, lo que puede hacer que se pierdan parte de los movimientos del mercado.

Direcciones de Optimización

- Incorporar más indicadores técnicos, como MA, MACD, etc., para mejorar la precisión en la identificación de tendencias.

- Optimizar la gestión de posiciones, por ejemplo, ajustando dinámicamente el tamaño de la posición según indicadores como el ATR.

- Optimizar la lógica de take profit y stop loss, por ejemplo, ajustando dinámicamente el nivel de stop loss según la volatilidad del mercado.

- Introducir indicadores de sentimiento del mercado para evitar entrar en condiciones de optimismo o pesimismo extremo.

- Ampliar las restricciones de fecha para aumentar la universalidad de la estrategia.

Resumen

AlphaTradingBot es una estrategia de seguimiento de tendencias intradía basada en el indicador Zigzag y los retrocesos de Fibonacci. Determina la tendencia mediante máximos y mínimos, y entra durante los retrocesos de la tendencia para buscar una mayor tasa de aciertos y una mejor relación riesgo-beneficio. Las ventajas de esta estrategia radican en su fuerte capacidad para capturar tendencias, una lógica de retroceso clara y un riesgo medible, pero también conlleva riesgos como el exceso de operaciones, desviaciones en la identificación de tendencias y un rendimiento deficiente en mercados laterales. En el futuro, se puede optimizar la estrategia en aspectos como indicadores técnicos, gestión de posiciones, take profit/stop loss y sentimiento del mercado, para mejorar su solidez y rentabilidad.

- 1