AlphaTradingBot Stratégie de trading

Aperçu

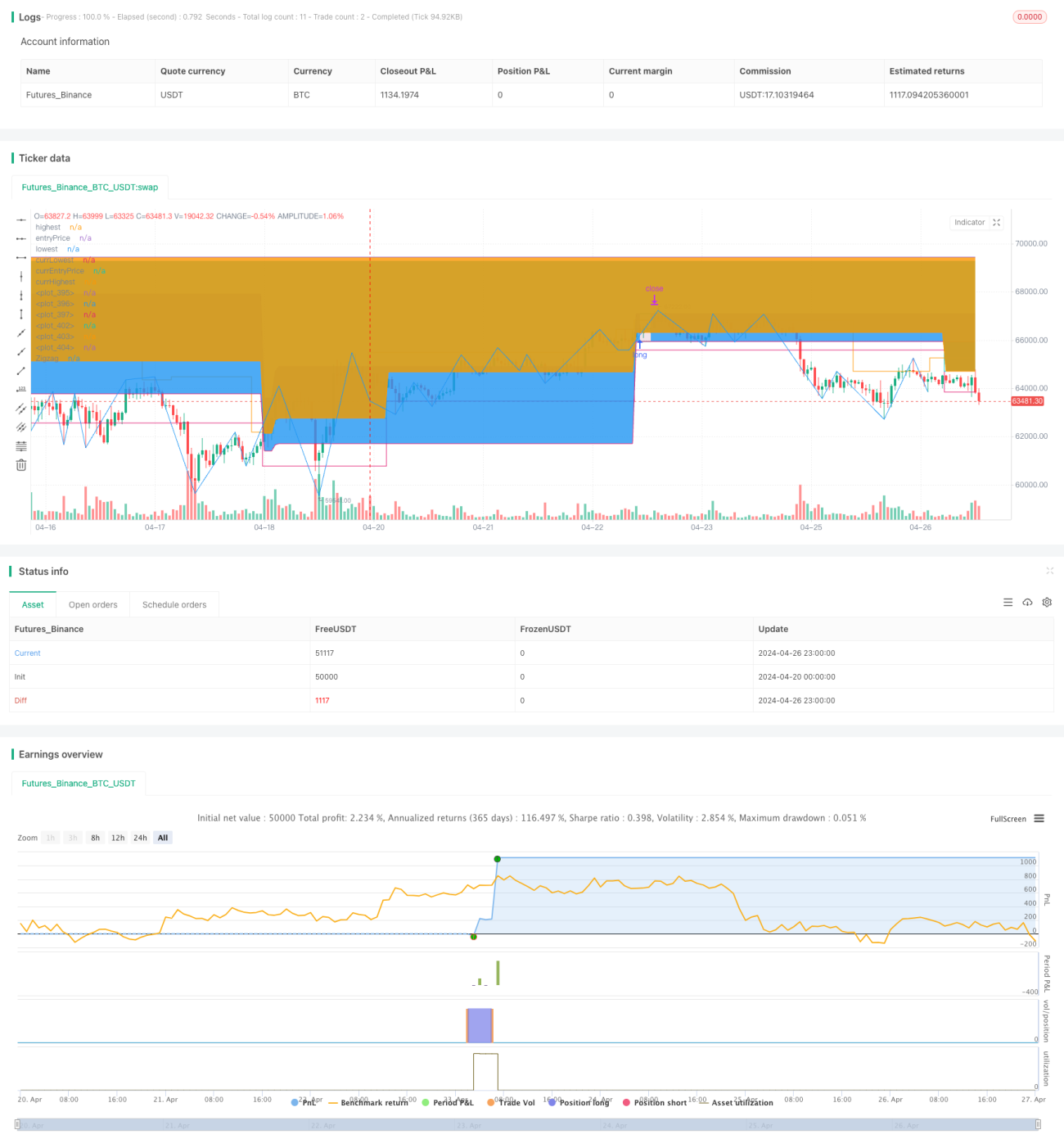

AlphaTradingBot est une stratégie de trading intraday basée sur l'indicateur Zigzag et la suite de Fibonacci. Cette stratégie identifie les tendances en repérant les points hauts (HH) et les points bas (LL) du marché, et utilise les retracements et extensions de Fibonacci pour définir les points d'entrée, les prises de bénéfices et les stop-loss. La stratégie ne fonctionne que dans une plage de dates définie, peut trader à la hausse comme à la baisse, et offre une bonne capacité à saisir les tendances ainsi qu'un ratio risque/récompense contrôlé.

Principe de la stratégie

- L'indicateur Zigzag identifie les points hauts (HH), les points bas (LL), les plus bas élevés (HL) et les plus hauts baissiers (LH) du marché.

- Lorsqu'un HH apparaît, il est considéré comme le début d'une tendance haussière, et l'on cherche des opportunités d'achat. Lorsqu'un LL apparaît, il est considéré comme le début d'une tendance baissière, et l'on cherche des opportunités de vente.

- En tendance haussière, si un HL apparaît, la zone comprise entre ce HL et le LL précédent sert de zone de retracement de Fibonacci pour les positions longues. Si le prix dépasse le précédent sommet, on ouvre une position longue dans la zone de retracement comprise entre 23,6 % et 38,2 % (paramétrable). Le stop-loss est placé à 61,8 % de retracement, et le take-profit est calculé à l'aide du ratio RR (paramétrable).

- En tendance baissière, si un LH apparaît, la zone comprise entre ce LH et le HH précédent sert de zone de retracement de Fibonacci pour les positions short. Si le prix casse le précédent plus bas, on ouvre une position short dans la zone de retracement comprise entre 61,8 % et 76,4 % (paramétrable). Le stop-loss est placé à 38,2 % de retracement, et le take-profit est calculé à l'aide du ratio RR (paramétrable).

- Gestion des ordres : un seul ordre est ouvert par signal, et aucun nouvel ordre n'est placé tant que celui-ci n'est pas clôturé. Si une perte individuelle atteint X % (paramétrable) du capital total, la stratégie cesse de fonctionner.

Analyse des avantages

- Forte capacité de suivi de tendance. L'utilisation du Zigzag permet d'identifier efficacement les tendances et d'intervenir dès leur début.

- Logique de retracement claire. L'utilisation des retracements de Fibonacci pour définir les zones d'entrée lors des corrections de tendance offre un taux de réussite relativement élevé.

- Risque contrôlable. En définissant un pourcentage de perte maximale par transaction, le risque de chaque opération est maîtrisé, et un stop-loss strict garantit la maîtrise du risque global.

- Ratio risque/récompense optimisable. Il est possible d'ajuster le ratio RR en fonction des caractéristiques du marché et des préférences personnelles pour optimiser le ratio risque/récompense de la stratégie.

Analyse des risques

- Trading excessif. La sensibilité élevée du Zigzag peut générer des signaux fréquents, conduisant à un sur-trading.

- Identification imprécise des tendances. Les tendances détectées par le Zigzag peuvent encore être erronées, ce qui peut conduire à des points d'entrée peu optimaux.

- Performance médiocre en marchés rangeés. Dans un marché sans tendance, la stratégie peut générer de nombreuses transactions perdantes.

- Période de fonctionnement limitée. La stratégie ne fonctionne que dans une plage de dates spécifiée, ce qui peut faire manquer certaines opportunités de marché.

Axes d'optimisation

- Introduire davantage d'indicateurs techniques, comme les moyennes mobiles (MA) ou le MACD, pour améliorer la précision de l'identification des tendances.

- Optimiser la gestion des positions, par exemple en ajustant dynamiquement la taille des positions en fonction de l'ATR.

- Optimiser la logique des stop-loss et take-profit, par exemple en ajustant dynamiquement le stop-loss en fonction de la volatilité du marché.

- Introduire des indicateurs de sentiment de marché pour éviter d'entrer en période d'optimisme ou de pessimisme extrême.

- Assouplir les restrictions de dates pour améliorer la polyvalence de la stratégie.

Résumé

AlphaTradingBot est une stratégie de trading intraday de suivi de tendance basée sur l'indicateur Zigzag et les retracements de Fibonacci. Elle identifie les tendances à l'aide des points hauts et bas, et entre sur le marché lors des corrections de tendance afin d'obtenir un taux de réussite et un ratio risque/récompense plus élevés. Les forces de cette stratégie résident dans sa capacité à saisir les tendances, une logique de retracement claire et un risque mesurable. Cependant, elle présente également des risques tels que le sur-trading, des erreurs d'identification des tendances et des performances médiocres en marchés rangeés. À l'avenir, cette stratégie pourra être optimisée en termes d'indicateurs techniques, de gestion des positions, de stop-loss/take-profit et de sentiment du marché, afin d'améliorer sa robustesse et sa rentabilité.

- 1