Penelitian tentang Binance Futures Multi-Values Hedging Strategy Bagian 2

Penulis:Kebaikan, Dibuat: 2020-05-09 16:03:01, Diperbarui: 2023-11-04 19:49:47

Alamat laporan penelitian asli:https://www.fmz.com/digest-topic/5584Anda dapat membacanya terlebih dahulu, artikel ini tidak akan memiliki konten duplikat. Artikel ini akan menyoroti proses pengoptimalan strategi kedua. Setelah pengoptimalan, strategi kedua jelas ditingkatkan, disarankan untuk meningkatkan strategi sesuai dengan artikel ini. Mesin backtest menambahkan statistik biaya penanganan.

# Libraries to import

import pandas as pd

import requests

import matplotlib.pyplot as plt

import seaborn as sns

import numpy as np

%matplotlib inline

symbols = ['ETH', 'BCH', 'XRP', 'EOS', 'LTC', 'TRX', 'ETC', 'LINK', 'XLM', 'ADA', 'XMR', 'DASH', 'ZEC', 'XTZ', 'BNB', 'ATOM', 'ONT', 'IOTA', 'BAT', 'VET', 'NEO', 'QTUM', 'IOST']

price_usdt = pd.read_csv('https://www.fmz.com/upload/asset/20227de6c1d10cb9dd1.csv ', index_col = 0)

price_usdt.index = pd.to_datetime(price_usdt.index)

price_usdt_norm = price_usdt/price_usdt.fillna(method='bfill').iloc[0,]

price_usdt_btc = price_usdt.divide(price_usdt['BTC'],axis=0)

price_usdt_btc_norm = price_usdt_btc/price_usdt_btc.fillna(method='bfill').iloc[0,]

class Exchange:

def __init__(self, trade_symbols, leverage=20, commission=0.00005, initial_balance=10000, log=False):

self.initial_balance = initial_balance # Initial asset

self.commission = commission

self.leverage = leverage

self.trade_symbols = trade_symbols

self.date = ''

self.log = log

self.df = pd.DataFrame(columns=['margin','total','leverage','realised_profit','unrealised_profit'])

self.account = {'USDT':{'realised_profit':0, 'margin':0, 'unrealised_profit':0, 'total':initial_balance, 'leverage':0, 'fee':0}}

for symbol in trade_symbols:

self.account[symbol] = {'amount':0, 'hold_price':0, 'value':0, 'price':0, 'realised_profit':0, 'margin':0, 'unrealised_profit':0,'fee':0}

def Trade(self, symbol, direction, price, amount, msg=''):

if self.date and self.log:

print('%-20s%-5s%-5s%-10.8s%-8.6s %s'%(str(self.date), symbol, 'buy' if direction == 1 else 'sell', price, amount, msg))

cover_amount = 0 if direction*self.account[symbol]['amount'] >=0 else min(abs(self.account[symbol]['amount']), amount)

open_amount = amount - cover_amount

self.account['USDT']['realised_profit'] -= price*amount*self.commission # Minus handling fee

self.account['USDT']['fee'] += price*amount*self.commission

self.account[symbol]['fee'] += price*amount*self.commission

if cover_amount > 0: # close position first

self.account['USDT']['realised_profit'] += -direction*(price - self.account[symbol]['hold_price'])*cover_amount # Profit

self.account['USDT']['margin'] -= cover_amount*self.account[symbol]['hold_price']/self.leverage # Free margin

self.account[symbol]['realised_profit'] += -direction*(price - self.account[symbol]['hold_price'])*cover_amount

self.account[symbol]['amount'] -= -direction*cover_amount

self.account[symbol]['margin'] -= cover_amount*self.account[symbol]['hold_price']/self.leverage

self.account[symbol]['hold_price'] = 0 if self.account[symbol]['amount'] == 0 else self.account[symbol]['hold_price']

if open_amount > 0:

total_cost = self.account[symbol]['hold_price']*direction*self.account[symbol]['amount'] + price*open_amount

total_amount = direction*self.account[symbol]['amount']+open_amount

self.account['USDT']['margin'] += open_amount*price/self.leverage

self.account[symbol]['hold_price'] = total_cost/total_amount

self.account[symbol]['amount'] += direction*open_amount

self.account[symbol]['margin'] += open_amount*price/self.leverage

self.account[symbol]['unrealised_profit'] = (price - self.account[symbol]['hold_price'])*self.account[symbol]['amount']

self.account[symbol]['price'] = price

self.account[symbol]['value'] = abs(self.account[symbol]['amount'])*price

return True

def Buy(self, symbol, price, amount, msg=''):

self.Trade(symbol, 1, price, amount, msg)

def Sell(self, symbol, price, amount, msg=''):

self.Trade(symbol, -1, price, amount, msg)

def Update(self, date, close_price): # Update assets

self.date = date

self.close = close_price

self.account['USDT']['unrealised_profit'] = 0

for symbol in self.trade_symbols:

if np.isnan(close_price[symbol]):

continue

self.account[symbol]['unrealised_profit'] = (close_price[symbol] - self.account[symbol]['hold_price'])*self.account[symbol]['amount']

self.account[symbol]['price'] = close_price[symbol]

self.account[symbol]['value'] = abs(self.account[symbol]['amount'])*close_price[symbol]

self.account['USDT']['unrealised_profit'] += self.account[symbol]['unrealised_profit']

if self.date.hour in [0,8,16]:

pass

self.account['USDT']['realised_profit'] += -self.account[symbol]['amount']*close_price[symbol]*0.01/100

self.account['USDT']['total'] = round(self.account['USDT']['realised_profit'] + self.initial_balance + self.account['USDT']['unrealised_profit'],6)

self.account['USDT']['leverage'] = round(self.account['USDT']['margin']/self.account['USDT']['total'],4)*self.leverage

self.df.loc[self.date] = [self.account['USDT']['margin'],self.account['USDT']['total'],self.account['USDT']['leverage'],self.account['USDT']['realised_profit'],self.account['USDT']['unrealised_profit']]

Kinerja strategi asli, setelah pemilihan jenis mata uang, berjalan dengan baik, tetapi masih ada banyak posisi kepemilikan, umumnya sekitar 4 kali

Prinsipnya:

- Perbarui kutipan pasar dan posisi penyimpanan akun, harga awal akan dicatat pada run pertama (mata uang yang baru ditambahkan dihitung sesuai dengan waktu bergabung)

- Perbarui indeks, indeks adalah indeks harga altcoin-bitcoin = rata-rata (jumlah ((harga altcoin / harga bitcoin) / (harga awal altcoin / harga awal bitcoin))

- Menghakimi operasi panjang dan pendek berdasarkan indeks penyimpangan, dan menilai ukuran posisi berdasarkan ukuran penyimpangan

- Menempatkan pesanan, jumlah pesanan ditentukan oleh strategi komisi gunung es, dan transaksi dilaksanakan sesuai dengan harga terbaru yang dapat dilaksanakan.

- Berputar lagi.

trade_symbols = list(set(symbols)-set(['LINK','XTZ','BCH', 'ETH'])) # Remaining currencies

price_usdt_btc_norm_mean = price_usdt_btc_norm[trade_symbols].mean(axis=1)

e = Exchange(trade_symbols,initial_balance=10000,commission=0.0005,log=False)

trade_value = 300

for row in price_usdt.iloc[:].iterrows():

e.Update(row[0], row[1])

empty_value = 0

for symbol in trade_symbols:

price = row[1][symbol]

if np.isnan(price):

continue

diff = price_usdt_btc_norm.loc[row[0],symbol] - price_usdt_btc_norm_mean[row[0]]

aim_value = -trade_value*round(diff/0.01,1)

now_value = e.account[symbol]['value']*np.sign(e.account[symbol]['amount'])

empty_value += now_value

if aim_value - now_value > 20:

e.Buy(symbol, price, round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

if aim_value - now_value < -20:

e.Sell(symbol, price, -round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

stragey_2b = e

(stragey_2b.df['total']/stragey_2b.initial_balance).plot(figsize=(17,6),grid = True);

stragey_2b.df['leverage'].plot(figsize=(18,6),grid = True); # leverage

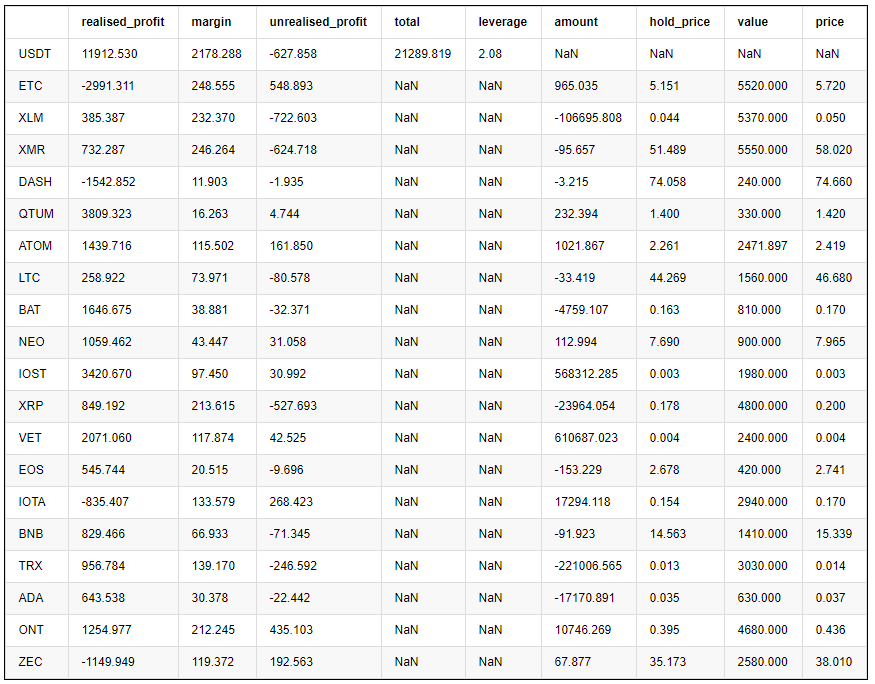

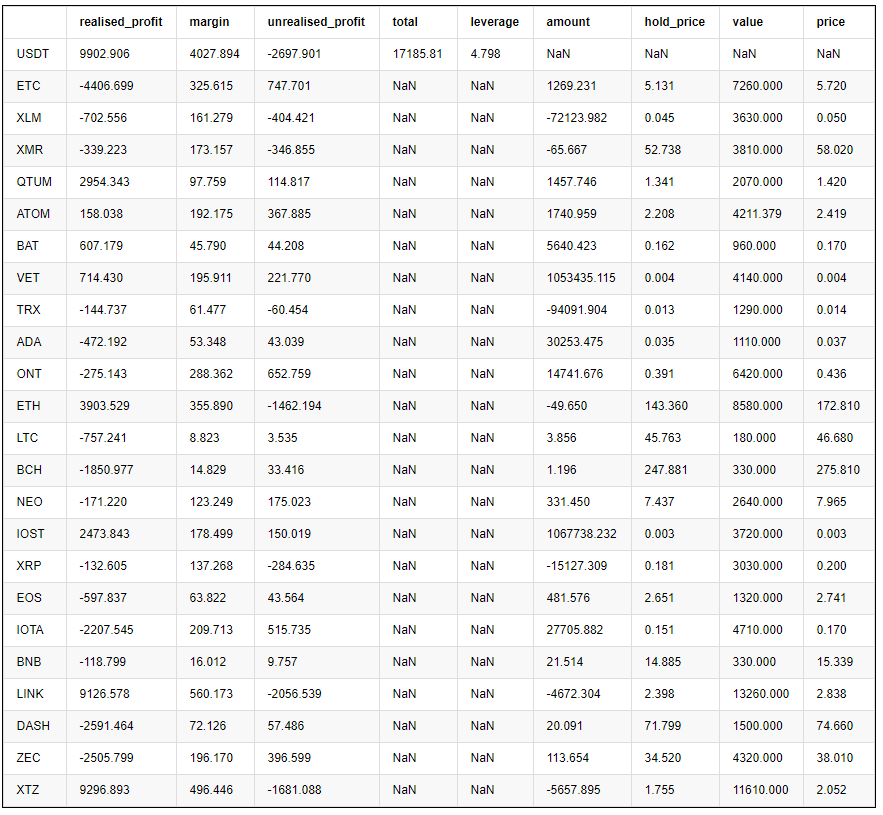

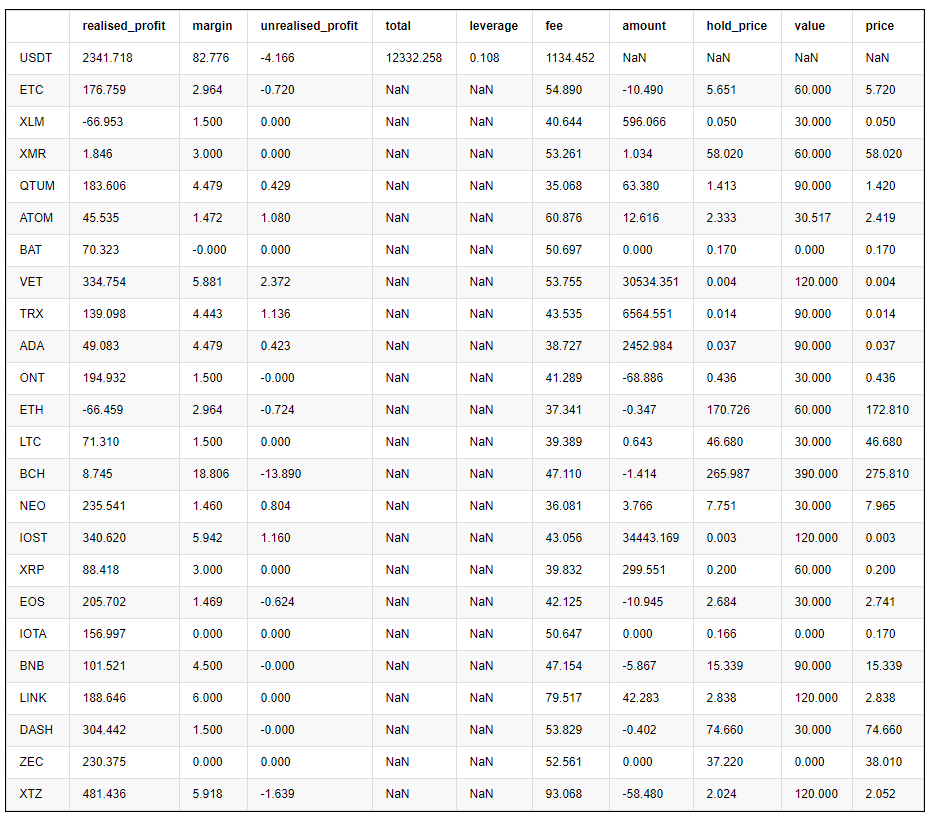

pd.DataFrame(e.account).T.apply(lambda x:round(x,3)) # holding position

Mengapa memperbaiki

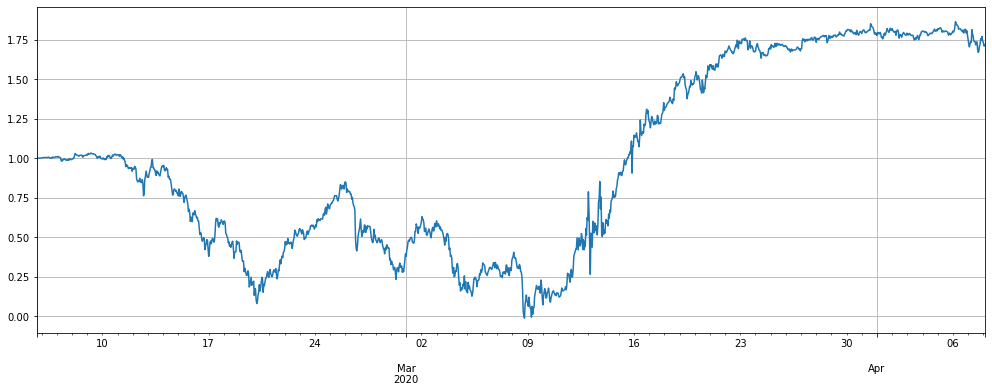

Masalah terbesar awalnya adalah perbandingan antara harga terbaru dan harga awal yang dimulai oleh strategi. Seiring berjalannya waktu, itu akan menjadi lebih dan lebih menyimpang. Kita akan mengumpulkan banyak posisi dalam mata uang ini. Masalah terbesar dengan menyaring mata uang adalah bahwa kita mungkin masih memiliki mata uang unik di masa depan berdasarkan pengalaman masa lalu kita. Berikut adalah kinerja mode non-penyaringan. Sebenarnya, ketika trade_value = 300, di tahap tengah dari strategi berjalan, itu sudah kehilangan segalanya. Bahkan jika tidak, LINK dan XTZ juga memegang posisi di atas 10000USDT, yang terlalu besar. Oleh karena itu, kita harus memecahkan masalah ini di backtest dan lulus tes semua mata uang.

trade_symbols = list(set(symbols)) # Remaining currencies

price_usdt_btc_norm_mean = price_usdt_btc_norm[trade_symbols].mean(axis=1)

e = Exchange(trade_symbols,initial_balance=10000,commission=0.0005,log=False)

trade_value = 300

for row in price_usdt.iloc[:].iterrows():

e.Update(row[0], row[1])

empty_value = 0

for symbol in trade_symbols:

price = row[1][symbol]

if np.isnan(price):

continue

diff = price_usdt_btc_norm.loc[row[0],symbol] - price_usdt_btc_norm_mean[row[0]]

aim_value = -trade_value*round(diff/0.01,1)

now_value = e.account[symbol]['value']*np.sign(e.account[symbol]['amount'])

empty_value += now_value

if aim_value - now_value > 20:

e.Buy(symbol, price, round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

if aim_value - now_value < -20:

e.Sell(symbol, price, -round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

stragey_2c = e

(stragey_2c.df['total']/stragey_2c.initial_balance).plot(figsize=(17,6),grid = True);

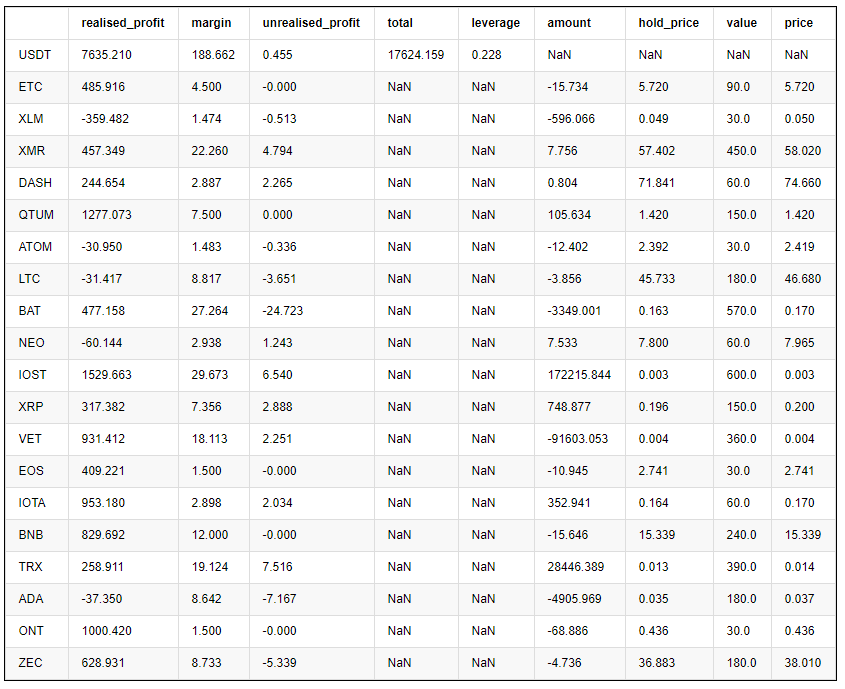

pd.DataFrame(stragey_2c.account).T.apply(lambda x:round(x,3)) # Last holding position

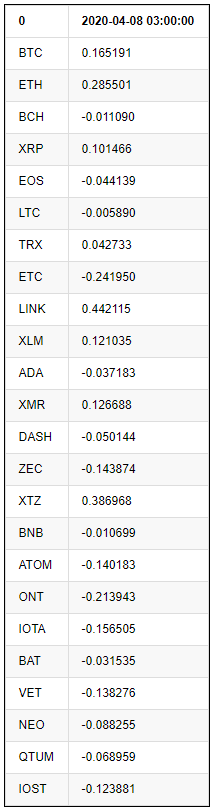

((price_usdt_btc_norm.iloc[-1:] - price_usdt_btc_norm_mean[-1]).T) # Each currency deviates from the initial situation

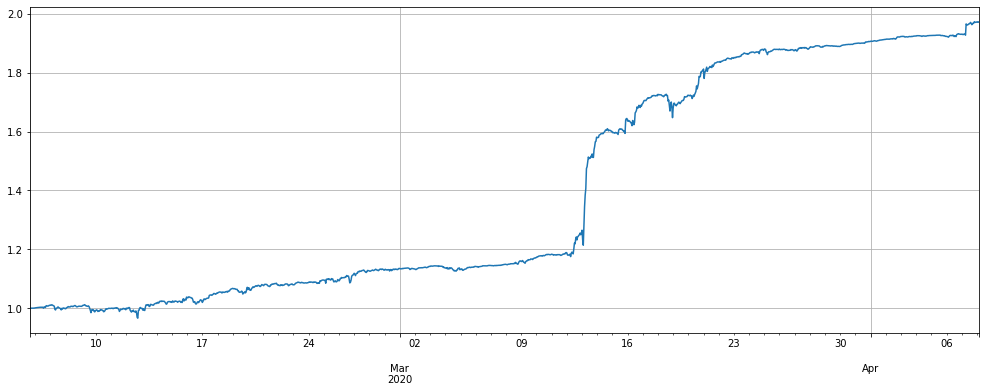

Karena penyebab masalah adalah untuk membandingkan dengan harga awal, itu mungkin lebih dan lebih bias. kita dapat membandingkannya dengan moving average dari periode waktu yang lalu, backtest mata uang penuh dan melihat hasil di bawah ini.

Alpha = 0.05

#price_usdt_btc_norm2 = price_usdt_btc/price_usdt_btc.rolling(20).mean() #Ordinary moving average

price_usdt_btc_norm2 = price_usdt_btc/price_usdt_btc.ewm(alpha=Alpha).mean() # Here is consistent with the strategy, using EMA

trade_symbols = list(set(symbols))#All currencies

price_usdt_btc_norm_mean = price_usdt_btc_norm2[trade_symbols].mean(axis=1)

e = Exchange(trade_symbols,initial_balance=10000,commission=0.0005,log=False)

trade_value = 300

for row in price_usdt.iloc[:].iterrows():

e.Update(row[0], row[1])

empty_value = 0

for symbol in trade_symbols:

price = row[1][symbol]

if np.isnan(price):

continue

diff = price_usdt_btc_norm2.loc[row[0],symbol] - price_usdt_btc_norm_mean[row[0]]

aim_value = -trade_value*round(diff/0.01,1)

now_value = e.account[symbol]['value']*np.sign(e.account[symbol]['amount'])

empty_value += now_value

if aim_value - now_value > 20:

e.Buy(symbol, price, round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

if aim_value - now_value < -20:

e.Sell(symbol, price, -round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

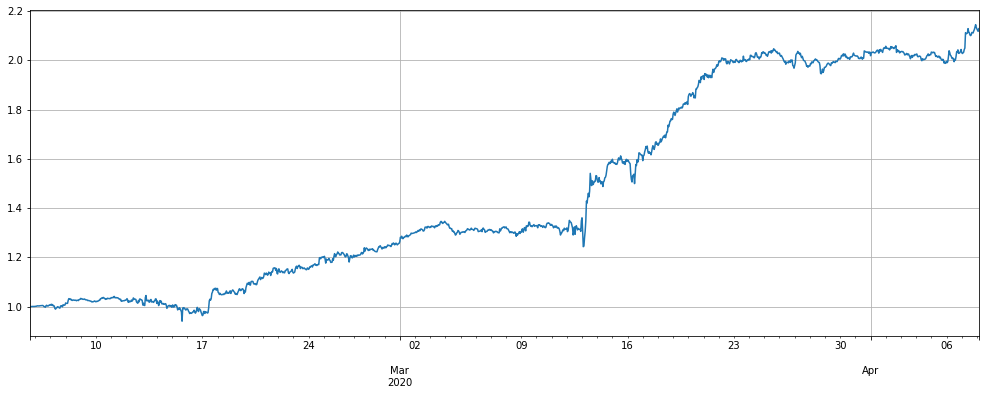

stragey_2d = e

#print(N,stragey_2d.df['total'][-1],pd.DataFrame(stragey_2d.account).T.apply(lambda x:round(x,3))['value'].sum())

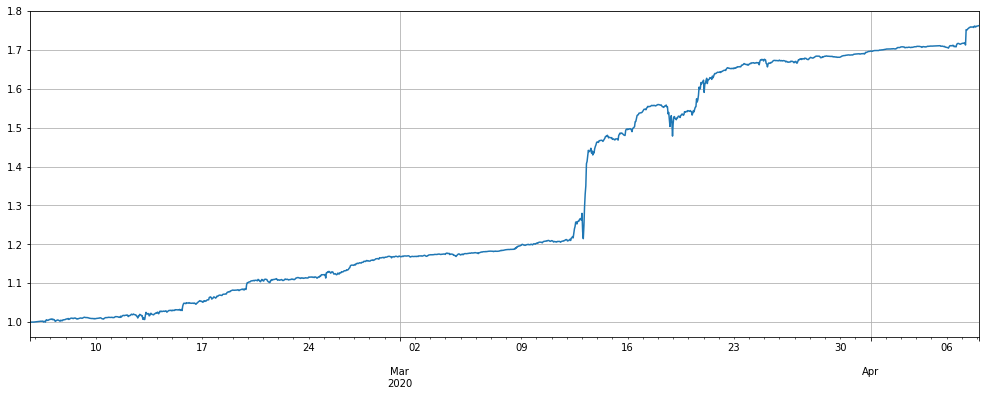

Kinerja strategi telah sepenuhnya memenuhi harapan kami, dan pengembalian hampir sama. Situasi posisi akun pecah dalam mata uang asli dari seluruh mata uang juga telah transisi dengan lancar, dan hampir tidak ada retracement. Ukuran posisi pembukaan yang sama, hampir semua leverage di bawah 1 kali, pada 12 Maret 2020 harga terjun kasus ekstrim, itu masih tidak melebihi 4 kali, yang berarti bahwa kita dapat meningkatkan trade_value, dan di bawah leverage yang sama, menggandakan keuntungan. Posisi kepemilikan akhir hanya BCH melebihi 1000USDT, yang sangat baik.

Mengapa posisi akan diturunkan? Bayangkan bergabung dengan indeks altcoin tidak berubah, satu koin telah meningkat 100%, dan itu akan dipertahankan untuk waktu yang lama. Strategi asli akan memegang posisi pendek 300 * 100 = 30000USDT untuk waktu yang lama, dan strategi baru akhirnya akan melacak harga acuan Pada harga terbaru, Anda tidak akan memegang posisi pada akhirnya.

(stragey_2d.df['total']/stragey_2d.initial_balance).plot(figsize=(17,6),grid = True);

#(stragey_2c.df['total']/stragey_2c.initial_balance).plot(figsize=(17,6),grid = True);

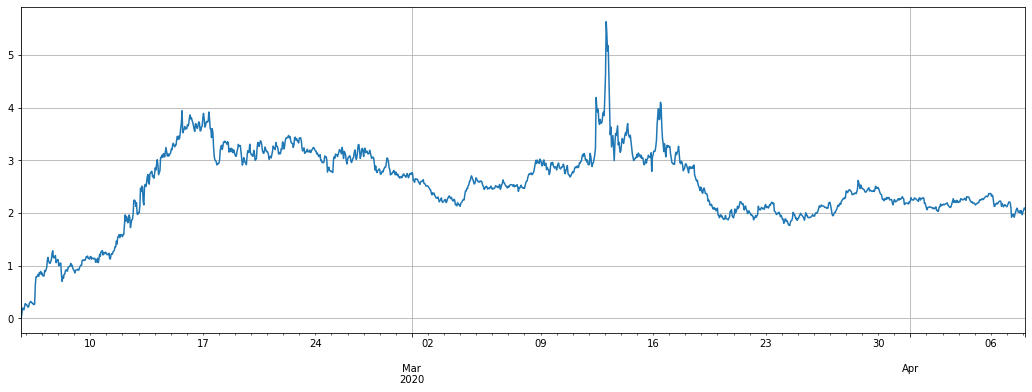

stragey_2d.df['leverage'].plot(figsize=(18,6),grid = True);

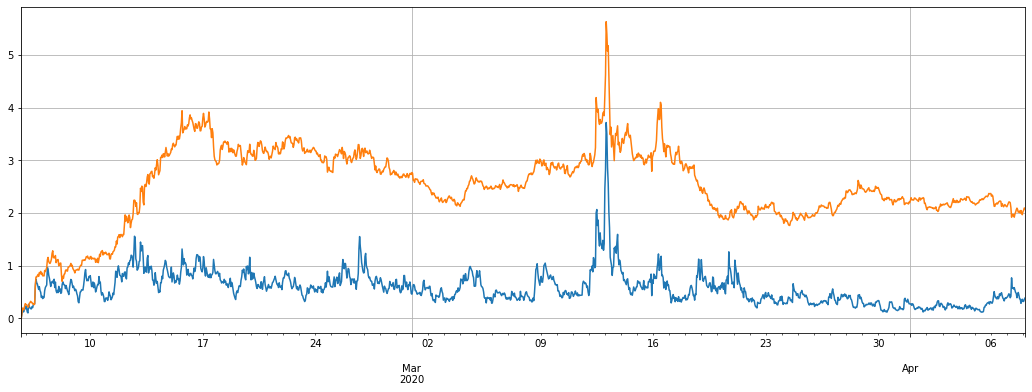

stragey_2b.df['leverage'].plot(figsize=(18,6),grid = True); # Screen currency strategy leverage

pd.DataFrame(stragey_2d.account).T.apply(lambda x:round(x,3))

Apa yang akan terjadi pada mata uang dengan mekanisme skrining, dengan parameter yang sama, keuntungan tahap sebelumnya berkinerja lebih baik, retracement lebih kecil, tetapi pengembalian keseluruhan sedikit lebih rendah.

#price_usdt_btc_norm2 = price_usdt_btc/price_usdt_btc.rolling(50).mean()

price_usdt_btc_norm2 = price_usdt_btc/price_usdt_btc.ewm(alpha=0.05).mean()

trade_symbols = list(set(symbols)-set(['LINK','XTZ','BCH', 'ETH'])) # Remaining currencies

price_usdt_btc_norm_mean = price_usdt_btc_norm2[trade_symbols].mean(axis=1)

e = Exchange(trade_symbols,initial_balance=10000,commission=0.0005,log=False)

trade_value = 300

for row in price_usdt.iloc[:].iterrows():

e.Update(row[0], row[1])

empty_value = 0

for symbol in trade_symbols:

price = row[1][symbol]

if np.isnan(price):

continue

diff = price_usdt_btc_norm2.loc[row[0],symbol] - price_usdt_btc_norm_mean[row[0]]

aim_value = -trade_value*round(diff/0.01,1)

now_value = e.account[symbol]['value']*np.sign(e.account[symbol]['amount'])

empty_value += now_value

if aim_value - now_value > 20:

e.Buy(symbol, price, round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

if aim_value - now_value < -20:

e.Sell(symbol, price, -round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

stragey_2e = e

#(stragey_2d.df['total']/stragey_2d.initial_balance).plot(figsize=(17,6),grid = True);

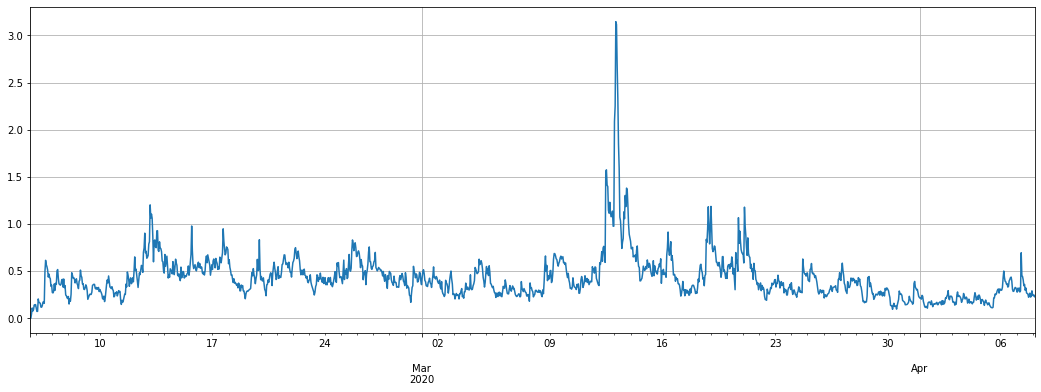

(stragey_2e.df['total']/stragey_2e.initial_balance).plot(figsize=(17,6),grid = True);

stragey_2e.df['leverage'].plot(figsize=(18,6),grid = True);

pd.DataFrame(stragey_2e.account).T.apply(lambda x:round(x,3))

Optimasi parameter

Semakin besar pengaturan parameter Alpha dari rata-rata bergerak eksponensial, semakin sensitif pelacakan harga acuan, semakin sedikit transaksi, semakin rendah posisi kepemilikan akhir. ketika menurunkan leverage, pengembalian juga berkurang. Menurunkan retracement maksimum, dapat meningkatkan volume transaksi. Operasi saldo spesifik perlu berdasarkan hasil backtest.

Karena backtest adalah garis 1h K, hanya dapat diperbarui satu kali dalam satu jam, pasar nyata dapat diperbarui lebih cepat, dan perlu untuk menimbang pengaturan spesifik secara komprehensif.

Ini hasil dari optimasi:

for Alpha in [i/100 for i in range(1,30)]:

#price_usdt_btc_norm2 = price_usdt_btc/price_usdt_btc.rolling(20).mean() # Ordinary moving average

price_usdt_btc_norm2 = price_usdt_btc/price_usdt_btc.ewm(alpha=Alpha).mean() # Here is consistent with the strategy, using EMA

trade_symbols = list(set(symbols))# All currencies

price_usdt_btc_norm_mean = price_usdt_btc_norm2[trade_symbols].mean(axis=1)

e = Exchange(trade_symbols,initial_balance=10000,commission=0.0005,log=False)

trade_value = 300

for row in price_usdt.iloc[:].iterrows():

e.Update(row[0], row[1])

empty_value = 0

for symbol in trade_symbols:

price = row[1][symbol]

if np.isnan(price):

continue

diff = price_usdt_btc_norm2.loc[row[0],symbol] - price_usdt_btc_norm_mean[row[0]]

aim_value = -trade_value*round(diff/0.01,1)

now_value = e.account[symbol]['value']*np.sign(e.account[symbol]['amount'])

empty_value += now_value

if aim_value - now_value > 20:

e.Buy(symbol, price, round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

if aim_value - now_value < -20:

e.Sell(symbol, price, -round((aim_value - now_value)/price, 6),round(e.account[symbol]['realised_profit']+e.account[symbol]['unrealised_profit'],2))

stragey_2d = e

# These are the final net value, the initial maximum backtest, the final position size, and the handling fee

print(Alpha, round(stragey_2d.account['USDT']['total'],1), round(1-stragey_2d.df['total'].min()/stragey_2d.initial_balance,2),round(pd.DataFrame(stragey_2d.account).T['value'].sum(),1),round(stragey_2d.account['USDT']['fee']))

0.01 21116.2 0.14 15480.0 2178.0

0.02 20555.6 0.07 12420.0 2184.0

0.03 20279.4 0.06 9990.0 2176.0

0.04 20021.5 0.04 8580.0 2168.0

0.05 19719.1 0.03 7740.0 2157.0

0.06 19616.6 0.03 7050.0 2145.0

0.07 19344.0 0.02 6450.0 2133.0

0.08 19174.0 0.02 6120.0 2117.0

0.09 18988.4 0.01 5670.0 2104.0

0.1 18734.8 0.01 5520.0 2090.0

0.11 18532.7 0.01 5310.0 2078.0

0.12 18354.2 0.01 5130.0 2061.0

0.13 18171.7 0.01 4830.0 2047.0

0.14 17960.4 0.01 4770.0 2032.0

0.15 17779.8 0.01 4531.3 2017.0

0.16 17570.1 0.01 4441.3 2003.0

0.17 17370.2 0.01 4410.0 1985.0

0.18 17203.7 0.0 4320.0 1971.0

0.19 17016.9 0.0 4290.0 1955.0

0.2 16810.6 0.0 4230.6 1937.0

0.21 16664.1 0.0 4051.3 1921.0

0.22 16488.2 0.0 3930.6 1902.0

0.23 16378.9 0.0 3900.6 1887.0

0.24 16190.8 0.0 3840.0 1873.0

0.25 15993.0 0.0 3781.3 1855.0

0.26 15828.5 0.0 3661.3 1835.0

0.27 15673.0 0.0 3571.3 1816.0

0.28 15559.5 0.0 3511.3 1800.0

0.29 15416.4 0.0 3481.3 1780.0

- Mengkuantifikasi Analisis Fundamental di Pasar Cryptocurrency: Biarkan Data Berbicara Sendiri!

- Di sini, saya akan membahas beberapa hal yang sangat penting tentang penelitian kuantitatif dasar dalam lingkaran mata uang - jangan percaya lagi pada guru-guru sihir yang bodoh, data berbicara secara obyektif!

- Alat penting dalam bidang transaksi kuantitatif - inventor modul eksplorasi data kuantitatif

- Menguasai Semuanya - Pendahuluan ke FMZ Versi Baru Terminal Trading (dengan TRB Arbitrage Source Code)

- Untuk mengetahui semua tentang FMZ, silahkan kunjungi situs resmi FMZ.

- FMZ Quant: Analisis Contoh Desain Persyaratan Umum di Pasar Cryptocurrency (II)

- Cara Mengeksploitasi Robot Penjual Tanpa Otak dengan Strategi Frekuensi Tinggi dalam 80 Baris Kode

- FMZ Kuantitas: Perencanaan Contoh Desain Permintaan Umum di Pasar Cryptocurrency (II)

- Cara Mengeksploitasi Robot Tanpa Otak untuk Dijual dengan Strategi Frekuensi Tinggi 80 Baris Kode

- FMZ Quant: Analisis Contoh Desain Persyaratan Umum di Pasar Cryptocurrency (I)

- Kuantitas FMZ: Perbedaan antara permintaan umum pasar cryptocurrency dan contoh desain (1)