Contoh desain strategi dYdX

Penulis:Lydia, Dibuat: 2022-11-07 10:59:29, Diperbarui: 2023-09-15 21:03:43

Sebagai tanggapan atas permintaan banyak pengguna, platform FMZ telah mengakses dYdX baru-baru ini, pertukaran terdesentralisasi. Seseorang yang memiliki strategi dapat menikmati proses memperoleh mata uang digital dYdX. Saya hanya ingin menulis strategi perdagangan stokastik untuk waktu yang lama, tidak masalah apakah itu menghasilkan keuntungan. Jadi selanjutnya kita datang bersama untuk merancang strategi pertukaran stokastik, tidak peduli apakah strategi berkinerja baik atau tidak, kita hanya belajar desain strategi.

Desain strategi perdagangan stokastik

Mari kita melakukan brainstorming! direncanakan untuk merancang strategi penempatan pesanan secara acak dengan indikator dan harga acak. penempatan pesanan tidak lebih dari pergi panjang atau pergi pendek, hanya bertaruh pada probabilitas. kemudian kita akan menggunakan angka acak 1 ~ 100 untuk menentukan apakah untuk pergi panjang atau pergi pendek.

Kondisi untuk pergi panjang: nomor acak 1 ~ 50. Kondisi untuk pergi pendek: nomor acak 51 ~ 100.

Jadi baik long dan short adalah 50 angka. Selanjutnya, mari kita pikirkan bagaimana menutup posisi, karena ini adalah taruhan, maka harus ada kriteria untuk menang atau kalah. Kami menetapkan kriteria untuk stop profit dan loss tetap dalam transaksi. Stop profit untuk menang, stop loss untuk kalah. Sedangkan jumlah stop profit dan loss, sebenarnya dampak rasio profit dan loss, oh ya! Ini juga mempengaruhi tingkat kemenangan! (Apakah desain strategi ini efektif? Dapatkah dijamin sebagai harapan matematika positif? Lakukan dulu! (Setelah itu, itu hanya untuk belajar, penelitian!)

Trading tidak bebas biaya, ada cukup slippage, biaya, dll untuk menarik stochastic trading win rate kita ke sisi kurang dari 50%. Jadi bagaimana untuk mendesainnya terus menerus? Bagaimana dengan mendesain pengganda untuk meningkatkan posisi? Karena ini adalah taruhan, maka probabilitas kehilangan selama 8 ~ 10 kali berturut-turut dalam perdagangan acak harus rendah. Jadi transaksi pertama dirancang untuk menempatkan sejumlah kecil pesanan, sesedikit mungkin. Kemudian jika saya kalah, saya akan meningkatkan jumlah pesanan dan terus menempatkan pesanan secara acak.

Oke, strategi ini dirancang sederhana.

Kode sumber dirancang:

var openPrice = 0

var ratio = 1

var totalEq = null

var nowEq = null

function cancelAll() {

while (1) {

var orders = _C(exchange.GetOrders)

if (orders.length == 0) {

break

}

for (var i = 0 ; i < orders.length ; i++) {

exchange.CancelOrder(orders[i].Id, orders[i])

Sleep(500)

}

Sleep(500)

}

}

function main() {

if (isReset) {

_G(null)

LogReset(1)

LogProfitReset()

LogVacuum()

Log("reset all data", "#FF0000")

}

exchange.SetContractType(ct)

var initPos = _C(exchange.GetPosition)

if (initPos.length != 0) {

throw "Strategy starts with a position!"

}

exchange.SetPrecision(pricePrecision, amountPrecision)

Log("set the pricePrecision", pricePrecision, amountPrecision)

if (!IsVirtual()) {

var recoverTotalEq = _G("totalEq")

if (!recoverTotalEq) {

var currTotalEq = _C(exchange.GetAccount).Balance // equity

if (currTotalEq) {

totalEq = currTotalEq

_G("totalEq", currTotalEq)

} else {

throw "failed to obtain initial interest"

}

} else {

totalEq = recoverTotalEq

}

} else {

totalEq = _C(exchange.GetAccount).Balance

}

while (1) {

if (openPrice == 0) {

// Update account information and calculate profits

var nowAcc = _C(exchange.GetAccount)

nowEq = IsVirtual() ? nowAcc.Balance : nowAcc.Balance // equity

LogProfit(nowEq - totalEq, nowAcc)

var direction = Math.floor((Math.random()*100)+1) // 1~50 , 51~100

var depth = _C(exchange.GetDepth)

if (depth.Asks.length <= 2 || depth.Bids.length <= 2) {

Sleep(1000)

continue

}

if (direction > 50) {

// long

openPrice = depth.Bids[1].Price

exchange.SetDirection("buy")

exchange.Buy(Math.abs(openPrice) + slidePrice, amount * ratio)

} else {

// short

openPrice = -depth.Asks[1].Price

exchange.SetDirection("sell")

exchange.Sell(Math.abs(openPrice) - slidePrice, amount * ratio)

}

Log("place", direction > 50 ? "buying order" : "selling order", ", price:", Math.abs(openPrice))

continue

}

var orders = _C(exchange.GetOrders)

if (orders.length == 0) {

var pos = _C(exchange.GetPosition)

if (pos.length == 0) {

openPrice = 0

continue

}

// Test for closing the position

while (1) {

var depth = _C(exchange.GetDepth)

if (depth.Asks.length <= 2 || depth.Bids.length <= 2) {

Sleep(1000)

continue

}

var stopLossPrice = openPrice > 0 ? Math.abs(openPrice) - stopLoss : Math.abs(openPrice) + stopLoss

var stopProfitPrice = openPrice > 0 ? Math.abs(openPrice) + stopProfit : Math.abs(openPrice) - stopProfit

var winOrLoss = 0 // 1 win , -1 loss

// drawing the line

$.PlotLine("bid", depth.Bids[0].Price)

$.PlotLine("ask", depth.Asks[0].Price)

// stop loss

if (openPrice > 0 && depth.Bids[0].Price < stopLossPrice) {

exchange.SetDirection("closebuy")

exchange.Sell(depth.Bids[0].Price - slidePrice, pos[0].Amount)

winOrLoss = -1

} else if (openPrice < 0 && depth.Asks[0].Price > stopLossPrice) {

exchange.SetDirection("closesell")

exchange.Buy(depth.Asks[0].Price + slidePrice, pos[0].Amount)

winOrLoss = -1

}

// stop profit

if (openPrice > 0 && depth.Bids[0].Price > stopProfitPrice) {

exchange.SetDirection("closebuy")

exchange.Sell(depth.Bids[0].Price - slidePrice, pos[0].Amount)

winOrLoss = 1

} else if (openPrice < 0 && depth.Asks[0].Price < stopProfitPrice) {

exchange.SetDirection("closesell")

exchange.Buy(depth.Asks[0].Price + slidePrice, pos[0].Amount)

winOrLoss = 1

}

// Test the pending orders

Sleep(2000)

var orders = _C(exchange.GetOrders)

if (orders.length == 0) {

pos = _C(exchange.GetPosition)

if (pos.length == 0) {

if (winOrLoss == -1) {

ratio++

} else if (winOrLoss == 1) {

ratio = 1

}

break

}

} else {

// cancel pending orders

cancelAll()

Sleep(2000)

pos = _C(exchange.GetPosition)

// update the position after cancellation, and check it again

if (pos.length == 0) {

if (winOrLoss == -1) {

ratio++

} else if (winOrLoss == 1) {

ratio = 1

}

break

}

}

var tbl = {

"type" : "table",

"title" : "info",

"cols" : ["totalEq", "nowEq", "openPrice", "bid1Price", "ask1Price", "ratio", "pos.length"],

"rows" : [],

}

tbl.rows.push([totalEq, nowEq, Math.abs(openPrice), depth.Bids[0].Price, depth.Asks[0].Price, ratio, pos.length])

tbl.rows.push(["pos", "type", "amount", "price", "--", "--", "--"])

for (var j = 0 ; j < pos.length ; j++) {

tbl.rows.push([j, pos[j].Type, pos[j].Amount, pos[j].Price, "--", "--", "--"])

}

LogStatus(_D(), "\n", "`" + JSON.stringify(tbl) + "`")

}

} else {

// cancel the pending orders

// reset openPrice

cancelAll()

openPrice = 0

}

Sleep(1000)

}

}

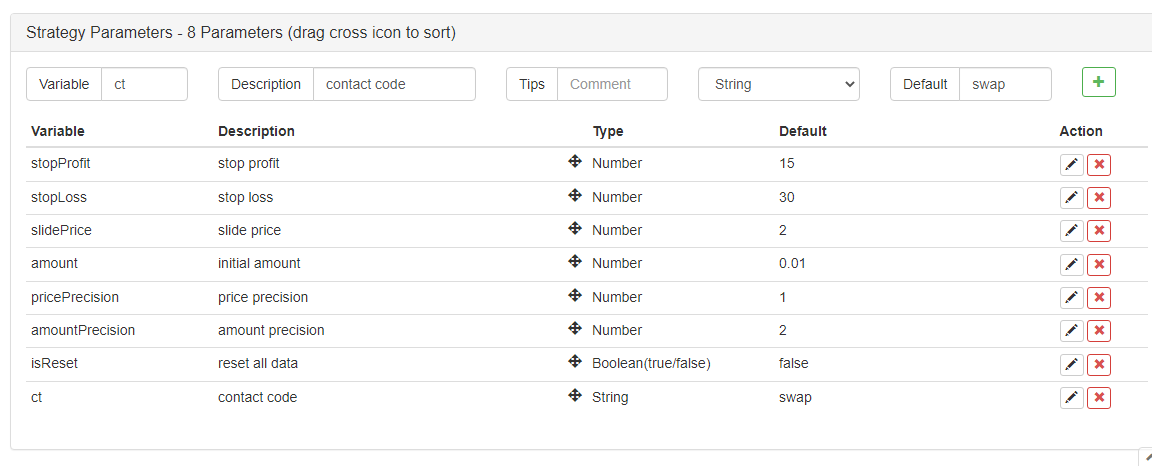

Parameter strategi:

Oh ya! Strategi ini membutuhkan nama, mari kita sebut

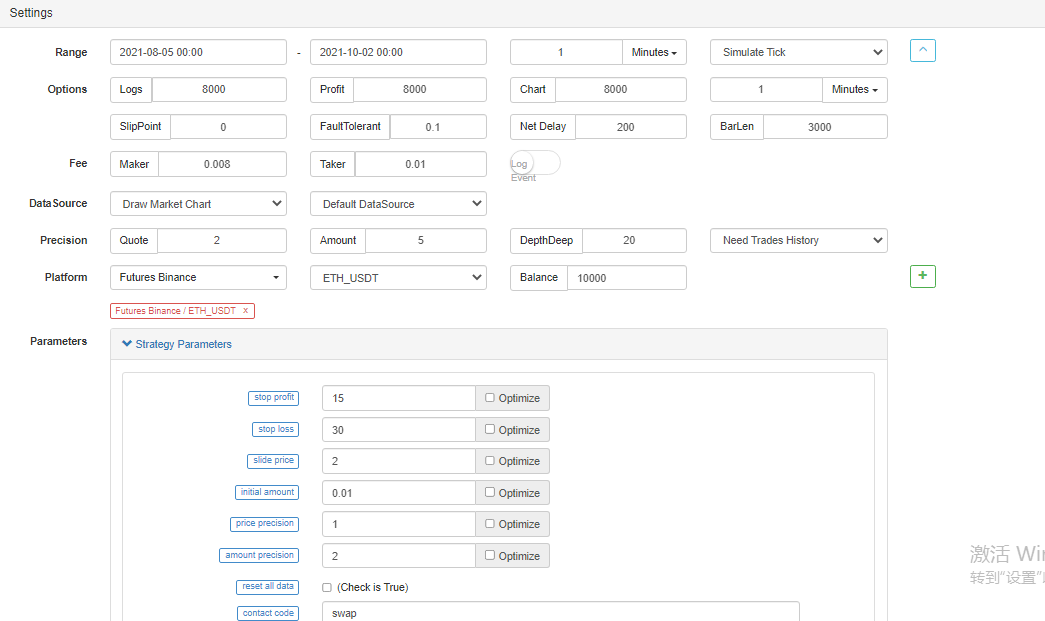

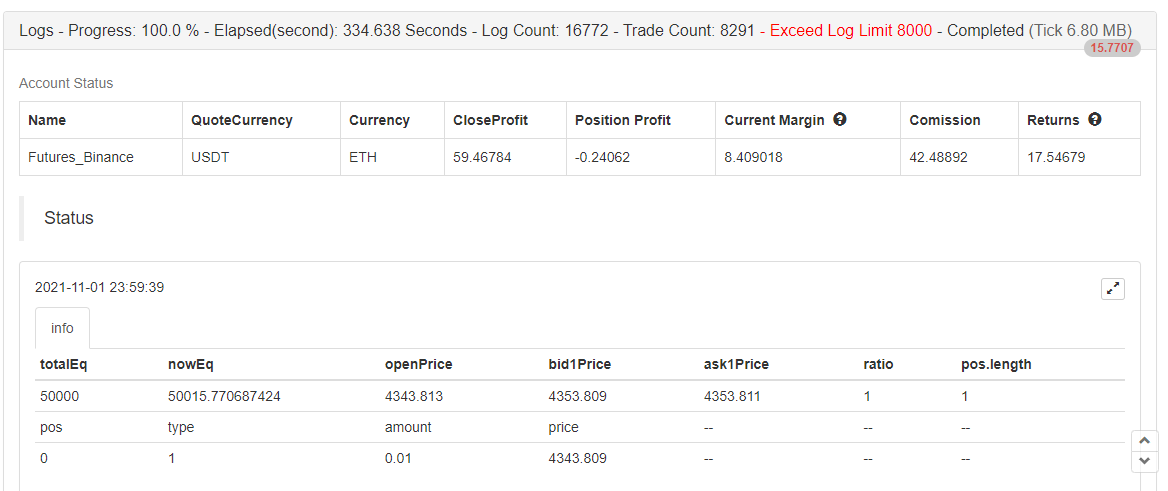

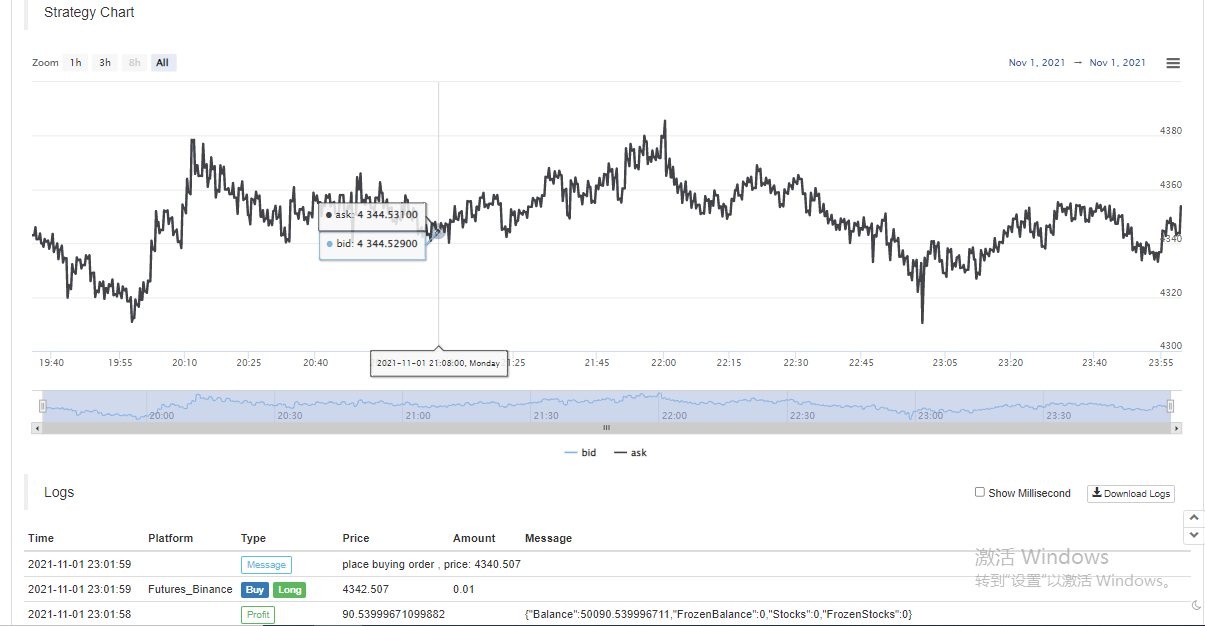

Backtest

Backtesting hanya untuk referensi, >_

Backtest selesai, tidak ada bug.

Strategi ini digunakan untuk belajar dan referensi saja, jangan gunakan di bot nyata!

- Mengkuantifikasi Analisis Fundamental di Pasar Cryptocurrency: Biarkan Data Berbicara Sendiri!

- Di sini, saya akan membahas beberapa hal yang sangat penting tentang penelitian kuantitatif dasar dalam lingkaran mata uang - jangan percaya lagi pada guru-guru sihir yang bodoh, data berbicara secara obyektif!

- Alat penting dalam bidang transaksi kuantitatif - inventor modul eksplorasi data kuantitatif

- Menguasai Semuanya - Pendahuluan ke FMZ Versi Baru Terminal Trading (dengan TRB Arbitrage Source Code)

- Untuk mengetahui semua tentang FMZ, silahkan kunjungi situs resmi FMZ.

- FMZ Quant: Analisis Contoh Desain Persyaratan Umum di Pasar Cryptocurrency (II)

- Cara Mengeksploitasi Robot Penjual Tanpa Otak dengan Strategi Frekuensi Tinggi dalam 80 Baris Kode

- FMZ Kuantitas: Perencanaan Contoh Desain Permintaan Umum di Pasar Cryptocurrency (II)

- Cara Mengeksploitasi Robot Tanpa Otak untuk Dijual dengan Strategi Frekuensi Tinggi 80 Baris Kode

- FMZ Quant: Analisis Contoh Desain Persyaratan Umum di Pasar Cryptocurrency (I)

- Kuantitas FMZ: Perbedaan antara permintaan umum pasar cryptocurrency dan contoh desain (1)